It felt like a switch had been flicked yesterday when I was out in the trenches. Managing private sale negotiations and two auctions, this week felt different.

Competition felt stronger, buyer willingness to stretch harder seemed obvious and the change in sentiment since our COVID numbers have reduced feels palpable.

Could it be the media’s “bear-to-bull” reversal? Possibly.

Since bank economists have downgraded our price fall outlook, buyers have been emerging. This has been exacerbated by talk of the APRA loosening of the Responsible Lending Guidelines early next year. A relaxation of lender scrutiny will most definitely make a difference for borrower eligibility, and when we consider the cost of money now after our most recent Cup Day rate cut, it seems to make sense that more borrowers will be able to borrow more money.

“But what about Job Keeper?” people ask?

It is fair to say that there will be pain for some households who have been particularly impacted by all that COVID has done to businesses. But not every business has been negatively impacted by COVID, and in fact many jobs in various industries have been resilient; some in fact strengthened.

The question is; Will the magnitude of the positive impact of the loosening of Responsible Lending Guidelines outstrip the negative impact of our COVID stimulus packages coming to and end?

Sentiment is a funny thing, and we often see it hit like a tsunami. People like social proof, and it doesn’t take long at the coal face for the tide to turn.

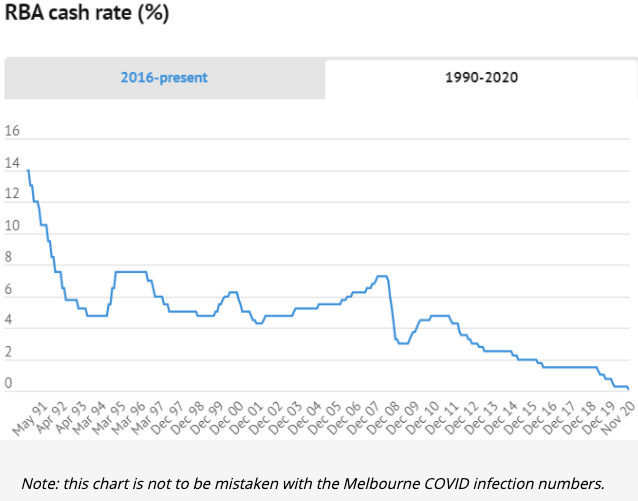

Whether it be the mere idea of the 0.15% rate cut, or the fact that we had a significant 0.25% rate cut back in March that we never really wanted to action back then, the truth is that our RBA have cut the cash rate to the lowest on record Australia has ever seen, (as shown below), and there is talk that it will not only stay low for a while, but we could even head into negative interest rate territory as other nations have done.

As Tim points out, we could be forgiven for looking at this as a COVID cases chart.

The combination of lower interest rates and tighter servicing rates for borrowers means that an applicant’s borrowing power is not only higher due to cheaper money, but it’s higher due to the bank calculating a smaller buffer.

For example, if a borrower has previously been eligible for a 3% interest rate with a 6% servicing buffer, a reduction of both servicing and interest rate will now result in a 2.6% interest rate with a 5% buffer. This translates into a substantial increase in potential borrowing power. Their eligible borrowings are calculated at only 5% pa and their mortgage repayments are now sub-3% pa.

Money is cheaper, and it appears that buyers are now taking heed of that.

Yesterday’s auction at 65 Canterbury St was a perfect example. I was bidding for an investor client and I was competing against three young owner-occupier couples.

I opened the bidding with $1.23M and in quick succession, two of my competitors took the lead and bid in ten thousand dollar increments against each other. As the bidding reached $1.3M, the listing agent ran inside quickly and sprinted back out with a quick “On the market, Nick” to his colleague. The bids continued, soaring past my limit and keeping the auctioneer and penciller busy. The hammer landed at $1.47M, some 13% beyond reserve and more than 10% beyond my appraised value.

After missing out at a mid-week auction in Coburg when this property at 36 May St sold over 27% above the top of the quoted range, I was justifiably anxious about the change in buyer sentiment.

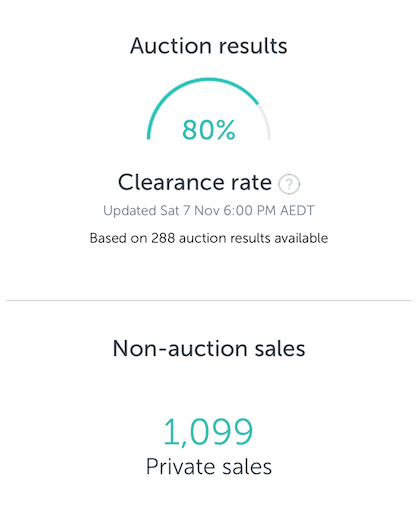

Yesterday’s auction clearance rate of 80% is still a limited source of a signalled change, because the number of auctions is low in comparison with a typical Melbourne Spring auction market, however it is one to watch, as is ‘days on market’, early market indicators and sales results.

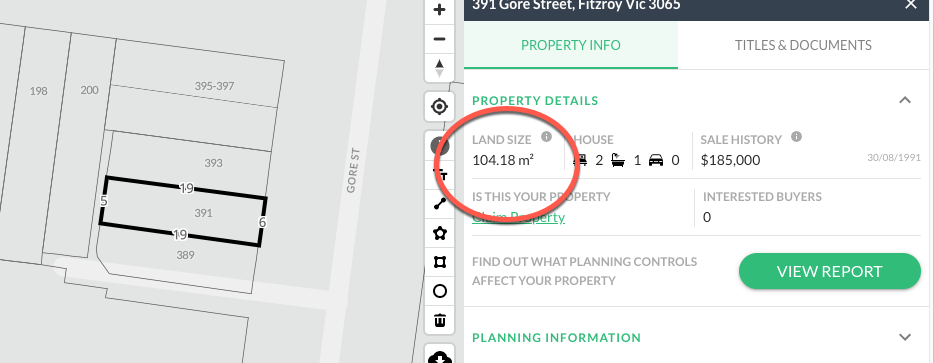

Thumbing through the auction results yesterday definitely demonstrated that some strong results, fuelled by competitive bidding were more than a few. This double storey terrace in quite rugged condition on a mere 105sqm shocked everyone when the hammer fell on a bid of $1.522M, nearly 40% above the top of the quoted range and reserve.

Presumably a jubilant vendor would have been celebrating this sale yesterday.

Whether this week has been an anomaly, or a sign of things to come, buyers are best placed to analyse the recent comparable sales carefully, understand the changed market conditions we’ve encountered since the Federal election and Australia’s first COVID outbreak, take into account the price fluctuations during these times and calculate their upper limits accordingly.

And fully credit-assessed pre-approval is not a recommendation, it’s a MUST.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU