Lending has changed dramatically since I was a mortgage broker, (over a decade ago). Since the GFC we’ve experienced a credit crunch, a pandemic, a large number of first home buyer incentives, and a proliferation of online lending resources.

Banks have always traditionally provided their customers a pre-approval service, but pre-approvals are not what they used to be, nor are they equal.

Different lenders apply different protocols to their pre-approval offering and so many consumers are none the wiser, but when it comes to being purchase ready, plenty of buyers assume they are when they are not.

Lenders assess borrowers on a range of qualifications, including:

- ability to service (repay) the loan based on income,

- proven savings/equity,

- credit character, (past behaviour with credit),

- employment type (ie. reliability of consistent employment),

- residency status in Australia

Since our prudential regulator, (APRA) initiated tougher lending conditions for borrowers, and following our Banking Royal Commission, the lenders’ focus on spending habits has become very stringent. Credit assessors now pour over applicant bank statements and query every expenditure item, from Uber Eats to gym memberships, and everything in between.

The credit approval timeline for some of our major lenders now exceeds a whole month.

Nothing is easy about the credit application process, and buyers who assume that their pre-approval gives them adequate certainty to purchase unconditionally need be completely confident that the pre-approval they hold is a genuine pre-approval.

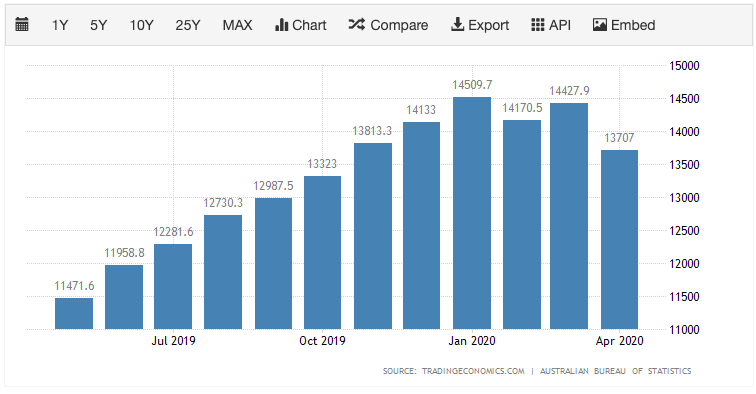

The above graph shows the number of loan approvals nation-wide. Pre-COVID our lenders were approving some $14B worth of loans each month. This number is vast, and many of our lenders have reconsidered their pre-approval process in an effort to optimise their output and profitability.

Many lenders have adopted an ‘indicative approval’ approach, where the credit assessment process is overlooked initially, and the applicant’s information provided is all that the assessment is based on.

In other words, a pre-approval is granted with a substantial caveat around it. The loan is subject to a formal credit assessment process, including employment checks, genuine savings checks and a credit score check, (among other elements).

If an applicant’s type of employment is not satisfactory to the lender, they may not become aware of this at the time of approval in principle. Likewise, if their credit history, spending habits or credit card limits sit outside of the lender’s tolerance or policy, they may not be aware of such limiting issues either.

Some lenders do still offer a full credit-assessed pre-approval, but it is a challenge to easily identify this without the help of a dedicated and knowledgable mortgage broker.

For those buyers who decide to deal directly with their bank, it is imperative that they understand whether their loan pre-approval has been fully credit assessed, and they must also be clear about any conditions outstanding. From requests to provide updated statements to compliance certificates on the purchase property, banks often have a list of requirements as conditions of their loan pre-approval terms.

And when it comes to auctions, there is no provision for a finance clause. Buyers must be confident, prepared and completely assured that their finance pre-approval is firmly in place.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU