There is no doubt about it… .2022 has been one of the most unusual years we’ve experienced in a long time, and that’s saying something since the craziness of 2020 and 2021.

However, five key things have enabled me to categorise 2022 as one of our most unusual. As we head into 2023, there is plenty of apprehension around capital growth movement as interest rates threaten to increase.

It’s actually a few less spoken about items that have labelled 2022 as one out of the box.

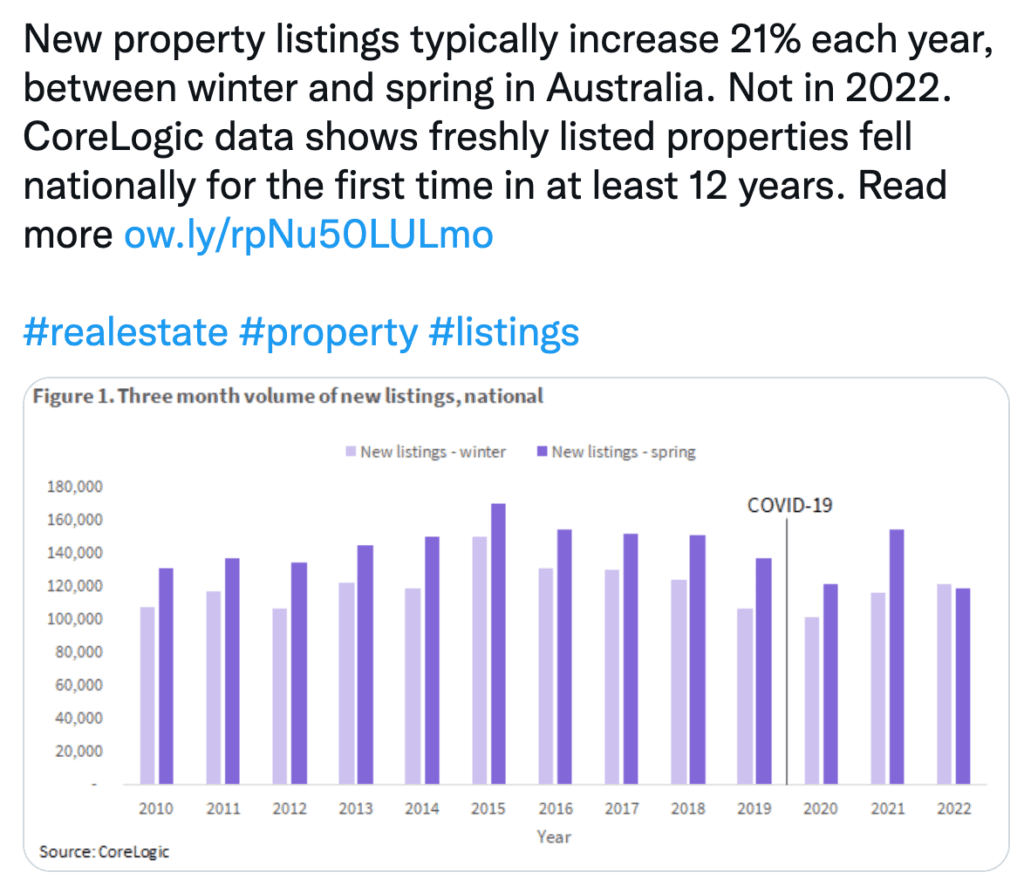

First relates to our seasonal pattern of stock levels. For the first time I can ever note, Australian property listings peaked in winter 2022 and eclipsed our spring 2022 levels.

The second point relates to domestic consumption and our resilience to interest rate rises when it comes to discretionary spending. While the RBA have acted with firm determination to reduce our rate of inflation by applying consecutive cash rate increases, the issue we’ve faced has been a hard one. Our extended lockdowns, (particularly in Melbourne) forced us to save. Our savings also helped us come out of lockdown with a renewed sense of living life to it’s fullest… termed YOLO if you will, (you only live once). However the specific items attracting the heftiest rates of inflation were the items we can’t really reduce our consumption of, such as fuel, transport, food and alcoholic beverages.

Hardly things we would “choose” to restrict.

We now find ourselves in a perplexing situation where we have a vital need for what is becoming more expensive, and our growing need is further exacerbating the problem as continued price hikes are applied (in line with inflation running high) and while credit supply is decreasing for many.

The third point is a sad one.

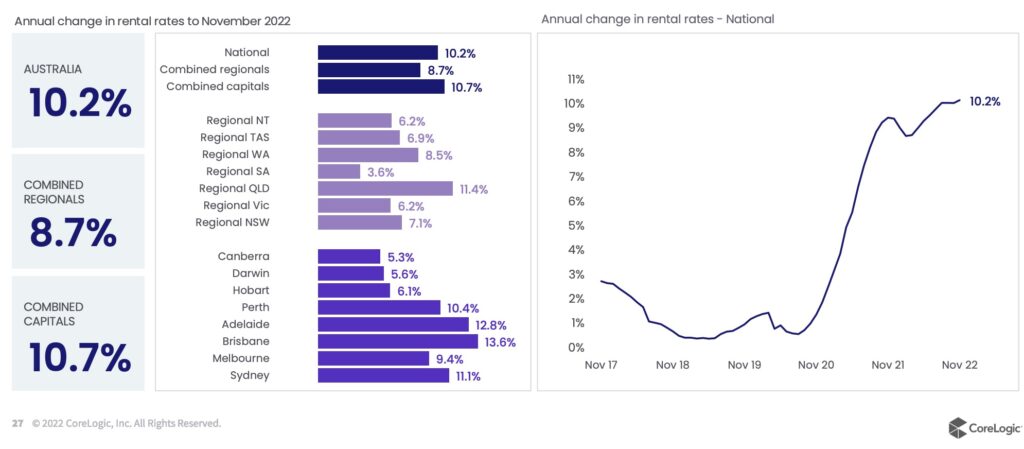

Number three relates to a rapidly declining rental pool and the harsh impact on renters in our nation. This is particularly challenging for those in regional locations and for much of the state of Queensland.

Declining rental stock is due to a combination of tough lender scrutiny and tight credit (particularly between 2016-2019) and tougher legislative control on rental properties. More recently, onerous rental reforms are disincentivising investors at a rate of knots. Queensland’s threat to land tax reform, (which was repealed earlier this year) unfortunately had a negative impact on stock levels in the sunshine state. This CoreLogic chart below illustrates the pressure on renters.

The problem is likely to intensify as investors opt to leave the property sector for various reasons. The top five reasons are:

- Surging holding costs, (particularly as interest rates have risen and fixed rates are coming off)

- Lack of control of their asset as government legislation continues to favour renters

- Increased expenses as rental reforms dictate tighter minimum/maintenance standards

- Tighter lending conditions for investors

- Baby boomers selling down investment to fund retirement

As rental stock depletes and new arrivals land on our shores, we can anticipate the tightened supply/demand ratio to continue to push up rents. Sadly, increased social housing investment won’t come close to solving the issue because our taxes and budgeting are insufficient for the government to aid the issue alone. Private investment is a necessity in our nation based on our current tax system.

Number four is all about elasticity.

We saw bosses commanding their troops to work from home in 2020 and 2021. Now many bosses are summoning their troops back to base, at least in a hybrid capacity, if not a full time capacity. We now have Melbourne inner-city units growing at a much higher pace than regional property; quite a shift from previous years. This is in response to many of our tree-changers and sea-changers opting out of their long commutes and setting themselves up with a city pad. In addition, we’re also seeing downsizers opting for a lower-maintenance lifestyle, close to transport and hospitals.

What this will do to outer regional markets is yet to be gauged.

Number five’s issue belongs to supply chain woes, builder shortages, labour shortage and the rapidly growing cost of materials. China’s continued lockdowns have hampered much of this supply and the war in Ukraine has impacted importation costs significantly. Sadly our construction costs and building timelines have blown out dramatically. This has forced a buyer preference towards newly renovated family homes, as opposed to renovator, new builds or development projects.

In fact, many builders and developers are selling their land-banked blocks at a loss, along with plans and permits.

And number six relates to interest rate increases, and the effect on both sentiment and actual borrowing capacity. The two don’t necessarily go hand in hand, and this is because some borrowers are impervious to borrowing capacity constraints, while others aren’t. For the borrowers who don’t need to borrow to their maximum constraint, (ie. those with cash surpluses, those who require smaller Loan to Value Ratios (LVRs), and those who are down sizing and aren’t borrowing at all), the recent rate increases bear no threat to their plans.

We actually have a multi-speed market, consisting broadly of the following contingents;

- First home buyers; who are utterly fearful of the unknown and are determining a reduced spend level of their own accord, (not necessarily what the lender’s are restricting them to),

- Upgraders who are throwing every bit of might at their upgrade plans, but finding that month after month, their limit is declining,

- Investors who are also somewhat caught in the crossfire of limitations to borrowing capacity due to lender scrutiny and tough cashflow calculators,

- Mature aged down-sizers who have neither a capacity constraint, but tough competition in their segment, and

- Business investors who are completely constrained in the commercial real estate space due to credit challenges.

2023 promises to be an interesting year. There is little doubt that our pattern of interest rate rises is not yet complete, however the questions around downward rate movements are alive and well. Short of suggesting that the RBA will backflip and reverse our rate movement, we also need to question three other possible outcomes;

- Will lender margin reduce under tough competition? After all, the banks are in business to lend money, and lending is significantly down. Margins have room to move and lenders will do what it takes.

- Will our regulator adjust the buffer rate to a lower level than 3% now that we’re much closer to what was deemed a longer term equilibrium level? With a buffer adjustment comes easing of borrowing capacity.

- What will an increase in the number of new permanent arrivals do to our supply/demand ratio?

…I don’t think 2022 is the last quirky year I’ll be writing about.

Bottom left: Emma, Cate, and Shannon

And my best tip….. be prepared to be nimble if you are keen to partake in the property market in 2023. Things could pivot fast.

Wishing you all a safe, happy and prosperous 2023!

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU