The first half of 2017 is shaping up to be defined by our business as the change of our normal blend. We have historically helped a larger proportion of investors in their quest to build a wealthier future; and our blend of home-finders has generally sat between 20-40% of our active clients. The Home-Finder client numbers currently sit just above 50% for us right now.

We can put this down to two changed elements in our current landscape.

- The incredibly difficult buying conditions in this under-supplied market are proving tough for many buyers.

- Investment lending has completely tightened up and clamped many investment spend-limits. APRA’s enforced limitations on bank lending to this segment of buyers has indeed taken effect and investor numbers are indeed diminishing, as are investor budgets. Lender appetites for equity releases are low and scrutiny is high. Many borrowers who purchased investments a year ago wouldn’t even qualify to borrow the same amount now. Loan to Value Ratios (LVRs) have been reduced for investors and just recently the capitalisation of Lender’s Mortgage Insurance at 90% LVR was struck. What this means is investors need to fund the LMI themselves; the lender will no longer simply add the premium to the balance of the loan. To illustrate the magnitude of the premium, a $1M purchase at 90% LVR will cost around $36,000.^

Lending conditions are quite different for home buyers though. Lenders are still allowing some eligible applicants to borrow as high as 97% of the value of the property when structured as a 95% LVR loan with partially capitalised LMI.

It is fair to say that home buyers are driving our strong market performance right now.

At almost every auction I’ve attended this year, the surprisingly strong results have generally coincided with an emotional squeal and joyous tears in the crowd when the auctioneer’s hammer has finally fallen.

This week when our state budget was announced, it was no surprise that our government decided to offer higher Stamp Duty Concessions for First Home Buyers. After all, we are the most expensive state in the country when it comes to Land Stamp Duty and our radio talkback hosts have been having a field day with the challenges our first home buyers face in relation to housing affordability.

Will the higher concessions help or hinder the very buyers we are trying to assist after July 1?

We believe that the hiked concessions will hinder first home buyers. While the calculation shows the savings on offer to those who are eligible for the free stamp duty up to $600,000 (and concessions from $600,001 to $750,000), what they don’t show on the State Revenue Office site is the impact of higher buying power in the market.

Some will argue, but we predict that the buying conditions for first home buyers in the $400,000 to $650,000 market space will be particularly difficult and competitive. The sale values won’t simply reflect the additional $13K or so which the buyers have preserved in their pockets. They will reflect the higher borrowing power that each buyer has access to based on a stronger capital contribution.

When buyers leverage at a high LVR, their borrowing power is significantly enhanced with that additional $13K or so.

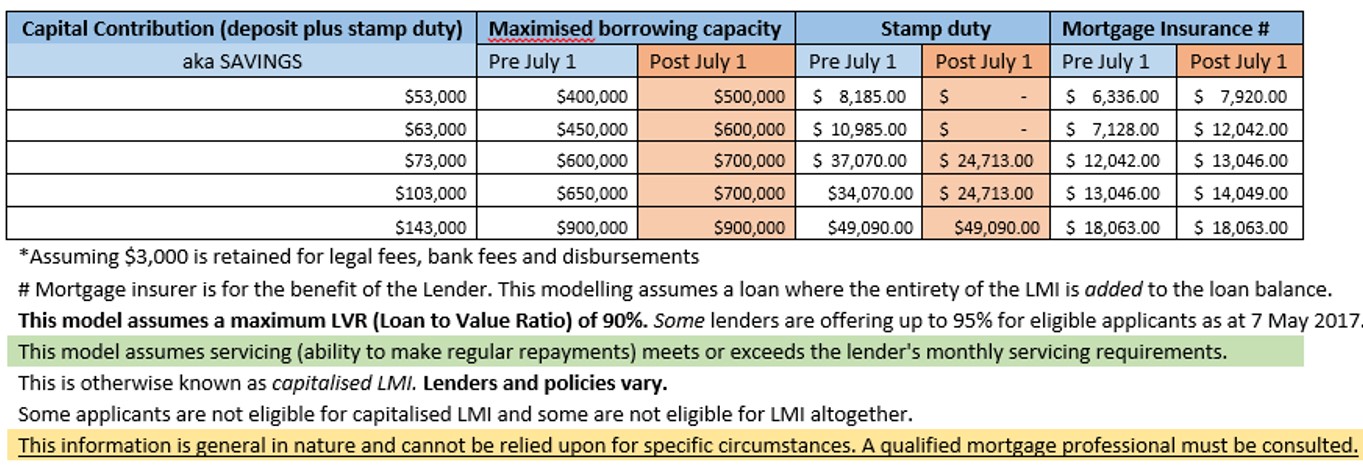

This chart shows the broad changes to borrowing power for five generalised segments; eligible first home buyers with $53K, $63K, $73K, $103K and $143K in savings. For illustrative purposes the chart roughly models the difference in borrowing capacity for buyers who either buy between now and 30 June, or for those who buy on or after July 1. It assumes 90% LVR plus capitalised LMI borrowings to demonstrate how hard these buyers can stretch their reach if they are happy to take on a level of LMI (Lender’s Mortgage Insurance) which most lenders have on offer to those who qualify.

What is really interesting is the changed borrowing power at the lower savings level. Buyers whose savings restricted them from higher borrowing power will wield some power particularly in the $400,000-$700,000 segment of the market.

What we believe this will cause is a distortion to values within this range.

Depending on the pent-up demand by First Home Buyers when changes go live on 1st July, we could see a floodgate swing open in a short space of time. We do anticipate the price movement in this segment of the market will be strong.

This model shown does not take into account Off The Plan (OTP) sales, but based on the relatively small differential for OTP stamp duty charges within the $400K-600K increments, we believe that the established property market will be the most seriously price-impacted.

The properties which we believe will be affected most dramatically include older apartments, villa units, townhouses and houses up to $750,000.

This does prompt the question: are FHB’s who can buy now better off buying before the floodgate opens?

We believe so.

Yesterday’s purchasers in Baxter decided to purchase of their own accord. We proudly assisted two special buyers with their first home purchase in the sub-$500,000 range and despite paying ~$10,000 more stamp duty now than what they could have faced post-1 July, they secured their home in their budget.

The changes certainly warrant careful consideration and discussion.

At this changing time, more than ever – first home buyers need the assistance of a knowledgeable and responsive mortgage broker.

Lending policy is changing almost daily and the conditions above cannot be guaranteed to apply.

The cited approximated figures in the chart are for illustrative purposes only and are general in nature.

SRO calculators have been used and LMI (Genworth) online calculator used:

Genworth Lenders Mortgage Insurance Calculator

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU