I’ve met hundreds, if not thousands of investors over my twenty years in the property industry. Some are active clients, others are friends of friends at BBQ’s, parties, etc. People talk openly about investor regret when property is the topic of conversation, and over the years I’ve noted the common investor regrets. Here they are…

- Selling a good property for a modest gain and realising that holding it for longer could have yielded much more impressive gains

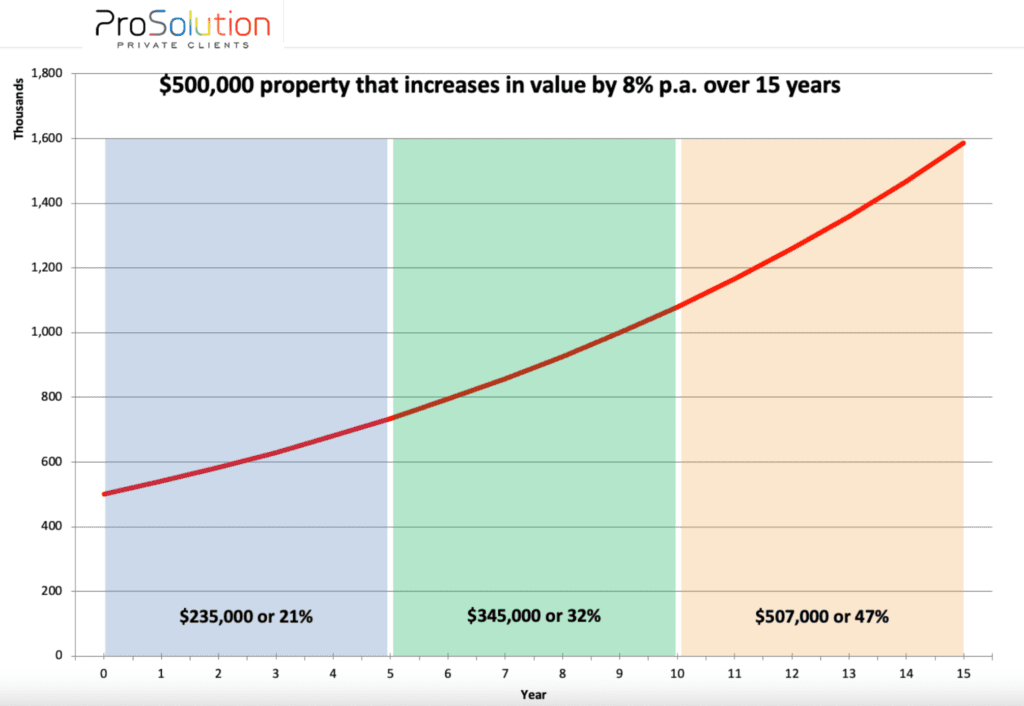

This is a mistake I sometimes see past clients make too. Property capital growth isn’t typically linear. Some years are strong, some are flat and occasionally a good property will exhibit negative price movement in a tough year. But over the long term, provided the fundamentals are sound, a good property will perform. One of my favourite charts is this one below, credit to Stuart Wemyss from Pro Solution.

The chart shows gains in the first decade. Sure, they are powerful, but the gains within the second decade of holding are substantially stronger. Compounding growth, however shows that each consecutive decade strengthens and the returns increase exponentially. Stuart’s chart maps out 8% pa returns, but even at a modest 5%, the message is the same.

Holding a good property for longer than ten years yields better results.

- Selling a good property because of a headache tenant or a headache property manager

This regret bites hard when the investor realises their mistake. Moving on a bad tenant is a challenging prospect, but with the help of a great property manager, this can be done. Bad tenants come in all shapes and sizes; non-payers, those who maliciously damage a property, those who breach their lease conditions and so on. It’s not always easy to identify a bad tenant at the beginning, but a good property manager can assist when things get tricky. Selling a good property because of a bad tenant can feel like a sense of relief at the time, but as the years tick by, it’s a hard realisation that a bad tenant got between you and an asset with strong potential. And if it’s a bad property manager that has an investor tempted to sell, then this may be an upsetting revelation. Switching property managers is easy. In fact, the new property manager can even do the break-up for you if its too awkward.

- Selling a good property to free up some cash buffers

This is a tougher concept to tackle. When finances (or fear about finances) bite, many singles and couples will opt to sell the investment property. It may be a move to free up cash for a renovation, or a holiday, even just to feel safer with cash reserves on hand. However, it runs counter to the reasons for investing in the first place.

Buying a property does require sacrifice and at times it comes with discomfort.

Working through the cashflows prior to the purchase is essential though, and discussion with a good strategic mortgage broker will help an investor map out some buffers for future events. These can include parental leave, study leave, family holidays, home upgrades and other investment activity. It hardly makes sense to invest in a property (and pay the associated duties and taxes), only to sell it with agents’ fees, marketing costs and capital gains tax bills a few years later. It should always be for the long term, and advice for navigating the stormy seas should come before purchasing.

- Not using an offset account

This is a sad little oversight that can become large in the years to come. Offset accounts cost a nominal annual fee and while the benefits may not be completely obvious at the start, they certainly are at the end.

There is a difference between redraw and offset accounts, and it is all about tax.

I’ve seen investors make this critical mistake and it’s cost them tens of thousands of dollars in the long run. More information about offset accounts can be listened to here.

- Waiting for the market to slow in order to ‘time’ the market

Just ask anyone who decided during 2020 to wait for the ‘drop’. Many of those buyers are still waiting for the drop now, while others downgraded their expectations and secured a property as the market experienced one of the headiest growth periods of the decade.

- Not doing anything

This is by far the harshest property regret. I’ve been investing now for more than half of my life and it’s interesting to talk to those who chatted about investing in my early days, but have still not actioned it. Perhaps they have purchased shares, or maybe they’ve channelled their income into retiring the debt on their home.

Years later though, the vast majority tell me they wish they’d done something.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU