This is one of the questions we often field. Is one significant property better, or is spreading the risk with multiple smaller properties more optimal?

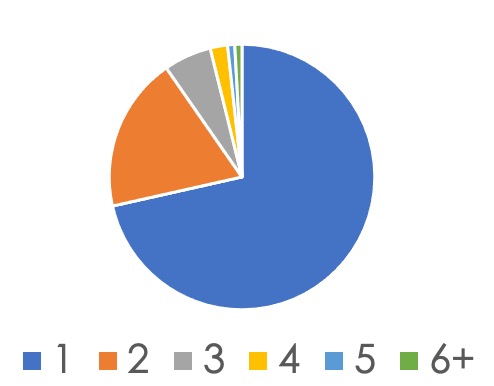

Firstly, let’s explore the reasons behind this question for many investors. Some like the idea of a property portfolio that they can count on two hands. We often hear people announcing, “We want ten properties before we are forty”, or “I’d like to buy one property each year.” Without a strategy or a basis for this, the exercise could create some issues of it’s own. Multiple property investors aren’t plentiful in Australia, and as this pie chart shows, the total percentage of those who own six or more properties is a mere 0.89% of our total investor population. In raw numbers, our last ATO collection of data registered less than 20,000 Australian investors in this category.

This equates to 0.00075% of Australians.

While this club might sound special, being a member of it shouldn’t dictate strategy. Personal goals and cashflow should be the determinant of a strategy.

Having a sizeable property portfolio to boast about isn’t the only reason why a buyer may wish to buy three, smaller properties with their $1.8M though. Some are limited to purchasing higher yielding properties due to loan servicing constraints. A lender may require a higher rental yield in order for the borrower to meet their cashflow requirements.

Other buyers hold concerns about diversification, and prefer not to put all of their eggs into the one basket.

And there are the investors who are mindful of the impact of land tax, (particularly Victorians). A lower-valued land component will ease the land tax burden.

There are plenty of reasons why investors favour the three-property scenario, but is it the optimal strategy?

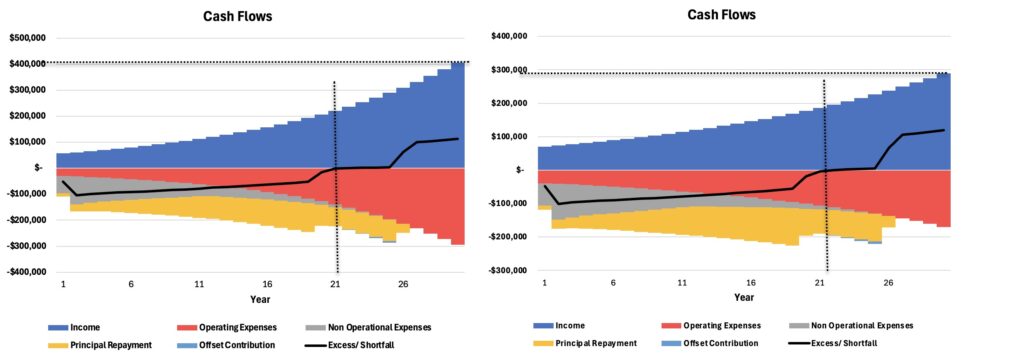

Cedric Janvier completed an internship with us recently. Cedric has just finished his third year in his accounting degree and modelled a detailed cashflow calculating tool within our business. His model includes the impact of offset account utilisation and takes into account all of the varying outgoings, from strata fees to land tax, operating and maintenance costs, and depreciation, to name a few.

We modelled this very scenario, with Strategy 1 representing a $1.8M acquisition of one, well located, free standing house. Strategy 2 represents three $600,000 units, also well-located but delivering lower overall capital growth. Our growth assumptions are 7% year on year for the $1.8M house, and 5% year on year for the units. Rents have been input as follows;

- Rental income of $1100 per week for the house, and $450 per week for each unit.

- Rental growth is also modelled on the same rates as the capital growth inputs. It’s important to note that rental growth and capital growth doesn’t often move in sync, but over time the gross yield typically oscillates within a band (2-4% for houses and 3-5% for units).

While these estimates are simplistic, the model itself shows the significance of this rental growth when the charts are compared, side by side.

It’s forgivable to assume that the units will become cashflow neutral at an earlier date than the house, particularly given the rental yields are higher in this example. However, as the chart shows below, the point of neutral cashflow is marginally earlier for the single acquisition. The cashflow is superior at the onset for the multi-property investor, but over time this benefit erodes.

More importantly, the income at year 30 is far greater for the house.

This chart below shows the equity discrepancy for the two scenarios; a noteworthy differential at year thirty.

This modelling takes into account the land tax, strata fees and all associated rates and insurances.

A significant burden that strategy two incurs as the years move on relates to maintenance costs. While strategy one bears the brunt of higher land tax, the impact of the maintenance as the properties age claims some of the returns for the multi-property strategy.

The debt-retirement plans play a crucial role in any investor’s decision too. From divestment timing to buy-and-hold status, tax related decisions and lifestyle, it’s not just about cashflow. but cashflow counts for a lot.

It’s a compelling discussion, and one that requires some serious consideration before the investor decides their investment strategy.

Special thanks to Cedric for this impressive model. We look forward to sharing some more scenarios!

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU