We’re all hearing news of interest rate rises… and speculation about capital growth contraction. But we do have to wade through headlines and negative news stories in order to see what is really happening.

COVID challenged every forecast and every lending economist’s predictions, and our selection criteria for property altered somewhat also. Some of these changes are likely to experience an elastic spring-back, while others will be here to stay.

What COVID impacted, however (and many would argue, negatively), was rental stock supply.

Following concerns about investor activity hindering first home buyer opportunity a decade ago, our prudential regulator tightened investor credit from 2014 and by 2017 it had ground to halt. Not only did our lenders have a particularly divided offering for owner occupiers versus investors, but the level of assessment scrutiny and heightened buffer rates just about eradicated the strongest of investor finance applicants.

Following the Banking Royal Commission and our surprise 2019 Federal election result, investor lending did open back up, but it was short-lived. COVID-19 struck just ten months later and investors recoiled. Our property market gains were hampered by lockdowns in many cities, Melbourne in particular and purchase efforts were difficult to say the least.

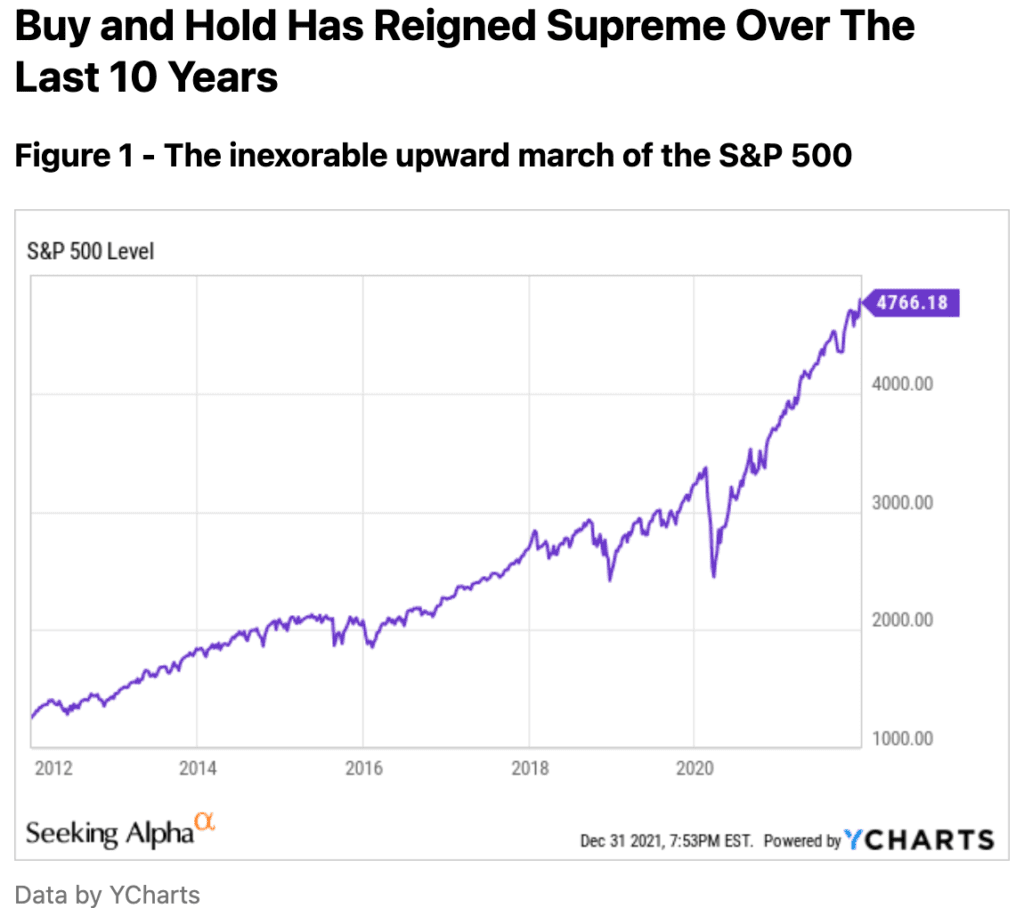

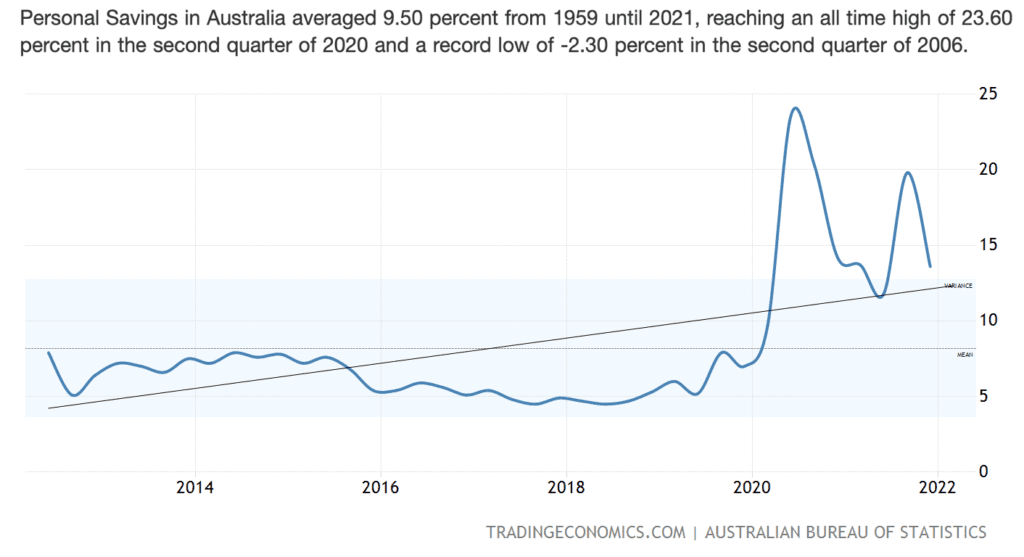

Interestingly, at this time a lot of people turned to shares. They had time on their hands, (particularly those in lockdown cities), they had additional household savings and they were comfortable to turn away from bricks and mortar.

For many, the resultant run on the property market, (even for Melbourne which recorded 15.1% in 12 months for 2021, despite six lockdowns and a total of more than 260 days in lockdown) came as a surprise. Economists had predicted horrible price falls and many buyers put their plans on hold in response to the grave forecasts. Some turned to shares, others turned to a tree-change, and many turned to bunkering down and saving.

Meanwhile, those who could escape the city did so. Apartments were vacant in response to the lack of demand from local tenants and international students, and disenfranchised landlords looked on in horror as asking rents plummeted and high rise asset values languished.

What happened next was intriguing.

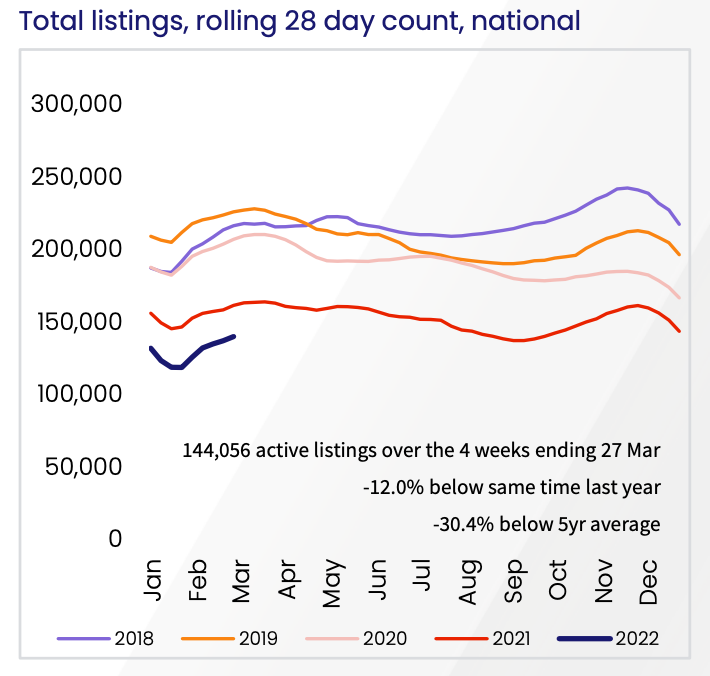

While our vacancy rates were high, our city’s total stock count was low. It seemed to happen very quickly; owner occupier buyers started snapping up the disenfranchised investor stock. Landlords listed and owner occupiers bought.

Suddenly our investment property pool was in decline.

At a time that investors were turning to shares, banks were still enforcing greater lender scrutiny to investors, and many households were focusing on upgrading their home or increasing the footprint of their floorplans, our rental market tightened.

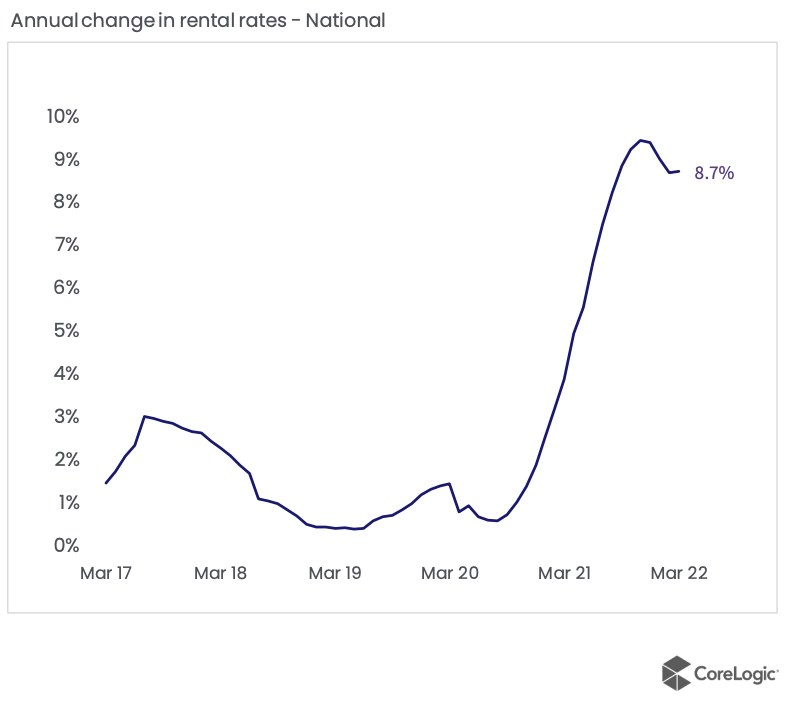

Even Melbourne apartments turned a corner quickly, and nation-wide, rising rents were making headlines. Vacancy rates are now at an all time low and for the first time in decades, gross rental yields have increased.

What is going to be insightful is the measure of second owner-occupier dwellings. Many households have embraced their sea-change/tree-change move, but buffered it with a ‘city pad’ purchase. Only time will tell when our 2021 Census data is released.

Now we find ourselves in an inflationary economy, talk of interest rate rises is incessant. Previously investors may have chased the capital growth dream and further convinced themselves that property is the right asset class now that rental yields are up, but jitters about the sharemarket and a desire to hedge against inflation are two considerable drivers for bricks and mortar. As this article in The Australian articulates, those investors who lock in a loan at today’s rate are positioning to enjoy the diminishing loan balance as inflation does its thing.

While it’s still not easy for investors to obtain a loan quickly, credit certainly is easier for investors compared to four years ago. The driving forces for investors into the Australian property market is six-fold:

- A taste of stellar capital growth over the last two years,

- Increasing rental yields,

- Tight vacancy rates, (which in turn removes concerns about vacancy associated financial losses),

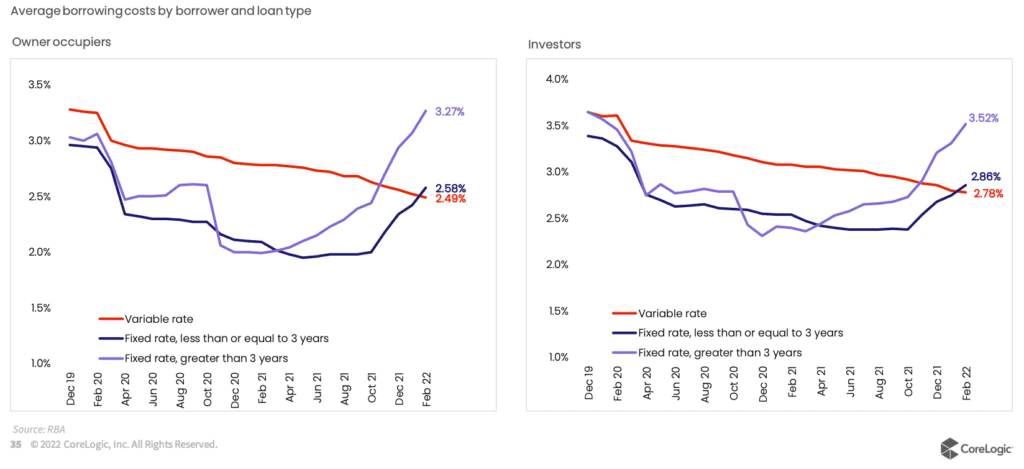

- Super-low interest rates, (and investors know that while increases are tabled, the forecasted rates are still comparatively super-low by historical standards).

- Diversification away from shares, and

- Hedging against inflationary pressures

After all, if inflation bites, yesterday’s loan balance diminishes.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU