Victoria’s performance has been lacklustre these past couple of years. It’s not surprising that people have compared the property market to the share market and asked themselves this question.

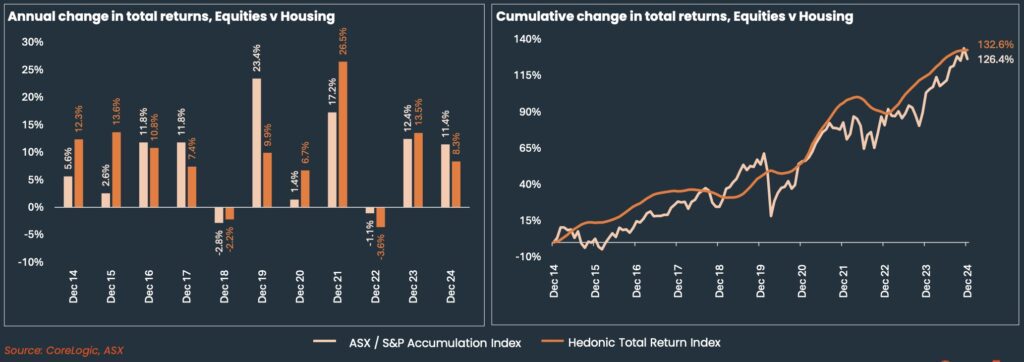

According to Core Logic, “When accounting for both capital gains and rental income, housing offered a total return of 8.3% over the 2024 calendar year. This equates to around three percentage points below the 11.4% return recorded in Australia’s equity market.”

To compound the blow, shares don’t attract maintenance costs, management fees, rates, insurances or land taxes. For a combination of reasons, but certainly this one, Victoria has seen a larger number of investor-led sales over the past two years.

Despite the compelling differential in returns, the past year doesn’t define the long term performance of the property market. There are some significant positives when it comes to property, as Core Logic reminds us;

“However, investing is a long-term game. While falling short in 2024, housing has outperformed equities in six of the past ten years and, cumulatively, has recorded total returns of 132.6%, around six percentage points above the 126.4% decade return of the stock market.”

Returns aside, there is another reason that gives property an edge.

Many people have written about shares versus property, (including the Property Trio’s Peter Koulizos), and the best financial planners and advisors will recommend a diversified investment portfolio. Stuart Wemyss from ProSolution wrote this fantastic article. Stuart describes the shares versus property debate as “meaningless”, and his reasons and comparison exercise support this.

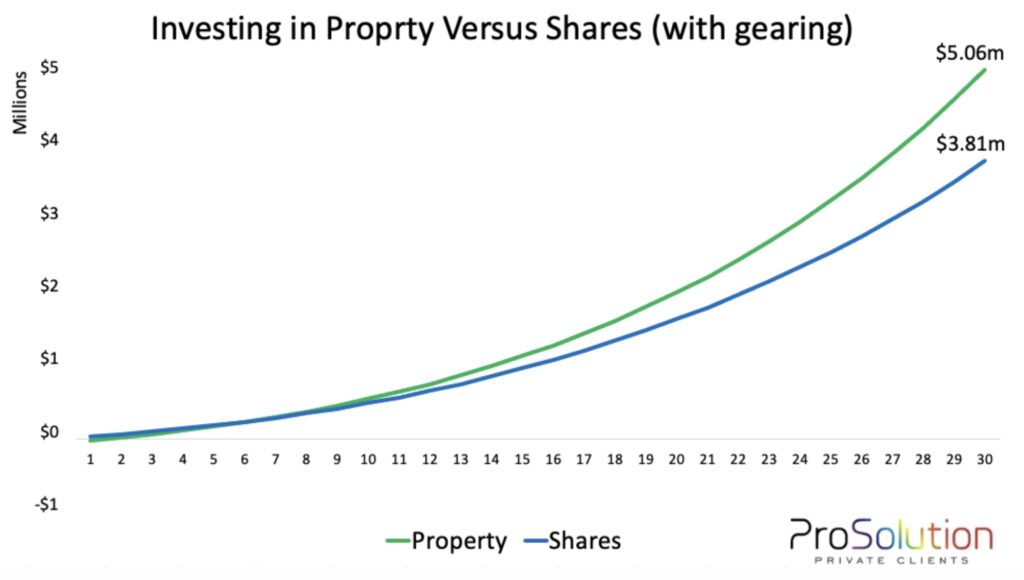

Stuart modelled two scenarios for the purposes of comparing the asset classes side by side.

Scenario One involves an investor accessing equity in their home* and drawing $5500 per month to invest over a fifteen year period. The rationale for doing this in tranches is well-documented. It is based on the relative volatility of the share market and it spreads the market timing risk.

*For those who don’t have property to borrow against, (or available equity to utilise), the amount of borrowings available will be lesser, and the interest rate will be substantially higher. More details below.

The second scenario involves an investor purchasing a $940,000 property and borrowing $1,000,000 to cover the stamp duty and buyer’s agent’s fees.

Scenario one’s assumptions are as follows: A share market return of “9.8% p.a., comprising of 3.7% of growth and 6.1% of income (this is based on the past 10 year performance of Vanguard’s growth index fund)*. Other assumptions include a mortgage interest rate of 6.5% p.a., a marginal tax rate of 39%.” (*Note that Stuart’s study was conducted in 2021).

Scenario two’s assumptions are as follows: “The property generates an initial rental yield of 3.2% and this rental income increases at a rate of 5% p.a. The assumed long-term capital growth rate is 6.6% p.a. (so that the total return is 9.8% p.a. – same as scenario one).”

The thirty year outcome is noteworthy, however we also need to factor in the holding costs associated with property. As Stuart points out, “You have an obligation to meet a property’s holding costs (from your salary or other resources), whereas the share strategy is self-funding (investment income pays for the interest costs).” We can also take into account the tax benefits (depreciation and negative gearing) and apply them to each model.

Overall, gearing is the key to this result above. The shares were purchased slowly over time, while the property investor’s million dollars was leveraged from day one. And Stuart points out that “The property strategy analysed above will be superior as long as the property’s average capital growth rate exceeds 5.85% p.a.”

So what happens when property doesn’t deliver an average result above 5.85%, year on year?

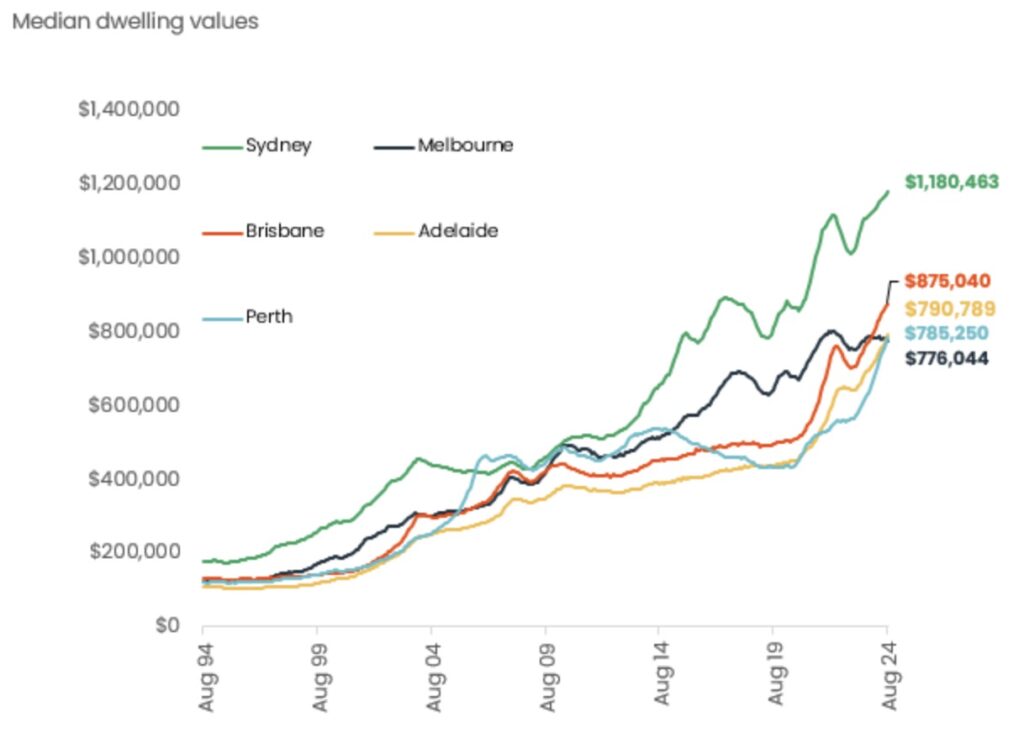

It’s a fair question, particularly in the current climate here in Victoria. However, it’s important to observe the longer term trends, rather than fixating on periods of downturn for individual cities. This chart from CoreLogic below shows thirty years of capital city median values.

Unfortunately, Darwin and Hobart aren’t included, but the ‘league ladder’ is important to observe. Individual capital cities, (and regional cities) do each have periods of relative underperformance.

According to CoreLogic in August 2022, “Nationally, dwelling values have increased 382% over the past 30 years, or in annual compounding terms, rising by 5.4% on average since July 1992.”

However, for capital cities during the period 1992 – 2022, it was the capital cities that recorded a higher growth rate. During this time, dwelling values rose by 409% and 294% respectively across each of the combined capital city and rest of state regions. Interestingly, it was Melbourne which recorded the highest growth of the capital cities during this time at 459%, (5.9% per annum). On the other hand, Perth recorded the lowest growth at 303% (4.8% per annum). (Source here.)

Pivoting back to the ‘Property versus Shares debate’, leverage counts for so much.

As mentioned above for Stuart’s scenario one, the borrowers who do not have an existing property to borrow against (or available equity to access), have less attractive lending options.

Typically a maximum LVR (loan to value ratio) will be around 70%. In this scenario, the investor would contribute $300,000 of their own savings and borrow $700,000. The margin loan interest rate is typically 3% higher than residential home loan rates also. The volatility of shares is often a concern for borrowers who have margin loans, because the lender can issue a ‘margin call’ at any time that the LVR exceeds the maximum limit. The borrower will have only 24 hours to do this, so maintaining liquidity is important.

Assuming the growth rates as documented above in Stuart’s two scenarios, the property investor who has borrowed 106% utilising equity, (or even 95% utilising mortgage insurance for their first purchase) will experience a superior overall capital growth return. This is purely based on the amount that they are leveraging.

In other words, the return on their initial investment will be amplified by the amount that they borrow.

The Shares versus Property debate is an old one, but like all investment decisions, the ‘best’ option is based on personal circumstances. Age, risk appetite, liquidity, retirement plans, cashflow and tax are all pertinent considerations. And of course, good asset selection is the clincher, combined with a long term hold.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU