I get this question so often.

An investor has, (let’s say) a $1,200,000 budget. They schedule an appointment to chat about their options and their strategy, and part the way through, the question pops up. Or, perhaps they as the question up front. Either way, it’s clear that they don’t yet have a strategy and it’s a perfect signal for their advisor to cut to the heart of why they are investing, and what kind of wealth creation strategy they should be paving.

It’s all about cashflow and how the debt is ultimately to be retired.

First and foremost, I explore the reasons why they are investing. This can come in all forms, ranging from;

- Amassing wealth via strong capital gains, (which will ultimately be crystallised when the property is sold one day in the future)

- Building up a multi-property strategy and retiring when the rental income can replace salary or wages

- Buying a future home and renting it for now

- Buying a child or a family member a future home/investment

- Buying because the accountant advised them to save on tax

- Buying to prove a point, or ‘because Sally from work did it’

- Altruism; to provide housing to someone who needs it at a discounted or free rental

- A defensive move; ie. to stop a neighbour/developer buying a property

Assuming the investor has strong cashflow and is keen to buy for the first reason above, (capital growth), the question of buying two smaller properties versus one larger one is redundant. In most capital cities and larger regional markets, it’s houses that have consistently outperformed units. Houses come at a higher cost, but they deliver stronger capital growth returns.

Take this beautiful beach side suburb in Melbourne as an example; Chelsea is home to over eight thousand people and is located 30km from the CBD and offers rail amenity on the Frankston Line. Chelsea has an eclectic array of housing, ranging from superb waterside houses and townhouses, to plenty of villa units and a few waterside apartments.

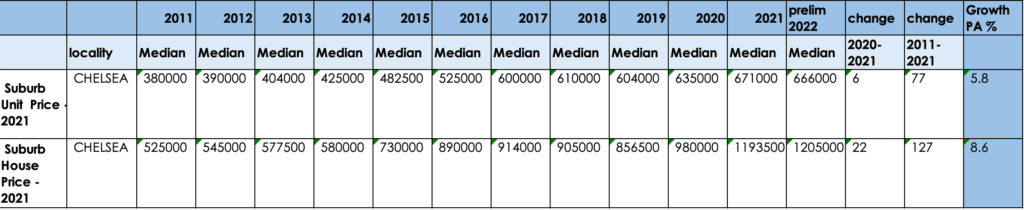

Our 2021 Victorian Valuer General ten year capital growth figures below demonstrate the differential between historical capital growth for houses versus units.

If this investor splits the $1.2M budget into two, they’ll likely purchase two villa units similar to this recent sale.

And if they target a house, something akin to this renovated character home is representative of Chelsea’s housing offering.

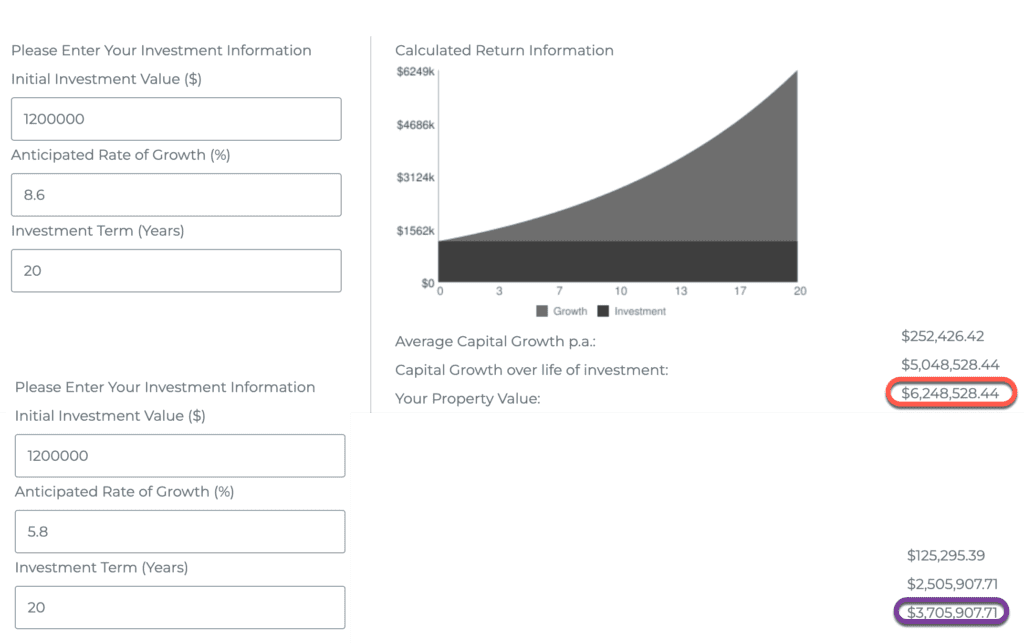

Based on the ten year capital growth figures above, the investor’s gain for the house option over a twenty year period is a dazzling $5M+. However for the two units, their gain is roughly half of this figure.

It sounds compelling to opt for the house, but the significant questions that every investor must ask themselves are;

- Am I reliant on a stronger rental return?

- Is my future borrowing capacity contingent on maintaining higher rental yielding properties?

- How do I plan to retire the debt, and when?

- What are the tax ramifications if my strategy relies on me selling the property one day?

To add context to these questions, it’s important to consider the rent, the maintenance, other associated outgoings and the likely tenant profile also. The annual rental return for the house is estimated (in today’s dollars) to be around $30,000, while the two units should deliver around $40,000.

When our investor considers the rental return between the two options, they’ll note that the unit proposition delivers stronger rental returns, and hence is easier on their cashflows. Not only that, but the unit proposition is likely destined to become cashflow-neutral at an earlier point in time, and the investor’s ability to organically retire the debt via channelling rent payments into their loan offset account will aid a ‘buy and hold’ strategy.

There is no right or wrong, but it is black and white.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU