There is so much talk of doom and gloom in the media and it’s making it very difficult for many buyers and sellers to make informed decisions.

Bad news seems to sell papers.

Since our first interest rate rise in eleven years, the most commonly asked question I’ve been fielding is, “Cate, is it a good time to buy?”. And since last week’s half-a-percent surprise rise, the question is coming at me thicker and faster.

Despite my own clear view on the answer, it is as difficult question for me to field because it’s obvious I could carry bias. After all, I’m a buyer’s advocate and my business revenue is based on clients making a decision to purchase. Any of my industry colleagues would understand the sense of responsibility that we have to carry when answering this question. The reality is that none of us can accurately predict what will happen in the short term, and coaxing a client into a purchase decision does not rest comfortably at all. Deciding when to purchase is entirely a personal decision and we always try to provide balanced information to our clients and prospective clients when they are tackling a transitioning, or delicate market.

Ultimately, the decision of when to purchase must take into account personal finance and risk-related considerations.

However, I do have a firm opinion about the state of our market and whether buyers can expect growth. There is no doubt that we are tackling some challenging headwinds as a direct result of pressure on fuel and energy prices, (a war will do that), inflationary pressures and building shortages, but in tandem, our leading indicators tell a far more optimistic story than the daily papers are suggesting.

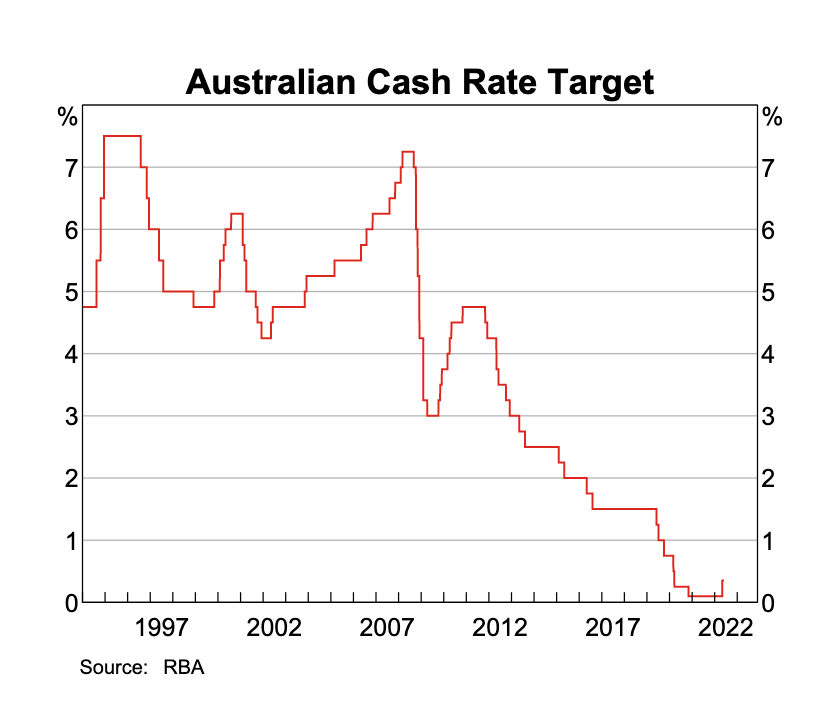

First and foremost, money is still cheap.

Whatever way we look at it, a cash rate of 0.85% is still ridiculously low.

The short term issue that our market faces is more about shock than financial pressure. For any buyers or property owners who have only been active in the market for the last eleven years, this is the first time they have ever experienced a rate hike. For the rest of us, however…. it’s not much of a shock. We remember the monthly merry-go-rounds of earlier years when it came to rate movements.

Shocks are often short-lived, and as people’s expectations adapt to our new norm, rate increases will become a cost of doing business and we’ll stop panicking about interest rates.

For now though, an obvious observation at the coal face is the impact of rate rises on first home buyer appetites. The lower-priced market in the sub-$800,000 category that would typically attract first home buyers, (particularly units and townhouses) has been rattled a little bit by plenty of first home-buyers who are hitting the panic button. Some are downgrading their budgets in an effort to factor in future rate increases, while many are now deciding to sit it out and wait to ‘see what happens’. On Friday we secured a superb boutique unit with courtyard on title prior to auction for a fabulous first home-buyer. Arguably this property should have had multiple bidders fighting it out, but timing-wise, this wasn’t the case.

In my opinion, our client was able to purchase advantageously due to rate-rise jitters.

The second driver for growth relates to employment. Our nation’s unemployment rate currently sits at 3.9%. While interest rates are now on the increase, job-security and employment is in the healthiest shape it’s been in a long while.

At our coal face, the difference between job security now versus 2020 and 2021 is vast. We are having conversations daily with prospective buyers who are feeling confident about their ability to borrow and their ability to sustain consistent employment.

Our conversations about job security and employment consistency were very different in the past couple of years.

The next driver relates to a difficult challenge we face, and I strongly believe it’s going to be the most significant future growth driver. We have a looming issue with supply. Currently, new listings aren’t looking too troubling. They are slightly down on previous years. All listings tell a different story though, as does all sales. We have come out of COVID lockdowns and the flurry of listing and selling activity was exacerbated due to a few factors; namely;

- Vendor confidence in price gains, (let’s face it… when vendors who are thinking of selling watch their neighbours getting record prices, it will tempt them to list and sell),

- Vendor confidence in avoiding lockdown disruptions

- Separation and divorce that was precipitated by horrendous lockdowns

We saw a large burst of selling activity, particularly in our lockdown cities in late 2021 and early 2022.

The volumes did calm down and are now seemingly restored to normal historical levels. It’s fair to say that there are still some opportunistic sellers on the market still who aren’t genuinely motivated and will likely withdraw their properties for sale in hotter market conditions. Listing activity doesn’t always match selling activity when we factor in these non-motivated, opportunistic sellers who missed the gravy-train.

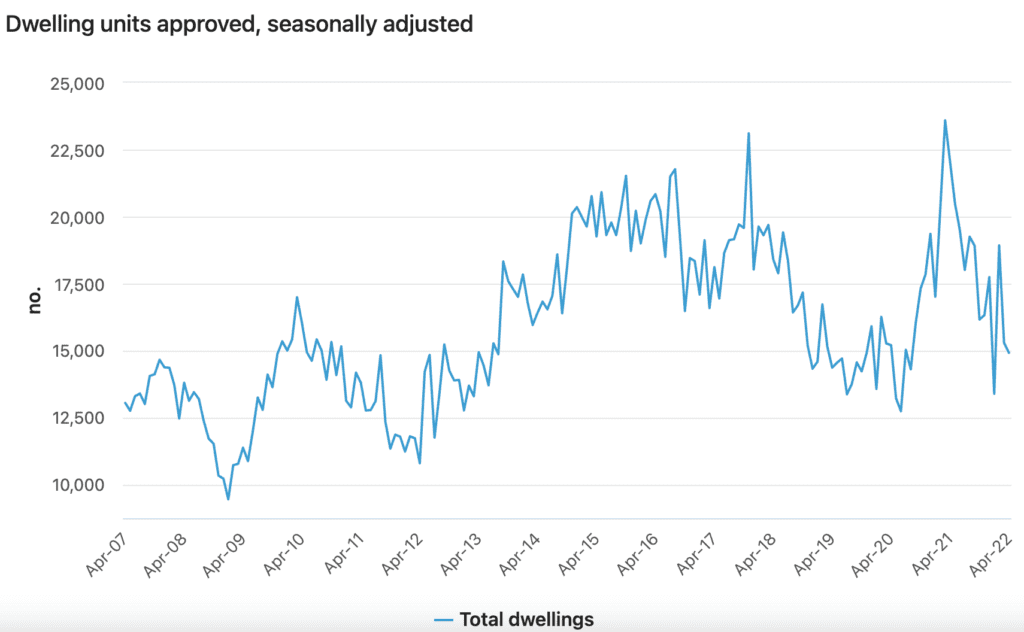

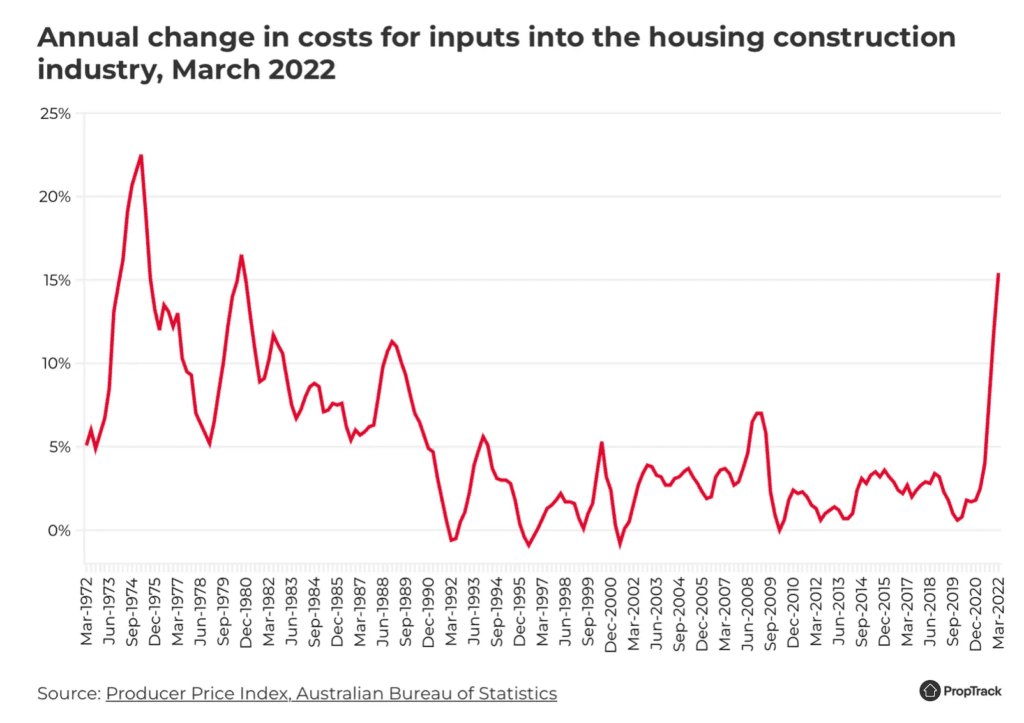

The key concern now relates to new builds and the slowing building activity. Traditionally we have used housing approvals as a leading indicator for new dwellings, but this is now less of a reliable indicator in today’s climate. Following the HomeBuilder-fuelled explosion of building activity, and unfortunately coupled with rising materials costs, supply chain woes and a tight labour market, our new building starts are clearly under pressure.

Building material costs and labour costs have soared. Fixed price contracts are flushing out some building companies, while delays, disruptions and start dates are hampering property owner’s plans to move in time. Buyers are placing a higher value on newly renovated, established stock, and for good reason.

At the coal face we’re seeing renovated, well-presented properties in good locations being fought over. Sales results for this category of dwelling are generally exhibiting growth still.

Buyers understand that picking up a renovation project is now a costly headache.

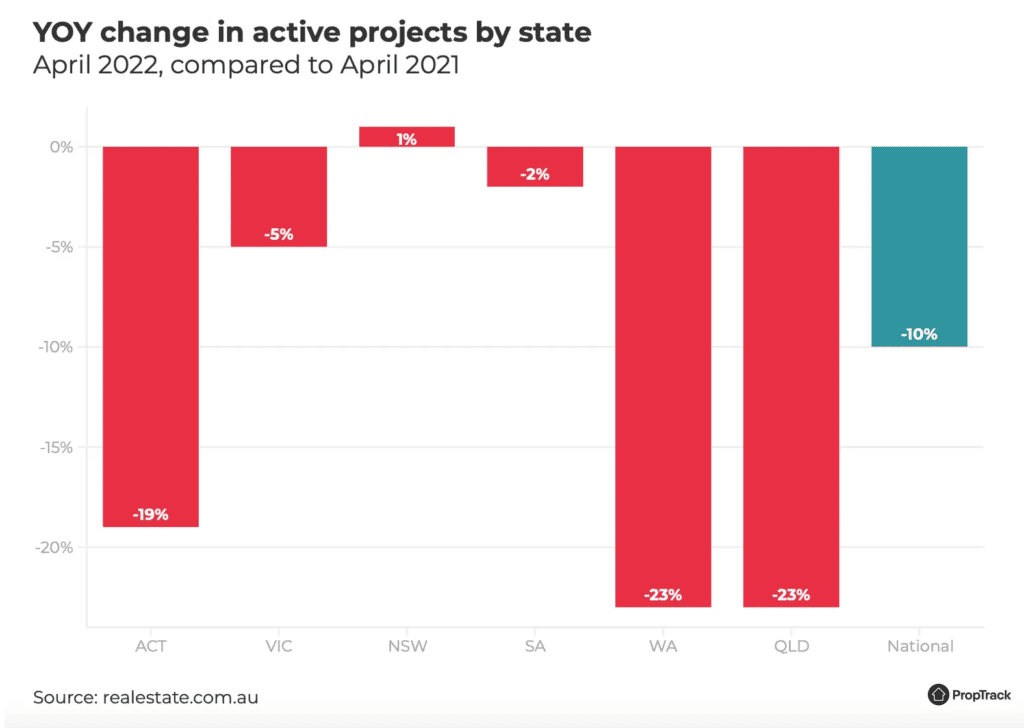

More alarming is the issue of short-term, future supply. Agents are now telling me that developer clients of theirs are opting to sell off their blocks with plans and permits, as opposed to pressing ahead with their unit construction. This is evident when an experienced buyer trawls through the property search engine and spots a significantly higher number of older houses/blocks of land being sold with plans and/or permits. If developers and land-banking owners are determining that a development is no longer financially feasible, we can expect that the ‘building approvals’ figure won’t correlate with new building activity figures.

In addition, brokers are reporting to me that many of their house and land buyers are now pulling out of their contracts prior to land titling and they are opting to sell the land. These buyers will no doubt re-enter the established housing market.

Supply is tightening and will continue to do so.

“Australia’s new home sales fell by 5.5% month-on-month in May 2022, following a 1.2% drop in the previous month, data from the Housing Industry Association (HIA) showed. It was the second straight month of decline in new home sales, amid a federal election and worries rising interest rates begin to bite. ” The impact of rising rates will be compounded by the going increases in the cost of construction and land, forcing up the cost of new house and land package. The lag from when a rate rise results in a decline in starts can be as short as six months, but in this cycle, it could be more than 12 months before the volume of starts fall due to the rise in rates,” Tom Davis, HIA Economist, said. (Source: Trading Economics)

We are navigating some headwinds that are likely going to naturally limit the supply of stock, and at the same time we will have an increase of new arrivals as our government tackles the labour force shortage.

The question looms; could now actually be an advantageous time while so many are ‘waiting to see what happens?’

It reminds me, (to a lesser extend) of when COVID first struck and so many decided to wait it out.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU