In 2014 our prudential regulator, APRA issued a recommendation to our banks to slow down the rate of new investment loans being approved. Not until two years later did our lenders fully adopt the recommendations, but when they did; things got serious.

The methodology adopted included;

- a reduction of the maximum Loan to Value Ratio (LVR) for investment borrowers.

- a differential in the interest rate on offer between owner-occupiers and investors.

And then in 2017 we saw further efforts from our banks to slow investors, including;

- a restriction on Interest Only lending,

- an increased level of servicing commitments based on buffered interest rates, amortised loan repayment terms and calculations based on Principal and Interest repayments.

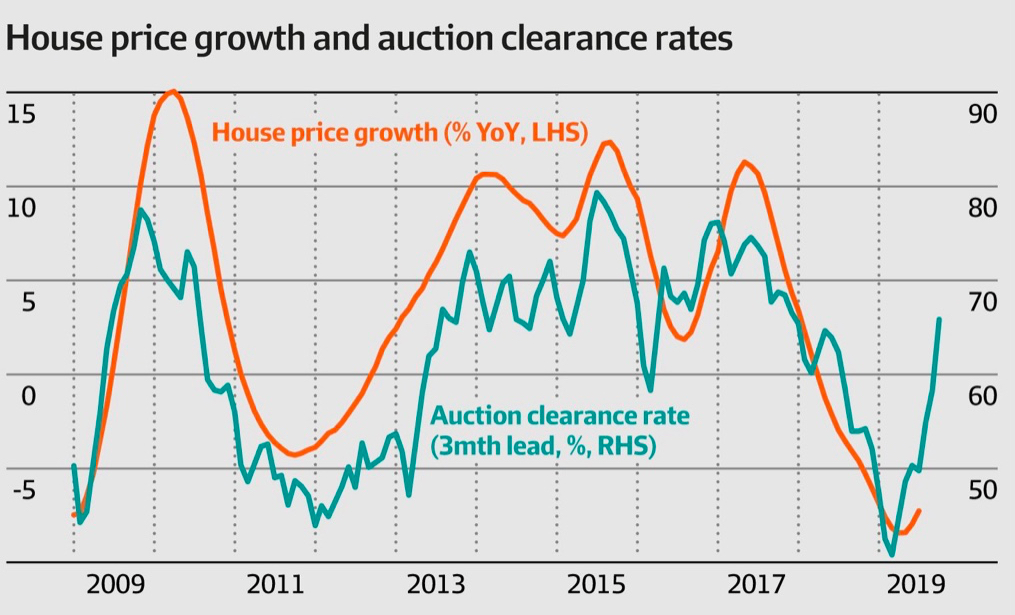

What ended up happening was possibly an oversteer on our regulator’s part. Our property market stepped into line with Sydney, (albeit six months’ later), and capital growth reversed form positive to negative in mid 2018. Auction clearance rates plummeted as our Spring market auction properties stockpiled later in the year.

Auction clearance rates in November and December were consecutively sitting around forty per cent each week.

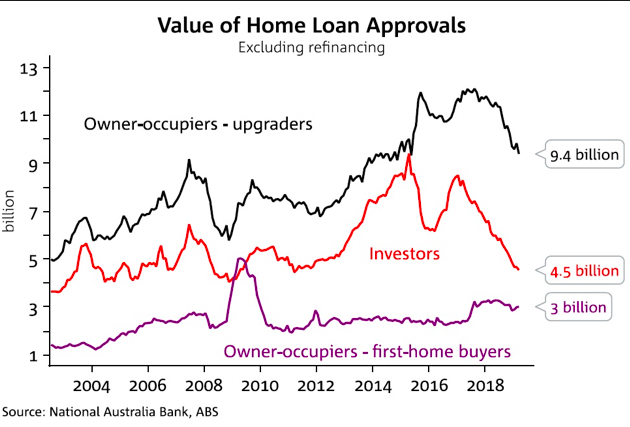

Investors had been largely chopped out of the buyer market, and pending news of a likely Labour Government with a mission to cut negative gearing benefits stifled any remaining investor activity.

Our new investment property settlements were extremely low and another challenge appeared.

Heightened lender scrutiny was no longer just affecting investor borrowers,. It was applied to all loans, and we could see lender approvals dropping in the statistics across all applications; not just investors’.

The only contingent who seemed to be getting a break were First Home Buyers.

We had a Banking Royal Commission unfolding and it wasn’t pleasant for anyone.

Loan assessment times blew out to weeks (as opposed to the former; which was usually days), and credit assessors were no longer able to apply discretion like they had in the recent past). Eligibility for lending became a rigorous and strict ‘tick-a-box’ routine, and clients who would have once had plentiful options, were restricted to one or two at best. Lending had become really difficult for most.

Some buyers went on hold. Many gave up.

The result of these challenges was a thriving rental market. Rents began to climb at a heartier pace than normal for Melbourne, and before we knew it our vacancy rate in the inner-ring suburbs had dropped to below 1.5%* (Source: SQM Research).

Vacancy Rate is an interesting measure. It is precisely the percentage of rented properties that are vacant and available for rent.

A considered and acceptable ‘normal’ measure varies between countries, but hovers around 5-7%. A figure above this signals a market that is saturated with available rental properties. A figure below this signals a market in tight supply of available rental properties.

Melbourne’s current lack of available rental properties, combined with our increased lender scrutiny (and reduced borrowing capacity for owner-occupiers) has cast our city into a tough supply:demand ratio when it comes to inner-ring and middle-ring rental property.

At the coalface, our rental open-for-inspections are experiencing a change. Tenant numbers have ballooned as a result of the supply:demand ratio and our scheduled advertised properties have queues of prospective tenants in attendance. Property managers are reporting strong numbers of applications, increased offers of rental payments above advertised rent on applications, and tougher conditions for tenants who have less-than-attractive conditions on their applications.

It’s become really competitive for tenants.

As Buyers’ Agents, we are seeing the rental demand for quality properties in real-time. One client of ours purchased this $935,000 period property in Yarraville and decided to price it at $600pw; some 10% above appraised value by a local property manager. We were confident he could achieve a higher rental, but we weren’t certain $600pw would be likely. It was achieved before he settled the purchase.

Another recent client inner-west who settled last week, (arguably at a time feared historically by landlords; in the depths of a Melbourne winter) and his managing agent had suggested an advertised rental of $525pw. We intercepted this and recommended a level of at least $550pw should be advertised. He received fourteen prospective tenants at the first open, and leased the property within 36 hours at a rental value of $550pw. His tenant has since moved in some five days later.

Our message to our clients, (and new purchasers) is to take into account recent rentals, and not to under-price their properties. Many rental managers are still being conservative, yet our house shortage remains a genuine situation, and landlords need to ensure that they are receiving commensurate rentals, in line with market demand.

Melbourne’s rental yields have been the lowest in our nation’s capital cities for a long time, but the market forces are now dictating rental increases.

Long-term investors need to have a serious chat with their property managers about market forces and commensurate rents if they haven’t done so already.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU