“Be greedy when others are fearful, and fearful when others are greedy”. Warren Buffett has famously quoted this line and has successfully applied it to varying asset class investment activity.

Given that supply and demand drive market prices (whether it be shares, bonds, or property), it is vital for investors (and particularly speculators) to be aware of the force and direction of their chosen market.

Contrarians are very small as a percentage of our buyer market, but they are out in force right now.

Property is an interesting asset class for two unique reasons, so careful analysis and due diligence needs to be applied for every purchase;

- Every single property is different. Even when we take two identically sized, copied floorplans with the same-orientation and same floor level, these apartments still don’t sit in the same airspace. They are unique to one another.

- The entry and exit costs and time required to complete the property transaction is slower and more costly than shares and bonds. For this reason, property speculators find themselves up against tougher challenges to make money in the short term.

I’ve consistently held the firm view that it is time in the market, not timing the market that accounts for long term successful wealth creation. But taking advantage of a bear market certainly does aid the progress for the property investor.

Some of my best acquisitions were during the wake of the GFC and during the credit tightening period that immediately followed.

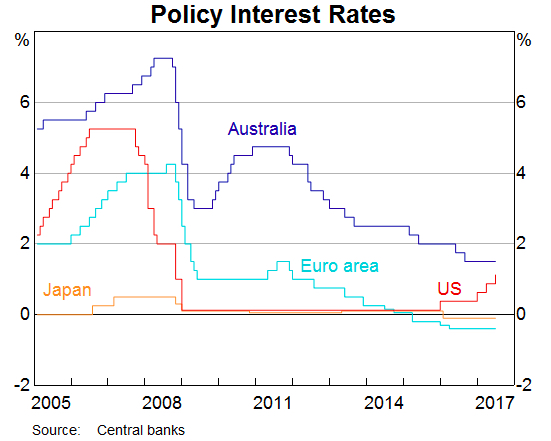

In late 2008, investor sentiment plummeted, vendor discounting became prevalent, our lenders all tightened their credit policies and some lenders opted out of the Australian market altogether. This was particularly noticeable (and very dramatic) for investors because interest rates were higher (see chart below from Central Banks), and our lenders had been offering far looser credit terms in contrast to today’s climate. For example, “No-Doc” loans were available in this same year, and some of our lenders were offering 104% lending for eligible borrowers.

The cloud that borrowers had to come down from was enormous, and lending felt as though it had changed over night.

Today’s environment is quite different. We certainly have a credit squeeze, and by design this APRA-instigated squeeze has cooled our market.

But what positives come from a market correction?

For those who can still borrow, there are some direct positives:

- Less buyer competition. While this sounds so obvious, the ‘spikey prices’ we witnessed a year ago were all achieved with high competition. Buyers knew they were stretching hard, but for highly sought-after properties, they had to stretch.

- Good properties (like really good properties) are now getting snapped up for price tags that don’t have a silly premium attached.

- Lending rates are still low. Some suggest we may have an interest rate rise (I don’t believe we will see a rise for at least a year and I hold the view that our market conditions are not indicating that we need the increase yet). Interest rates are at a record low in Australia.

- Agents and vendors are far more accepting of a finance clause in a buyer’s offer. And with auction clearance rates down in the 50’s, the chances of a property passing in favour a buyer who wishes to purchase with the security of a finance clause.

- We still have negative gearing on offer.

- …. and my personal favourite benefit: Rents are rising.

This last benefit is tangible and evident.

Our client’s acquisitions are monitored by us throughout the entire settlement phase, from rental appraisal to rental manager appointment through to settlement and finally tenanting. We are aware of the rental estimates and appraisals for every property and unlike past years, Melbourne’s rental returns are now increasing as a percentage (yield) and are more competitive between tenants.

Legislation in Victoria does not allow for landlords to engage in auction type tactics when advertising a property for rent. They must advertise a fair figure that they are prepared to accept. However tenants are permitted to offer a higher figure if they feel that they could have higher competing applicants for the same property.

In many cases our client’s rental figure has been 10% higher than appraised.

APRA’s actions to slow down our market and give first home buyers a better chance have certainly taken effect. What the masterminds behind the decision may not have considered is the adverse impact on housing supply to those who need it the most. In Victoria we have increasing population numbers. They have not eased. More and more people need a home.

Without a social housing policy in Australia that offers a viable solution for every price-sensitive tenant, we rely on our landlords (in combination with our government’s negative gearing contribution) to provide housing. The supply and demand equation is uncomfortably swinging out of favour of the tenant and into the favour of the landlord in many markets. With the added pressure that our next government could introduce by abolishing negative gearing, we do have to ask the question;

Is our tougher credit policy hurting the very people it was trying to help?

If and when our masterminds at the top decide this is the case, and once the hangover from the Banking Royal Commission passes and the media spotlight focuses on the next big issue, we can prepare for a loosening of credit again.

Until such time, our eased market conditions may be a just a little window of opportunity. We never can tell exactly when a market correction will switch back into the positive.

We need to ask ourselves if our best time to buy is now.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU