As our treasured January hybrid-break comes to a close, this Sunday blog reflects on the most used, most valuable, and, (at times) the most overlooked formulae. Property investing is not always black and white, in fact it requires a blend of science and emotion, but when it comes to reliable formulas, here are my top five:

- Gross rental yield.

Too many people feel confused by this, but it’s simple to calculate and important to apply to any property investment decision because it ties in to cashflow. Gross signals an income or profit before tax and other contributions, so it is important to ensure that a decision to invest isn’t made solely on the magnitude of the gross rental yield. It is possible for an ill-performing property to have a high gross rental yield and a low net rental yield if the outgoings are too dramatic. A case in point would be a high rise apartment with hefty strata/management fees and/or special levies for issues such as removal of combustible cladding.

Gross rental yield is calculated simply by dividing the annualised rent by the property purchase price. For example, a $750,000 townhouse delivering a $460pw rental outcome would be calculated as follows:

In tandem with other considerations, ie investor cashflow restrictions, lender interest rates, outgoings/fees, taxes, vacancy rates and overall debt retirement strategy, this measure should always be front and centre of any investor’s rapid calculations.

2. Land value.

We often hear knowledgeable local agents touting “$5,500 per square meter”, (or whatever their suburb’s standard value range sits), but it’s not always helpful and it shouldn’t be a broad brush application when considering a property in a given suburb. While it’s not too difficult to calculate, we must remember that it’s approximate only, and varies widely pending other characteristics of the parcel of land.

For example, a north facing rear on a block is far more valuable than a south facing rear. Elevation and slope impacts desirability, as does the broad level of the block. Proximity to main roads, train lines, overhead power lines and flight paths can detract when it comes to land value, and nearby parkland, beach/lake, access to village, walking distance to public transport and school zoning can all play a part in bolstering up land value. We then have invisible things to take into account such as encumbrances affecting the land, eg. easements, overlays, restrictive covenants. No two blocks are the same so we do need to keep land value in perspective.

Even a professional valuer would have a challenge determining the land value of an established property.

Methods to calculate this range from the Summation Method, (subtracting the depreciated value of the dwelling and improvements from the sale price), comparable sales analysis of unimproved blocks, or sales of similar land parcels with low-value dwellings on the land.

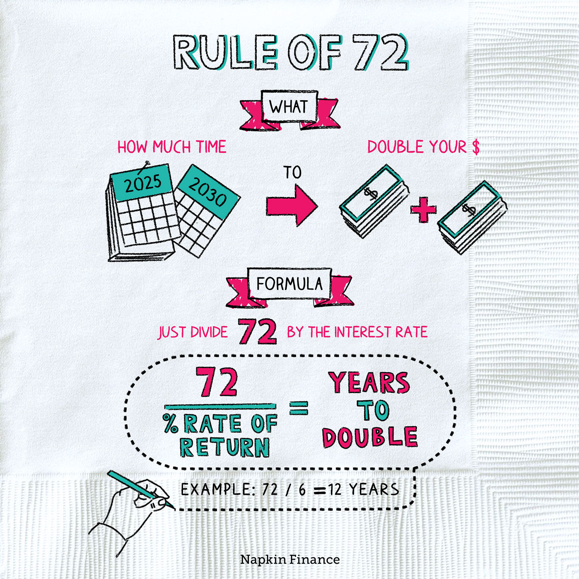

3. The rule of 72.

This is simple and easy, and originated from a 15th century Italian mathematician’s findings, Bartolomeo de Pacioli.

“The Rule of 72 is a simple way to determine how long an investment will take to double given a fixed annual rate of interest. By dividing 72 by the annual rate of return, investors obtain a rough estimate of how many years it will take for the initial investment to duplicate itself.” (Source: Investopedia)

This simple approach helps investors track the capital growth performance of their assets over the long term.

4. Land to asset ratio.

This measure is approximate in nature without the aid of an accurately determined land valuation and a quantity surveyor’s full depreciation report. All that aside, approximation is OK when it comes to this important measure, particularly when investors are weighing up the balance between capital growth prospects, rental yield and cashflow.

This measure is the most important and most applied for me as a property investment advisor.

Land to asset ratio explains why some dwelling types outperform others in the same suburb. It explains why some properties diminish in value in their early years, and it sheds light on why some landlord experiences are nothing short of frustrating when the land to asset ratio on their investment is too high.

I’ve written about, and talked about this measure in many forums, and this article dating back to 2015 gives some initial insight into the concept.

“Clients sometimes come to me with a brief commanding a brand new purchase; often reinforced by a well-meaning accountant or a financial planner who has introduced them to the idea of maximising tax deductibility and depreciation benefits. In their quest for saving some tax (and often tens of thousands of dollars are discussed), they neglect to consider the impact on the capital gain they could enjoy over the long term. The easiest explanation I can offer is that of ‘land-to-asset ratio’. If the land component appreciates and the dwelling component depreciates, then the investor needs to be confident that the majority of the value of the price they’ve paid is represented by the portion which grows. If they have targeted a sparkling, brand new dwelling, they can be reasonably certain that more than half of the price they’ve paid is represented by the dwelling component, and less so by the land. In most cases, the value growth is negative for around three to four years until the rate of depreciation of the dwelling slows enough to allow the land to start to catch up. A healthy rule of thumb is to ensure that the land component is worth at least 50 per cent of the price tag. An optimum land-to-asset value is closer to 70 per cent, where the quality of the dwelling (internally in particular) is still decent enough to attract a quality tenant at a good rental level, yet still dated enough to not be losing value at a faster pace than the land can grow at.”

“With this simple rule of thumb, an investor can avoid a negative growth asset that will likely disappoint in the early years when immediate equity growth is actually highly prized for a new portfolio.”

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU