We get this question often. Prospective property investors typically focus on the amount of funding that that they may have at their fingertips, closely followed by the number of properties that they could buy.

So many make the incorrect assumption that more properties in their portfolio equate to greater wealth.

The reality is; every property investor’s journey must be different. Some investors are able to achieve strong capital gains as a direct result of heightened borrowing capacity and an ability to sustain higher out of pocket contributions, while others may not have the ability to manage the negative cashflow, or may not have sufficient cash or equity to purchase in a more expensive area.

While this is a generalisation, it is fair to say that outperformance capital growth often goes hand in hand with negative cashflow.

There are certainly regional cities and dwelling types within our capitals that have delivered attractive cashflow and capital growth, but they aren’t always easy to find, and a long-term growth trajectory is not always a guarantee.

So, when a prospective investor asks us, “should I purchase one significant property, or two smaller properties?”, our answer is inevitably;

“It depends. Tell me more about your circumstances and what you are trying to achieve.”

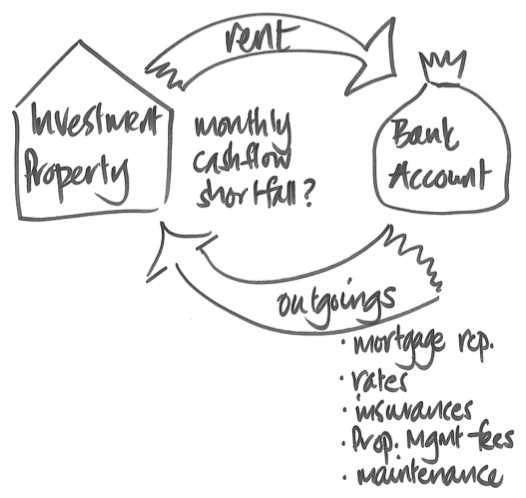

If an investor is focused on winding down their employment, either retiring imminently or scaling down their paid employment for other reasons, we need to be sensible about the amount of debt that they consider, and in particular, the cashflow shortfall that they could sustain. We also need to work through their ability to retire the debt and ultimately retain an unencumbered property.

The option to purchase with more aggression does exist for this category of investor, but they will likely need to consider the impact of triggering a sale event near to the time of ceasing their employment, and this does carry a degree of risk.

No investor wants to trigger a sale in a soft-market, however no aspiring retiree wants their retirement plans delayed by an investment property.

The truth is, investors who can sustain a cashflow shortfall, who have appropriate buffers in place for a long term buy-and-hold strategy, and have time on their side, do very well when it comes to sensible property investing.

If we circle back to the initial question, “should I buy one significant one, or two smaller ones”, there are some important points that should be considered when facing this decision.

Firstly, in Melbourne’s capital city market when contrasting houses and units in like-for-like suburbs, houses have outperformed units consistently for over two decades. Our buyer demand for houses has outstripped that of units, and for several reasons.

- We have an oversupply of units, (particularly apartments) in many of our suburbs

- Owner occupier preferences are still for houses on land, despite the convenience and value that some apartments and units offer

- We have a relative abundance of land in our fringe areas, and new house and land packages are still comparatively affordable, particularly with the government incentives on offer

If an investor is aiming for capital growth in a capital city, they are better off (long term) to aim for a house, as opposed to a unit. What they do need to factor into their equation is the cost of ownership, however.

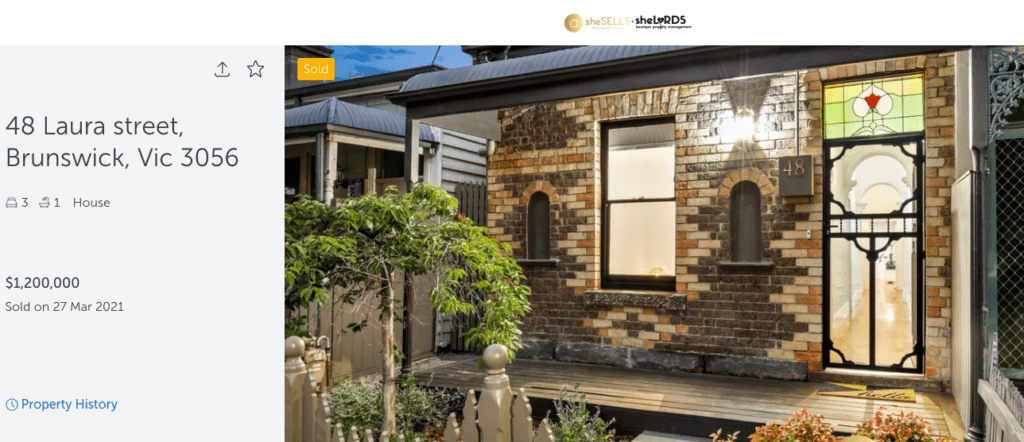

Take these examples below. The house will almost certainly outperform the two apartments when it comes to capital growth. Sure, the latter investor could say, “I’ve got two properties in my portfolio”, but if long term capital growth is what they are aspiring for, they may be disappointed in ten years’ time when the house has potentially doubled in value (working off 7% year on year capital growth), and the units have collectively exhibited significantly less.

The outlay is very similar; the sum of the two units is reasonably close to the sales price of the house.

However, the investor who is reliant on either neutrally geared cashflow, (ie. a net zero balance between the rental proceeds and the holding costs), or a property that becomes cashflow-positive in a shorter period of time will appreciate the latter scenario, (below).

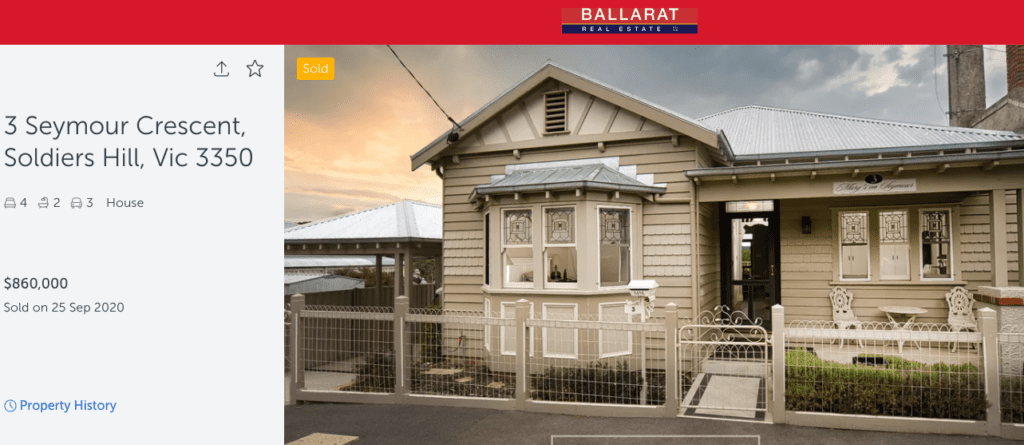

Deciding between purchase amounts and cashflow differences isn’t merely restricted to the capital city markets, either. Take Ballarat as an example; one of our nearby provincial cities within a 90 minute drive from our capital city.

A significant purchase in Ballarat could yield incredible capital gains if chosen well. This beautiful house in ever-popular Soldiers Hill is a case in point. The suburb is in high demand, offers incredible amenity and is home to some of the most magnificent, pretty houses in Ballarat. Land is scarce because the entire suburb is established.

By any investor’s measure, a purchase above $750,000 is significant, and well above the median house price of the city itself, and above Soldiers Hill’s median value of $665,000.

Investors should be cautious about targeting lower-than-median properties in the regions. While some such strategies can be fruitful, many can lead to stress and disappointment. Low socio-economic areas, dilapidated dwellings and broad house-and-land packages can be problematic.

Researching, familiarising with the area and talking to local property managers is a critical step for any investor targeting a region for value. Ballarat’s Wendouree is an interesting example; maps don’t obviously delineate between Wendouree and Wendouree West.

There is a significant value differential, and for a reason. While some investors may be comfortable with the latter, many wouldn’t be.

Balancing cashflow with capital growth is important, but rental vacancy, the profile of the tenant, and the maintenance required is a critical inclusion in any property strategy too.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU