Every buyer out there knows it’s a tough Seller’s market right now. The ratio of buyers per property is much higher than the historical average, and in the popular, established locales it isn’t a shock to see more than ten bidders making a play for a property at auction.

The problem with high competition in this asset class is that unlike some other asset classes, there isn’t more of the same identical product on the shelf. Only one of the ten aspiring buyers can take home the keys, while the other nine will miss out and experience emotions ranging from frustration to devastating disappointment.

Shares are different. You can still buy the share, it just may cost a bit more tomorrow if more people also want the same share.

Property can be so emotive, and particularly in this current environment we are in. It’s largely fuelled by owner-occupiers, as investors still only represent a tiny slice of buyers currently. The problem with emotive situations is that people can react very emotionally and this in itself can create issues.

What I’ve noticed of late is that emotional buyers are falling clearly into one of two camps. They are either so frustrated from missing out multiple times that they are bidding irrationally, or they are so despondent that they are entertaining disbelief, and hence rejecting the theory that the market pace is genuine and sustainable.

“It’s overheated. I’m thinking we should sit it out and wait for it to cool,” was one comment I received from a prospect yesterday.

I talked through his rationale. There wasn’t a lot of rationale to be frank, although he did hint at the threat of increasing interest rates. We explored this and I shed light on my thoughts about interest rate movement.

Despite what appears to be an aggressive property market bounce back following our COVID woes, our Reserve Bank has been very clear about the fact that they aren’t about to increase interest rates to combat the property market pace of growth. In fact, Governor Lowe in his latest RBA meeting even suggested that interest rates aren’t likely to start rising until at least 2024. This was a particularly notable mention, as forward ‘predictions’ like this are most uncommon in RBA meeting minutes. Sluggish wage growth and unemployment were two of the more pressing reasons to keep rates down, although international trade and commodity prices would no doubt be a key consideration too.

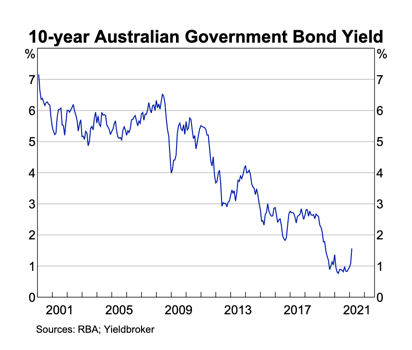

It’s interesting that one tiny mention about ten year bond yields can get journalists talking about interest rates rising, however. An uptick on this chart excited more than a few, and without drawing too long a bow, it’s fair to say that it indicates that long term we could brace for an interest rate increase. It’s hardly a startling sign, though.

The reality is that there are so many other troubling moving parts in our economy for our regulators and reserve bank to worry about before the property market. The interest rate cuts were made for broader economic reasons than the property market.

And the truth is; we have macro-prudential levers they can adjust if things start to bother them in the property market.

When we consider the two emotional camps of buyers, (and I’m not suggesting every buyer is letting emotion get in the way of sensibility; many buyers are remaining calm and focused). But for the two camps who aren’t, there are some concerning potential outcomes each camp must consider.

The irrational buyer who will win at whatever cost

We are seeing a lot of this. Only three days ago, I received an sms from the agent managing the sale of a property I was scheduled to bid at. The property was appraised at circa $1.05M by us. They received a knock-out bid of $1.22M from a buyer who had apparently got tired of missing out. The risk with a knock out bid like this is valuation shortfall and future exposure. If the lender isn’t of the same opinion as the buyer when it comes to value, the buyer must bridge the difference with savings in addition to their deposit, or forfeit their deposit and face losses. Going forward also, if the buyer (for whatever reason) needs to sell unexpectedly, they may find that they sell for less than they paid and incur losses.

It’s a dangerous strategy.

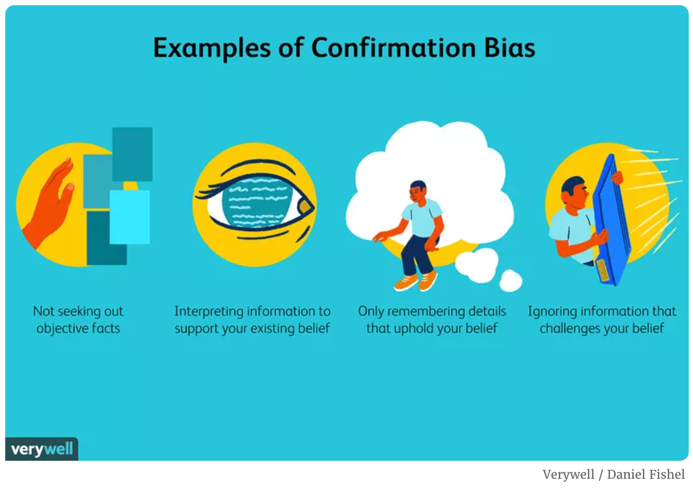

The disbelieving buyer who is falling prey to confirmation bias

These are the buyers who decide to sit it out and wait for prices to fall because they are so desperately wishing for this to be the case. Whether it be rising interest rates that cause the bubble to burst, or debt to income ratio charts that they find online, pointing to a downturn, it’s easy to find an article to support an angle. And nowadays with artificial intelligence influencing what appears in our newsfeed, we can find ourselves targeted with similar stories and viewpoints, even when we’re no longer searching for them.

Searching for an angle, while dismissing evidence and fact is known as confirmation bias. This has caused people to make decisions that haven’t necessarily served them well financially, and we all know people who have taken bold risks (or refused to take any risk) and are now wishing they had been more willing to take stock of the facts.

I recall buying a property direct from a vendor in late 2008. The GFC had struck and he was convinced that the bubble would bust and values would plummet. He sold his home at arguably, one of the worst possible times in a fearful market. I bought the property for a negotiated price, and we all know how the property market in 2009 went. Much like 2021; after our government over-stimulated the property market and at the same time, dropped interest rates dramatically.

This morning I read my friend’s article and sent him a quick message to say “snap! I was planning on writing about a similar topic”, so thank you, Tim Boyle for sharing two amazing insights I’m borrowing.

As much as I wish it wasn’t true, I too believe that these heady months of rapid price growth are here to challenge us for a while. The powerful trifecta includes:

- super low interest rates

- upturned buyer sentiment with an overwhelmingly large portion of buyers in the owner-occupier category; a more emotional catchment indeed

- a supply and demand imbalance favouring sellers

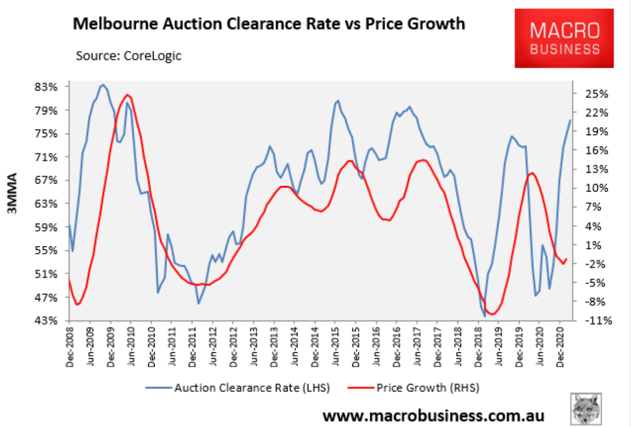

The RBA chart from this Macrobusiness article shows what can only be described as a compelling correlation between auction clearance rates and price movement. It starts by capturing the crazy growth in response to the GFC stimulus we remember Kevin Rudd declaring in 2008. It shows the heady value increases through 2013 to 2017 when auction clearance ranges happily sat above 70% on most weekends. And it illustrates the depths of our 2018/2019 downturn once credit was strangled, Banking Royal Commission loomed and the Federal Election threatened to scrap negative gearing.

What it doesn’t yet show is Quarter one for 2021… and we all know what that red line will look like. The blue line preceding it is the indicator.

“Price growth is running at around 16% annualised and this is reflected by auction clearances in the high 70s. Nevertheless, auction clearances are also pointing to ongoing strong price growth.” – The Unconventional Economist

As mentioned earlier, I do wish the conditions weren’t so heated, but they are. We have to work with what we’ve got. Considering only the most recent comparable sales, overlaying capital growth on top of historical sales, and having a competitive stretch budget are all essential approaches now.

We must be prepared to set a record when we buy, because most properties are setting records every Saturday now.

Buyers have to consider the facts, avoid confirmation bias, and most importantly, weigh up the financial risk of bold bids.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU