I am often asked for my thoughts on properties that people are contemplating. Whether it be a BBQ talk, a call from a friend or an enquiry via my email from a prospective client, it happens quite a bit.

No property is perfect, but sometimes the imperfections are glaringly obvious at the first click, and I use the words “red flag” or “warning bell” when these types of properties land on my internet browser.

We speak openly about our avoidance of properties that the banks don’t like, but these types of concerns aren’t always obvious to the untrained eye. In addition to the threat of finance woes though, underperformance is our key concern.

There are multiple imperfections, and sadly we see too many examples of properties that are impacted by more than one imperfection. In fact, one of the worst categories of investment property we identify is not only in abundance, but mistakenly considered investment grade by those who grade the merits of an investment property on the magnitude of tax deductions the property offers.

Excessive tax deductions mean that the investor is sustaining losses.

To illustrate examples of properties that I’d deem red flag investments, I didn’t have to search very hard to find a few. They all had a lot in common, sadly.

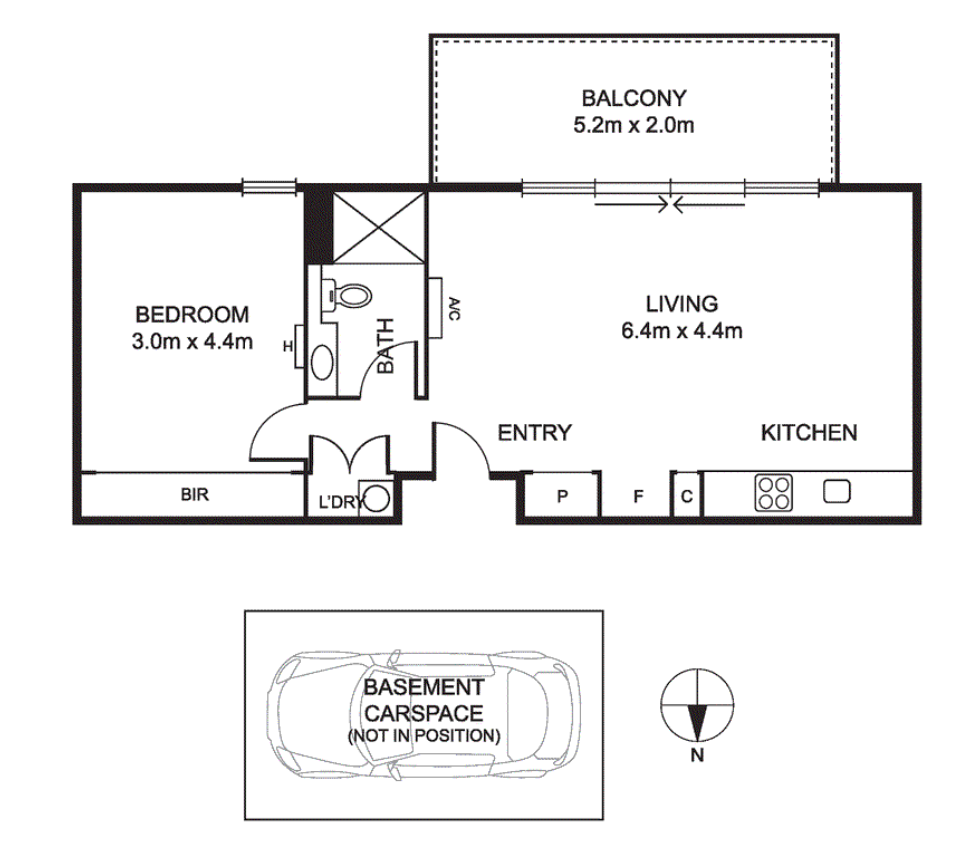

Take this suburban apartment as an example;

Boasting a busy street address, (noisy) being situated above shops, (coined by the selling agents as convenient, but flagging the potential for a zone we avoid at all costs), offering a tight internal living space, (often rejected by the banks at traditional lending levels), and being reasonably new, (or worse still, brand new or off the plan and hence delivering a low Land to Asset Ratio), this is a red flag property by almost every applicable measure.

For the investor, it spells disappointment and likely a highly regretful purchase. Not only would the rental journey be a challenging one, (let’s face it, finding a tenant who is happy to rent a tight space in a noisy location when other landlords in the same block are applying discounts to their asking rent isn’t all that easy), the capital growth journey is generally dismal at the beginning of the investment timeline.

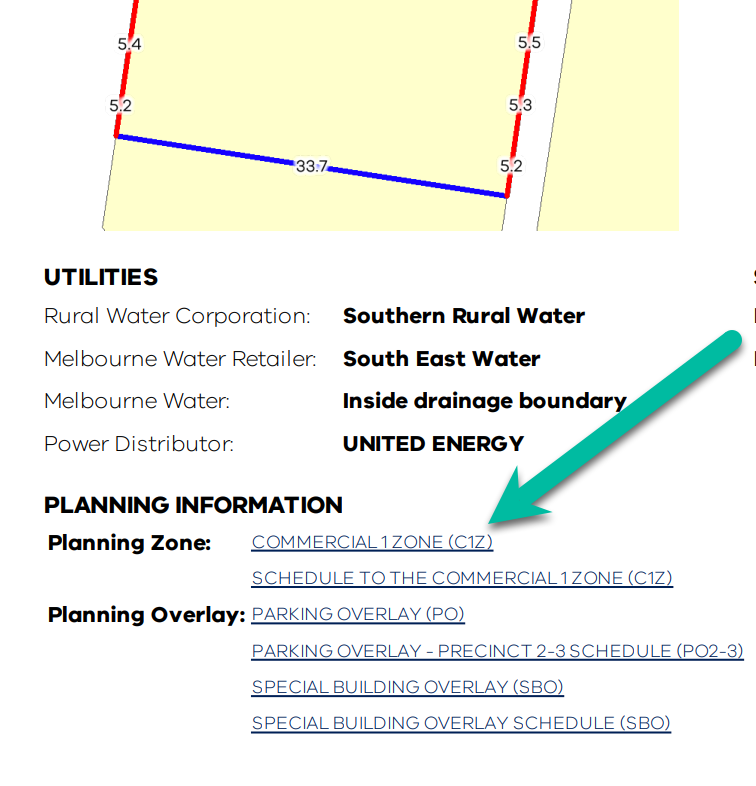

This particular unit in Melbourne’s south east demonstrates the negative impact of these imperfections. The property is smaller than the lender-preferred 50sqm (internal floor space, not car space, balcony or eaves), is on a busy main street with high traffic noise, is offering the unfortunate balcony orientation of south-facing, and lastly, (but most alarmingly),

This latter point is often argued by investors who are keen to get my approval for their purchase. Most buyers I chat to do not anticipate the zoning predicament, nor do they understand the implications of buying a commercially zoned property with a residential loan pre-approval.

“No, it’s not commercial. It’s definitely residential”, they tell me. “A tenant lives there. It has a bed and dining table, fridge and television. It’s definitely residential” they say.

Zoning is not necessarily matched to the end use, however. Occupancy permits can exist for commercially zoned dwellings.

The implication can be dire for some though.

if a bank loan pre-approval for a residential property is in place, it likely will not apply for a commercially zoned property. Some buyers may be eligible for a commercial loan product, but the repayments are far greater than the equivalent residential loan product. Firstly, the interest rates are higher, and secondly, the loan terms are usually fifteen years, not thirty years. The most frightening impact of a commercial loan, however is the deposit that it requires.

35% to 40% is a common deposit required for a commercial loan.

For the unfortunate buyers who unknowingly purchase a property in a zone that is not applicable for a residential loan product, they are often forced to relinquish their deposit and face legal costs associated with rescinding a purchase contract.

Not all buyers are eligible for a commercial loan, as the servicing rates often deem the borrower ineligible. The buyer pool for a property requiring a commercial loan is quite a lot shallower than a standard property.

It is for this reason that commercially zoned residences underperform and sell for less than comparable dwellings in residential zones.

We always check for zoning on the portal before circling in on a property. Anyone can access this portal and type in an address to check, free of charge.

The combination of these negative elements spells trouble for an investor;

- Low Land to Asset Ratio (applicable when a property is new or only a few years old),

- Small internal floor area

- Main road/busy road

- Commercially zoned

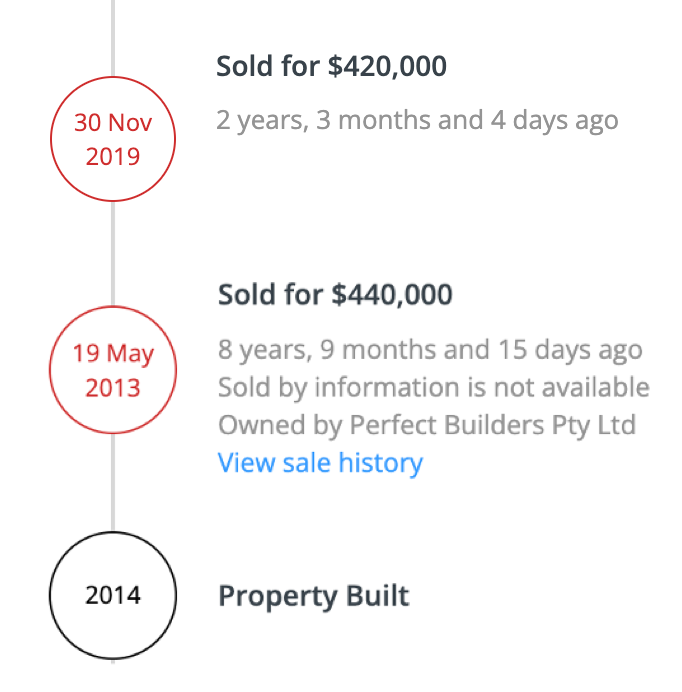

The investor journey for a sale of a property that sadly met all of these negative attributes is highlighted in the sales history for the unit. The history of the property is available in our paid portal.

Unfortunately for this investor, their brand new, off the plan purchase in 2013 resulted in Owner’s Corporation fees, rates, insurances, three sets of tenants, (including a vacancy period of 37 days for the first attempt to lease), and a capital loss some eight years later.

Not only did this investor lose money, but they lost a good opportunity to buy something that could have performed far better.

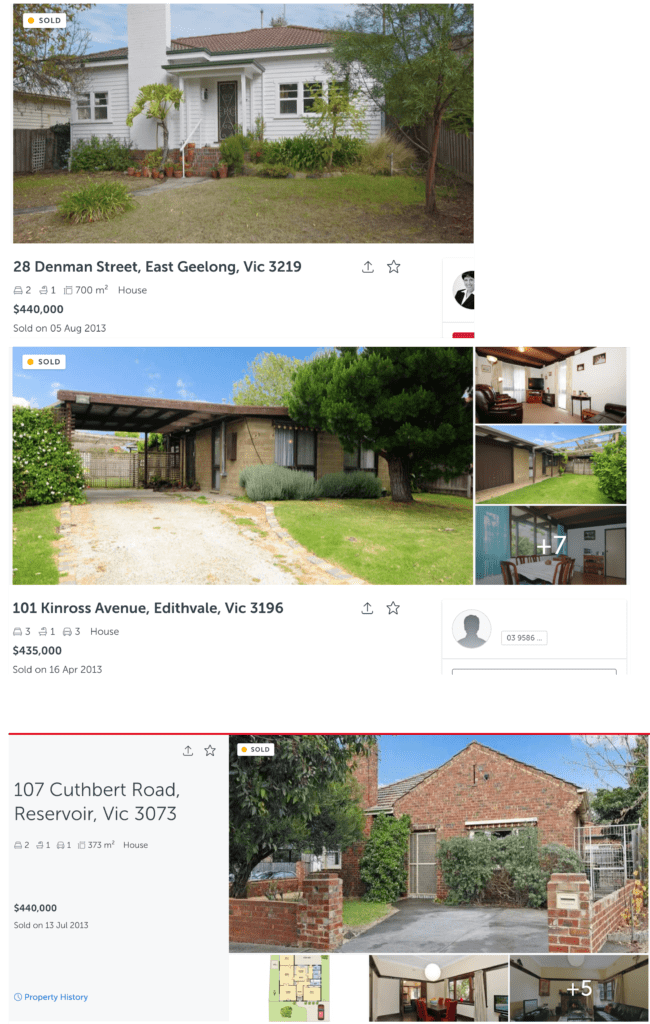

Some examples of more sound investment purchases for $440,000 in mid 2013 include these sales.

A stark contrast, when compared to this under-performing unit above.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU