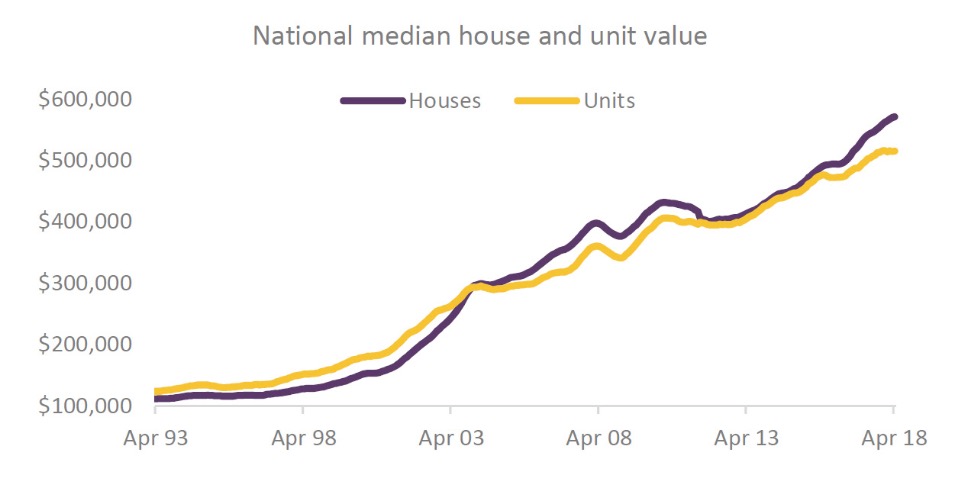

If you ask any investor who purchased an apartment back in 2010 if they were happy with their purchase, you’d likely hear some mixed sentiment. Plenty of advisors supported apartment purchases, and for good historical reasons. This chart may come as a surprise, but for a good few years prior to 2003, the national unit price median sat above that of houses.

Houses and apartment price movements have broadly remained in step over the years, however the relative performance of established Melbourne apartments has been disappointing in many postcodes.

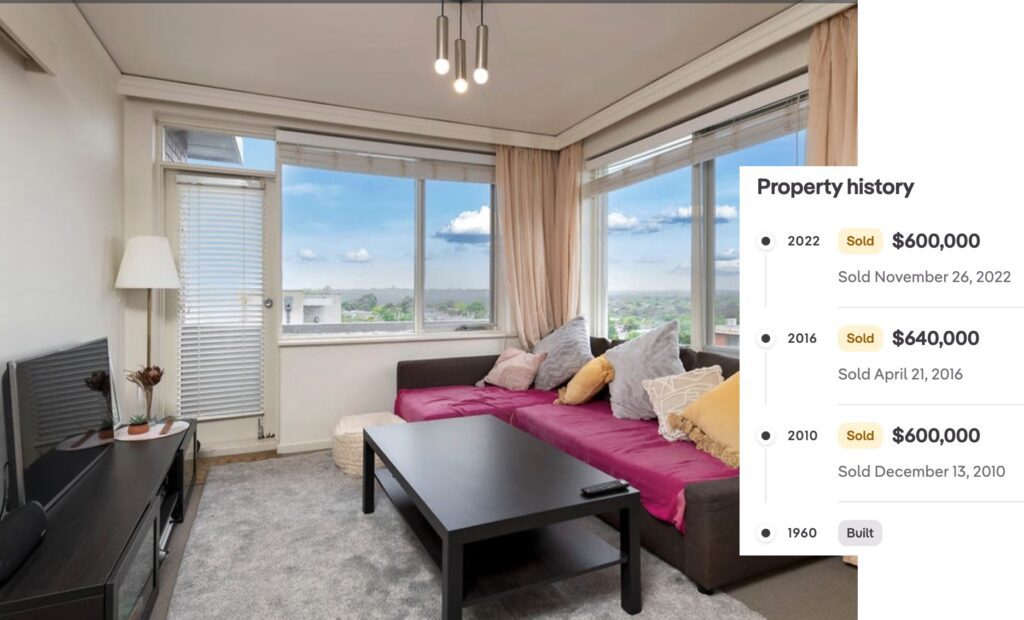

In some leafy suburbs like Kew and Hawthorn, some established apartments are selling now for similar prices to what they were last purchased for, twelve and thirteen years ago. This 1960’s apartment in Kew serves as an example. It last sold in November 2022 for $600K, some $40,000 less than it’s earlier sale price in 2014. No doubt a disappointing result for the former vendor.

Apartments in some parts of Melbourne exhibited lacklustre performance, more so than other capitals around our nation.

The question is, will established apartments rebound, or are Melbourne houses always going to outperform the unit market?

First, we have to look at the reasons why Melbourne apartments underperformed for a long period. Investors generally are reluctant to spend a similar budget on their investment property when contrasted to their family home. Price points in quality areas dictate a unit purchase when a smaller budget is driving the decision.

Secondly, our city is quite sprawling and houses have been in demand as our net migration has continued to grow. Demand in the new fringe areas for house and land packages has been very strong, and new arrivals have chosen to target larger properties. Outer suburban house and land prices have broadly matched that of inner-ring apartments.

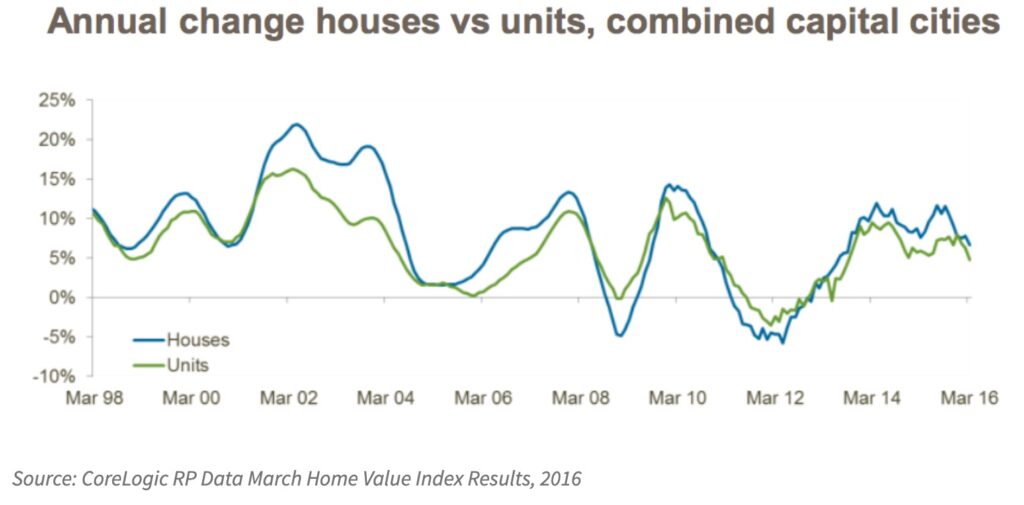

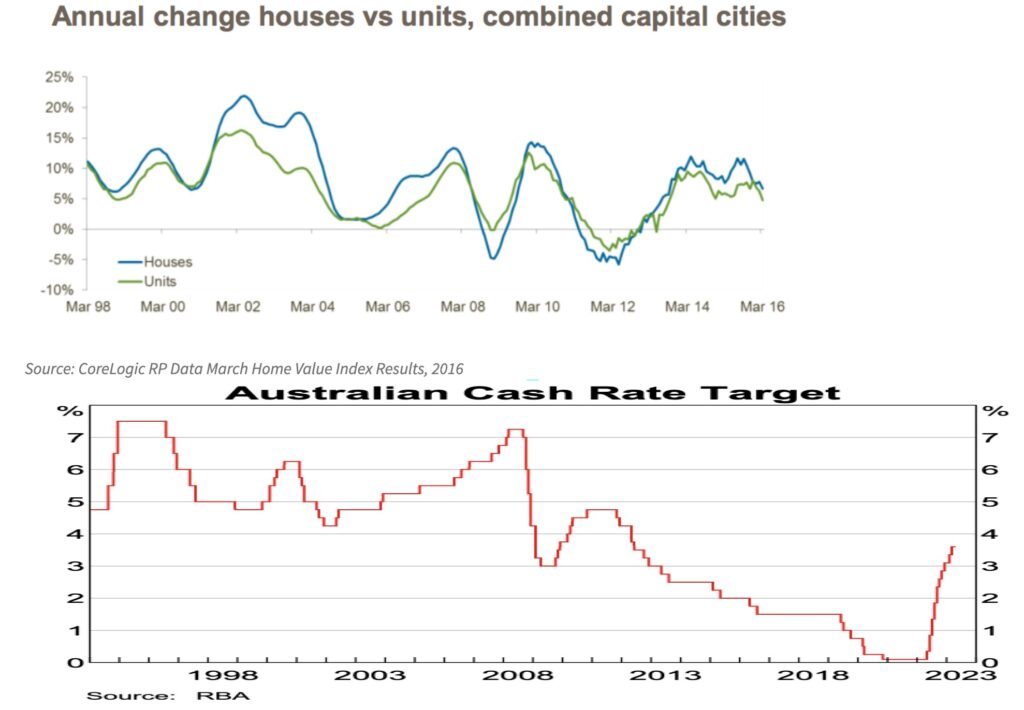

Interest rates were in decline during 2011 – 2022, a period that saw significant house price growth. Contrasting this house/unit price movement chart with the same period’s cash rate chart is interesting and certainly shows a correlation between house outperformance and the cost of credit.

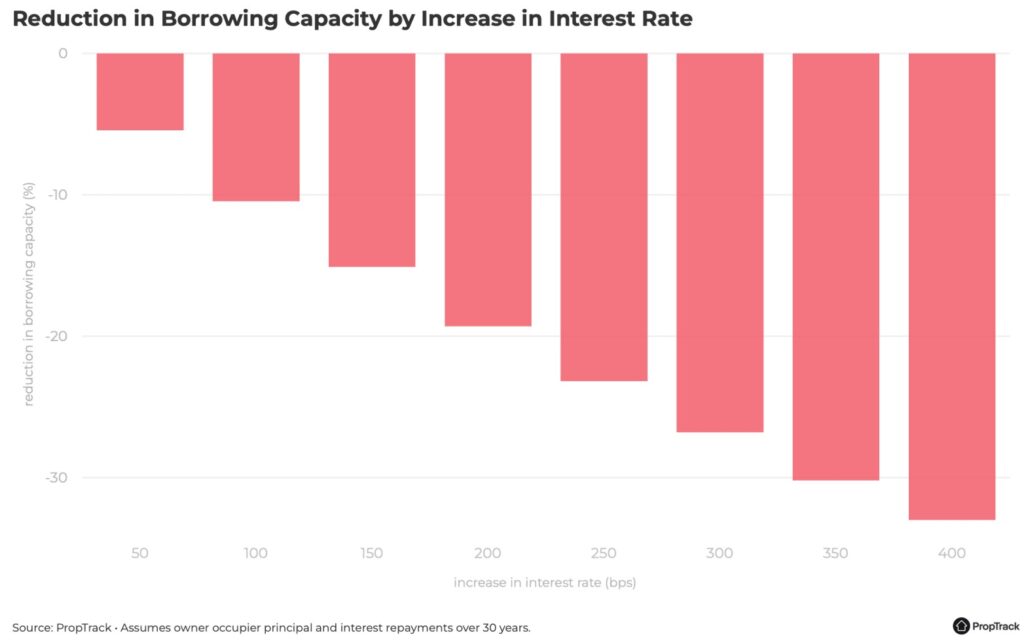

Looking more recently at our interest rate movements and the direct impact on borrowing capacity, the reduction in spend capacity is having a direct impact on consumer choices.

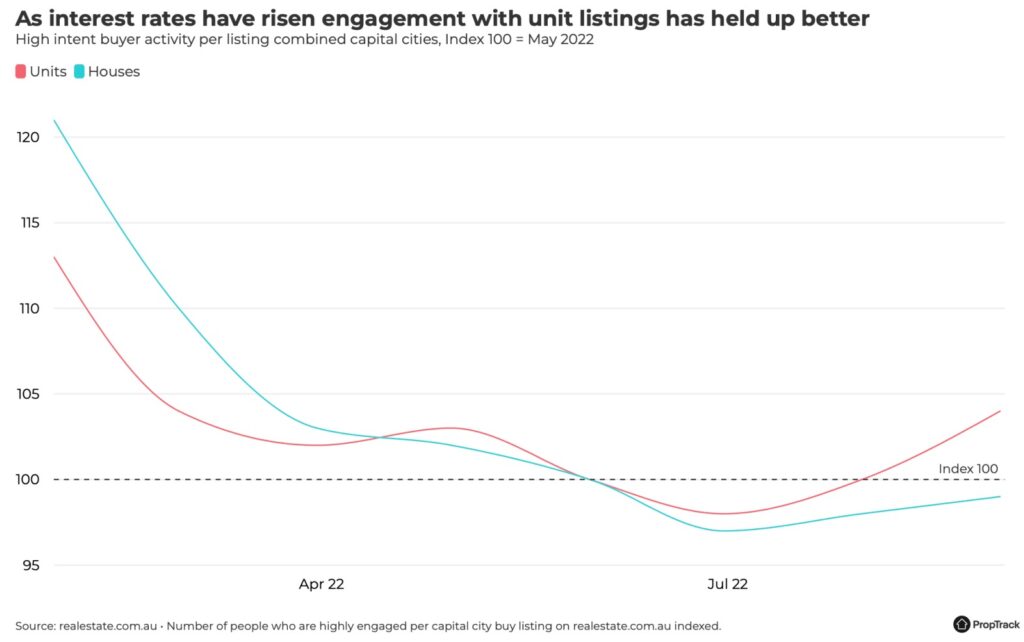

Below shows consumer engagement on realestate.com.au for both houses and units.

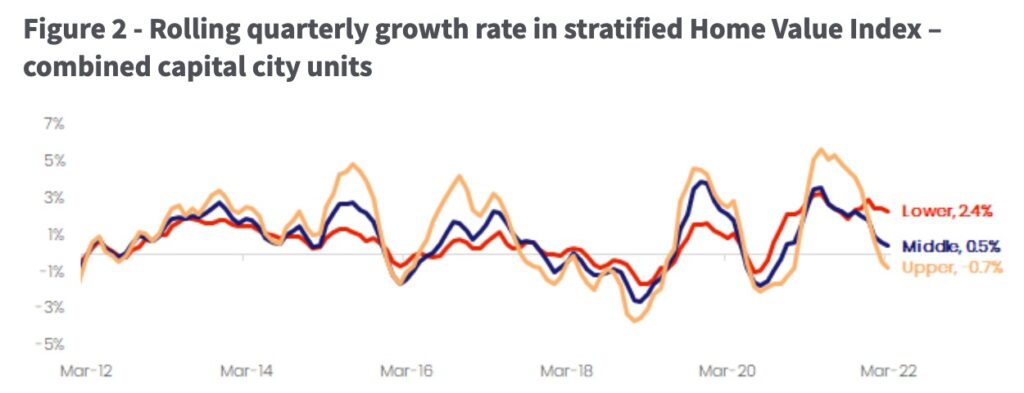

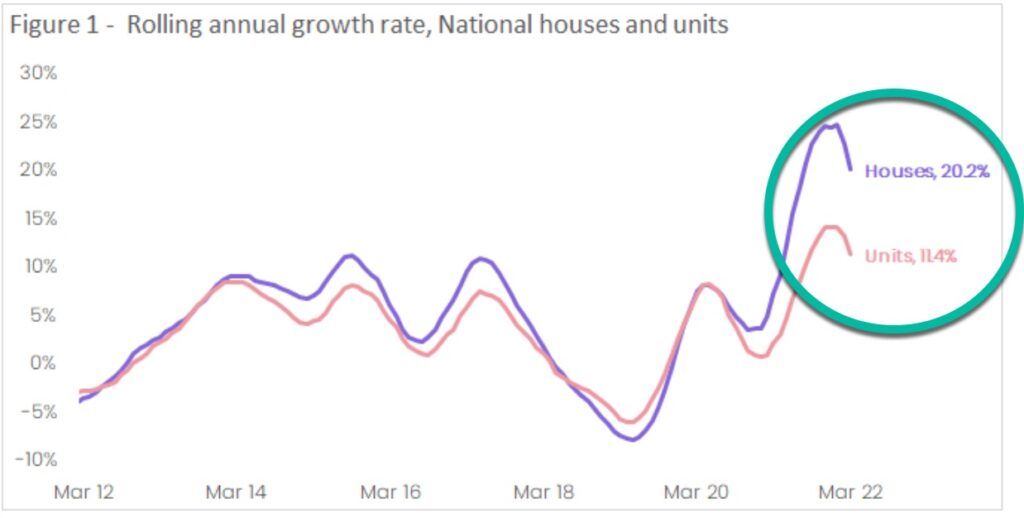

Focusing more specifically on the upper, middle and lower quadrants, we can see that the most affordable segment of the market has experienced the highest recent capital growth rates also; a certain correlation with increasing interest costs and tougher household affordability conditions.

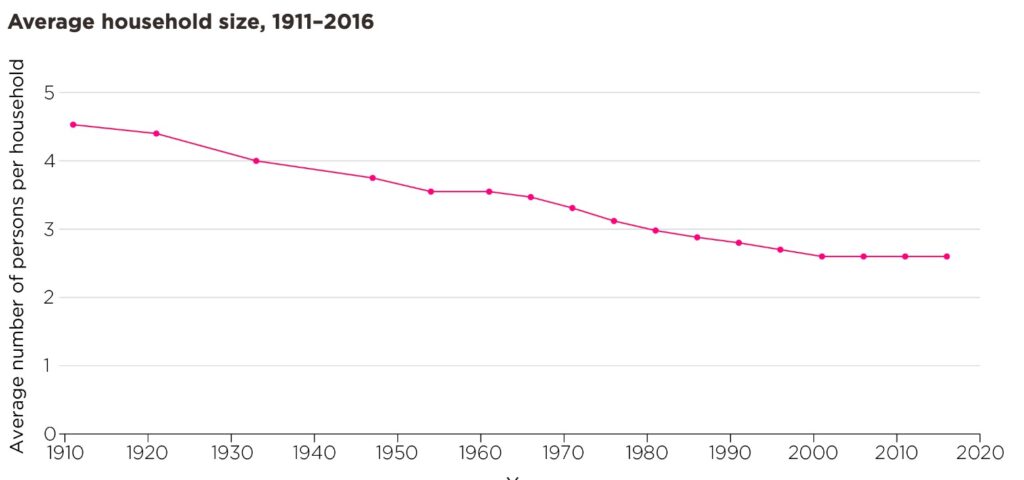

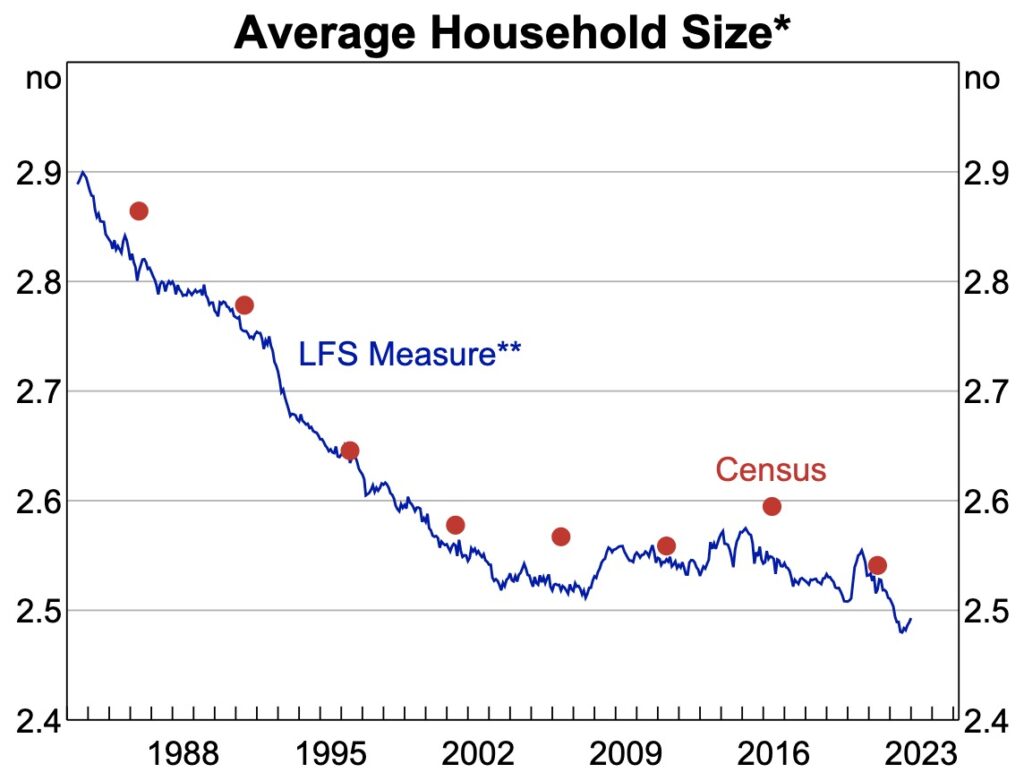

What is really interesting to note is also the household size and how this has reduced over the years. COVID created some immediate spikes, but looking more generally at this chart shows that household average sizes are more conducive to apartment living than previous decades.

Another interesting point relates to the ratio of house price to unit price. The gap has widened the most in recent years; potentially hinting at an opportunity for investors to target quality apartments while the differential in price points is at a historical maximum.

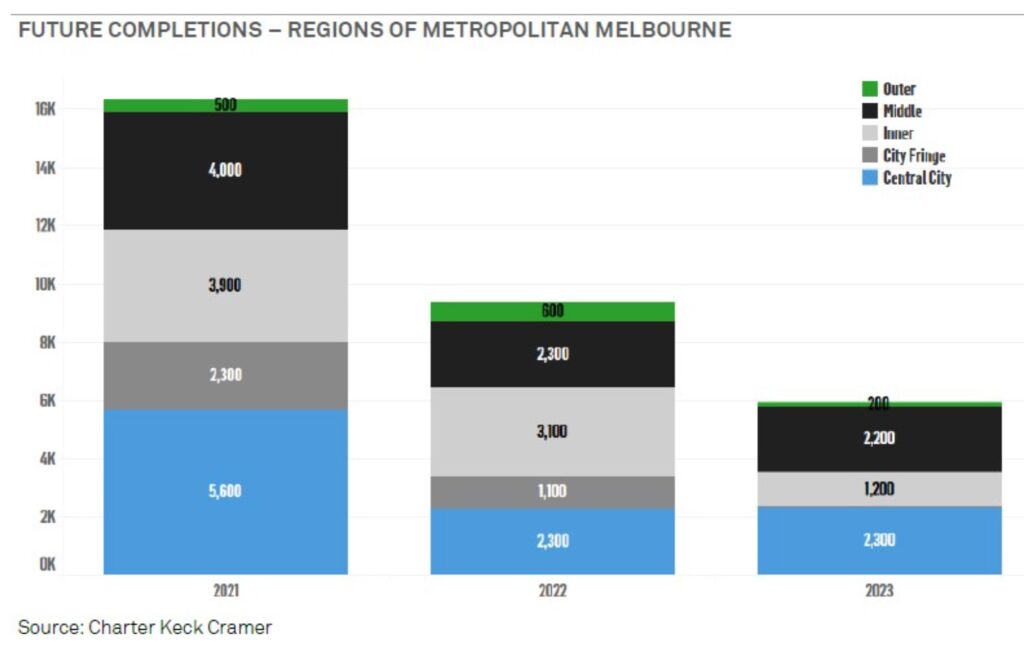

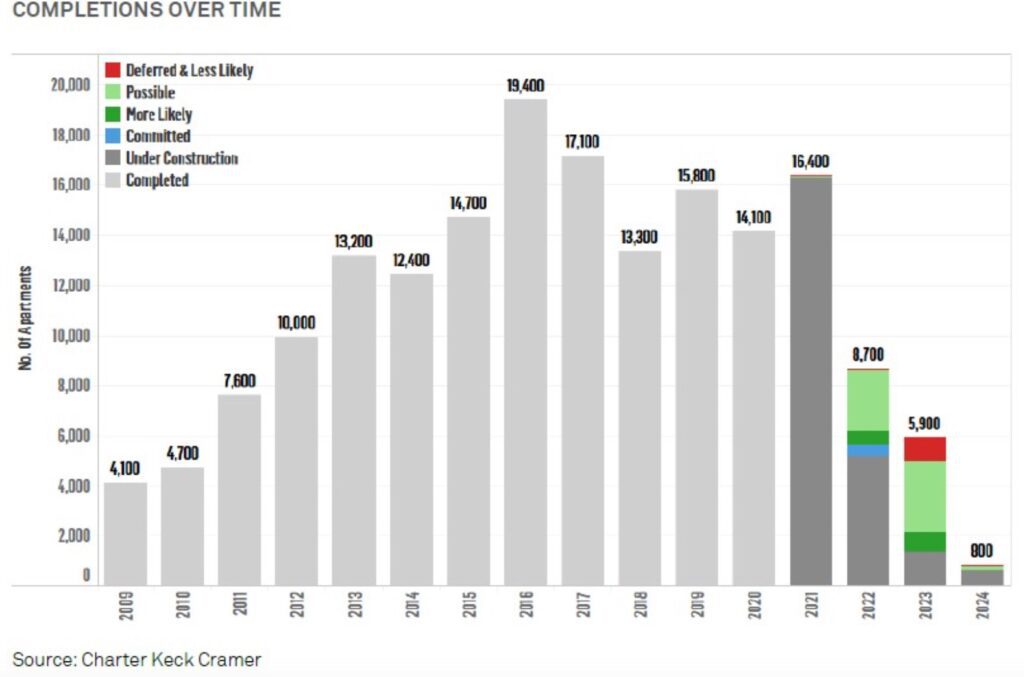

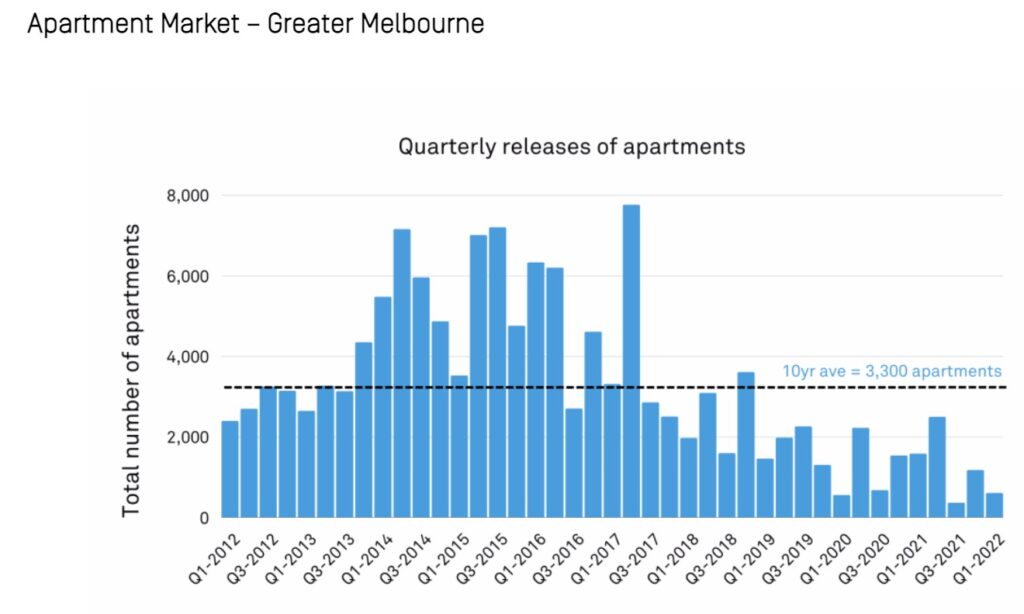

But one significant change we must note relates to apartment building starts and future completions. This data below shows the sheer reduction in apartment building activity in Melbourne and it doesn’t appear to be increasing in the short to medium term.

The rising building costs, the challenges presented during COVID, and the oversupply issues that hampered a lot of developers a decade ago have contributed to the problem of undersupply that we face now.

There are some compelling reasons to support a rebound in apartment capital growth performance, but like any dwelling type, location counts for everything, as does land to asset ratio and the physical quality of the block itself.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU