Over the past two years, we have seen a marked increase in the number of Sydneysiders buying in Melbourne, but why?

Some have chosen to move for sheer affordability reasons. Some have continued to rent and live in Sydney, but have circled in on Melbourne as their next home destination. While others have contacted us to assist with an investment property purchase.

The first motivation is understandable. Sydney is expensive.

In June 2023, Tim Lawless from CoreLogic reported, ” In March 2020, at the onset of COVID, Melbourne house values were 19.2% cheaper than Sydney’s. By April 2022 the gap between Sydney and Melbourne house values had blown out to 30.3% – the biggest divergence since May 2006. The gap has closed a little since then however Melbourne’s median house value was 29.6% behind Sydney’s in May 2023, or the dollar equivalent of roughly $382,500.”

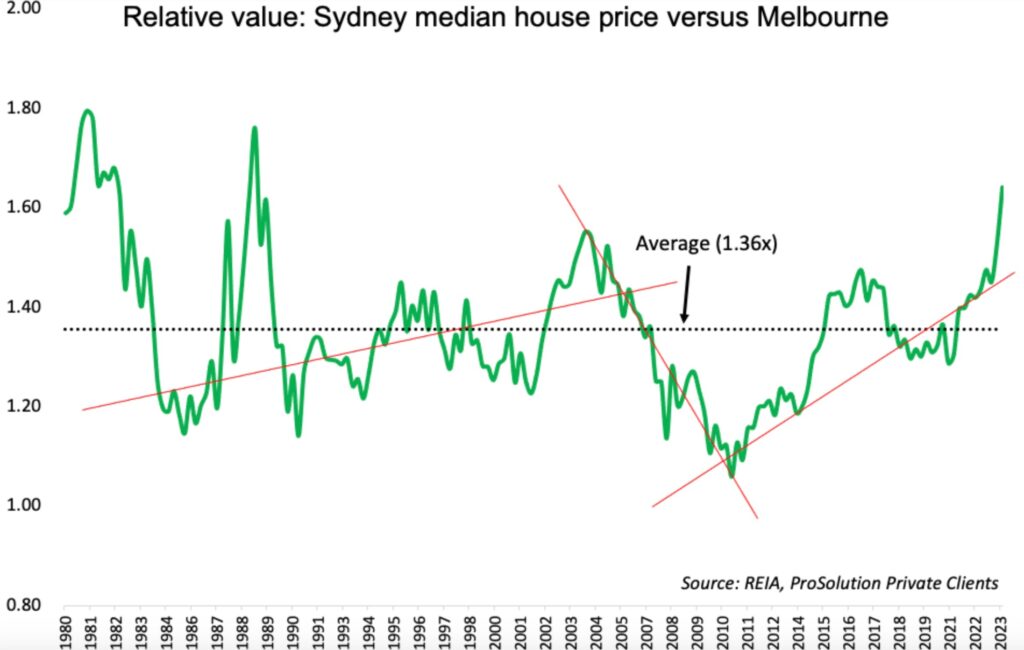

Late last year, Stuart Wemyss from ProSolution wrote a particularly compelling article about the disparity between the cities, and more so, some insights for investors to consider when selecting a capital city to place their capital into.This chart is thanks to Tim Boyle at Finalytics Financial, who featured it in his newsletter last week.

“The chart below illustrates Melbourne’s median house price compared to Sydney’s since 1980. Presently, Sydney’s median house price stands at 1.64 times that of Melbourne. Over the past four decades, the average price difference has been 1.36 times.”

“In relative terms, this macro-level data implies that either property in Sydney might be overvalued, or Melbourne might be undervalued, or perhaps a combination of both factors contributes to this discrepancy.”

Despite the pre and post 2000 Olympics price volatility, the last two decades have proven difficult for many Sydneysiders. It’s not entirely surprising that many have voted with their feet and decided to move, whether it be to regional cities or other capitals.

However, why would investors select Melbourne right now? The heightened temporary land tax rates, combined with onerous rental reforms have been front and centre in our newsfeeds for a while now. Investor sentiment hasn’t been great and agencies have reported a higher proportion of investor-led sales over the past year. Yet, when we look at the data, investors are still buying in Melbourne.

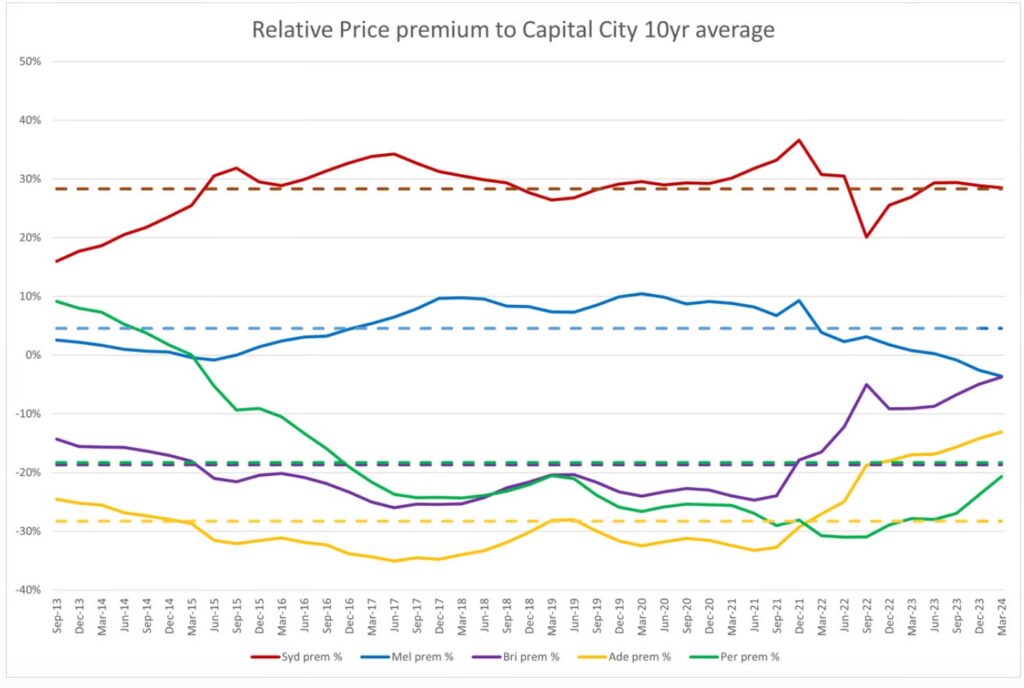

There are a few factors at play, and this clever chart grabbed my attention last week when Tim Boyle from Finalytics Financial featured it in his weekly newsletter.

The 0% is the baseline, which is the average national capital city value. As Tim pointed out, “Sydney usually trades at a 28% premium to national market over this time frame (flat, dotted red line). Given that the Sydney line is sitting on the dotted line suggests that Sydney is fairly priced on a relative basis.

However, Melbourne tells a different story, (as do Brisbane and Adelaide, but for different reasons, and this is important). Melbourne has historically traded at a 5% premium to the national average, but currently it is trading at a 4% discount. This indicates that Melbourne is undervalued on a relative basis.

Investors are clearly recognising an opportunity. Some could argue that Brisbane and Adelaide’s recent outperformance places these two cities in the overheated category based on this chart. While Perth has delivered stellar results over the past year, it could also be considered that Perth still has more short-term growth potential. Of course, relative purchasing power parity is not to be considered a yardstick on it’s own when it comes to identifying capital growth potential. There are many factors at play that are affecting house price movement in any given city.

But it certainly is interesting when we consider the data over history.

There are more reasons why Sydneysiders could target Melbourne for investment, and they relate to rents.

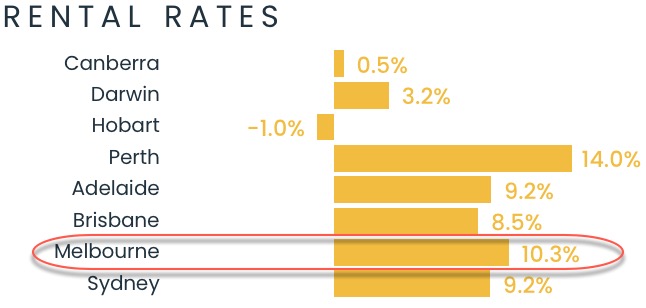

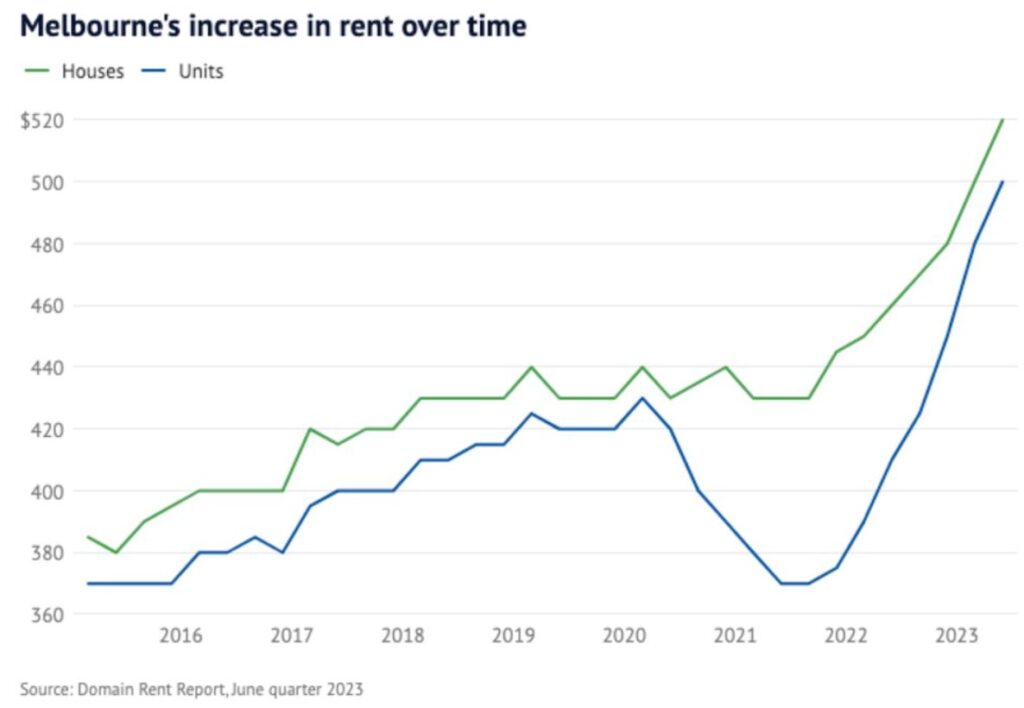

Over the past twelve months, Melbourne’s rents have soared. To further compound this, Melbourne’s rental growth outpaced most other cities during the previous twelve months also. The overall rate of rental growth in Melbourne since COVID has come off a low base, but it’s clearly outperformed.

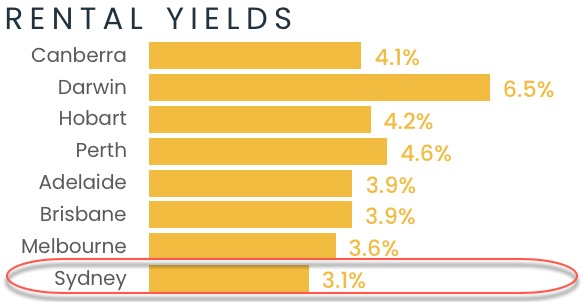

In addition, the gross rental yields have increased and no longer compare to Sydney’s. Historically, the differential between the two capital city’s rental yields has not been this large.

With higher holding costs due to higher interest rates, investors are calculating every penny, and looking at alternative opportunities where they can.

Lastly, and as Stuart pointed out in his article, investors are well-aware of the proposed migration numbers and associated capital city destinations. New arrivals need somewhere to live, and the pressure placed on rents (and house prices) is something they are factoring.

Is this trend of Sydneysiders buying in Melbourne likely to continue?

I think so, for all of the above reasons. Not to mention, the below.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU