I presented recently to a crowd of interested property investors and as I always find, the answers at the end of the presentation were varied and thought-provoking.

People often ask situational questions that give me an insight into what they are considering, what they’ve already signed up for, or what has perhaps frightened them.

It’s no surprise that one of the most common questions I receive at these nights goes as follows;

What is the best place to buy in?

And even if I wanted to give someone a short and punchy tip for assured growth, I’d be doing them a complete injustice without having any background knowledge of their personal situation. Most importantly, without understanding their why, my hot tip could not only land them in trouble but it could derail the lifestyle they ultimately want.

Property investment has so many moving parts to consider; it is never just a solution to deliver short-term capital growth.

Some of the worst strategies are founded on an unrealistic expectation of short term performance.

They include (but aren’t limited to) the following;

- Picking a ‘boom area’ on the basis of one exciting infrastructure project. If the project is shelved, reduced or moved, the boom town can quickly turn into a ghost town. Not only will the rental demand disappear but the equity position will likely be negative. The implication of this when obtaining finance for future investing is dire.

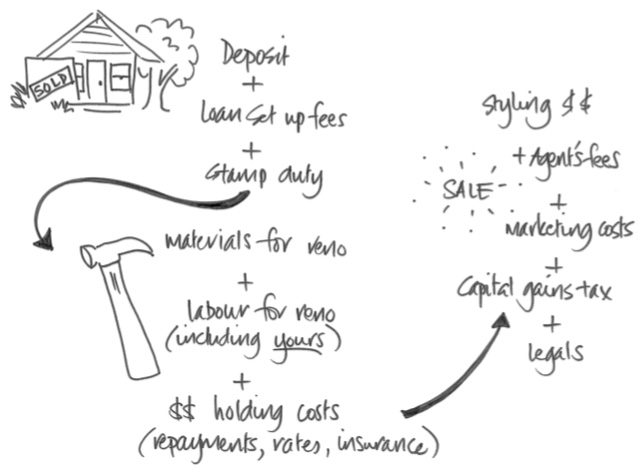

- Buying a house to do a quick-flip on. Some people manage this well, but the reality is that stamp duty, renovation costs, labour costs, financial holding costs (particularly when project delays strike), agent’s fees, marketing and selling costs, capital gains tax and legal fees all bite into any profits. In a positive trending market the profits are aided by growth, however in a negative trending market this strategy can prove to be a nightmare.

- Selecting a new subdivision on the basis that growth is imminent ‘because a community will be created’. Being mindful of the reasons why a new suburb will take off is essential. Is it based on desirability or affordability? Just because Bunnings is going in doesn’t mean that the area will sustain out-performance growth. Areas experience out-performance capital growth when the household incomes are trending upwards. When wealth comes into an area and heftier wallets are competing for property, prices will naturally go up.

- Collecting over a hundred properties offering positive cashflow. This strategy works for some but it’s not for the faint-hearted. One hundred properties spells one hundred tenants (all things going well!), and one hundred tenancies in a difficult socio-economic area can represent one hundred headaches. Being clear on the downside to such a strategy is imperative.

- Signing up for an off the plan property with a teeny-tiny deposit down. I can’t stress highly enough the caution that people should exercise with such a strategy. Imagine the stress levels associated with a valuation shortfall of over $100,000 when the whole reason for targeting the apartment in the first place was that only $1,000 was required as a deposit? Being told to find a magical $100,000 in the final month prior to settlement is a nasty shock for anyone, let alone a deposit-sensitive first home buyer. The percentage of valuation shortfalls adversely impacting off the plan apartment settlements is double digit in all of our capital cities.

Asking “What’s your why?” is the first question I start with.

Some investors what to build a passive income stream to sustain them during retirement and assist them into a phased retirement with choice and options.

Some wish to retire early on a strong income derived from sale profits (after tax is factored in).

Others like the idea of amassing a portfolio that organically dissolves all debt via strong rental returns over the years.

Many parents choose to do it to help their children. Whether it be teaching them pro-activity, handing them an asset in future years, or building an estate, the intent is there to provide for their children and possibly future generations.

Many parents choose to do it to help their children. Whether it be teaching them pro-activity, handing them an asset in future years, or building an estate, the intent is there to provide for their children and possibly future generations.

Me… I engineered a property portfolio for long term, future wealth and a passive income into retirement. I want to make sure that every day is lived to the fullest. Travel, time with my loved ones, happy times and making sure we’re able to get the education, health care and comfort we seek when we most need it is why I’ve invested in property.

Pending incomes, surplus cash flows each month, future expenses, desire to travel, and the time remaining until retirement, my advice will vary for every investor.

The two worst why’s are:

- because I want to make a fast and large amount of money, and

- because everyone else is doing it

Property investment needs careful planning, resources to actually do it, an adequate amount of time in the market, and a genuine reason.

What’s your why?

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU