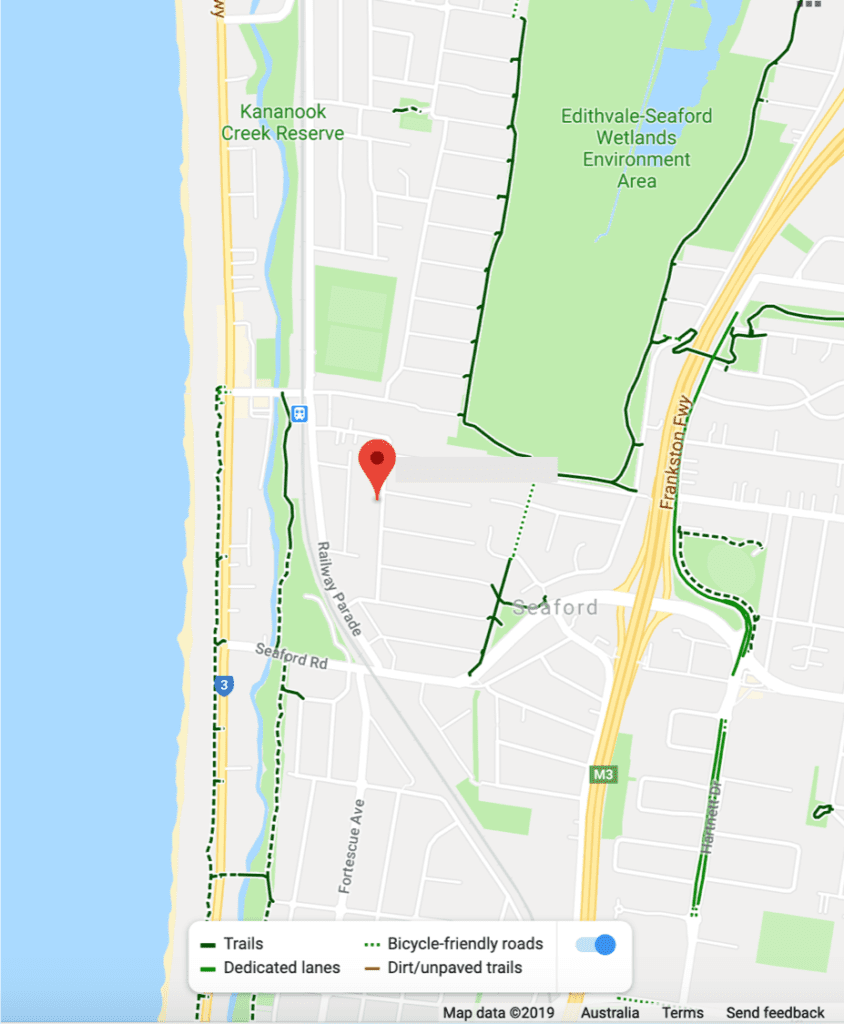

Back in 1999, I bought my second property. It was no means my eventual dream home, in fact it was quite disgusting. We paid $97,000 for it, which at the time was an exciting achievement. It was the only remaining house on a generous block of land within 600m to the beach and near to a rail station that I could find for under $100,000.

My rationale was sound, but it was my strategy that was terrible.

I was desperately chasing capital growth and a quick trajectory to a dream home. I’d made a list of all of the elements that I felt could equate to short term capital growth and targeted them in a hell-bent, determined-24 year old, kind of way. My list included;

- Short walk to beach. Preferably within 600m but absolutely within a 1km ‘crow-flies’ distance,

- Old house that we can add value to,

- Development site potential,

- Close walk to train station, (this was more of a bare necessity for me because I commuted to the city daily. My partner and I shared one car and he drove to work),

- Under $100,000.

The reason for this latter requirement was quite silly, but I had a dream of paying my home off completely by age 25 and this was a vehicle that could make that happen. After selling a property for a neat gain just prior, I’d calculated that a $20,000 debt against the beachside acquisition could be retired within the year, even with a basic graduate salary.

The capital growth was quite stellar at the time and the property was sold some 12 months later for double.

Seems good. What did I get wrong?

I made a list of mistakes. Firstly, I was thinking short term. I wanted that gain quickly. Secondly, the strategy was flippant at best and lacking a genuine long-term plan. Paying off a house at a young age is great but I was at the very beginning of my working life and had good jobs and sharp personal growth all in front of me.

I could have aimed bigger.

I didn’t seek professional advice. I thought I could handle it all, but negating the lending strategy, tax deductability, long term viability of the site, my ultimate location I wanted to reside in, and our inability to renovate on a shoestring budget and with limited trade skills was a huge blunder.

We were just lucky that that the Land to Asset Ratio was so high, and property land values soared in the area within that 12 month period.

The mistakes were varied, but the considerable one was my limited understanding of how equity can work for an investor. Rather than cashing in my gain, writing off the stamp duty and eroding the profit with agent’s fees, I could have arranged an equity release as a loan and targeted some investment-purpose, long-term “buy and hold” properties.

I just didn’t know that much about it and I didn’t ask.

There are a lot of things I wish I could tell my 25 year old self. When it comes to building wealth through property, good loan structuring advice and property strategy development is absolutely essential. I blundered my way through several more acquisitions until I firmed up a sound strategy back in 2003 with the help of a great mortgage strategist and a property-centric accountant.

The benefit of good advice has continued to serve me well, and I smile to myself when I get to meet lovely people who come to me for assistance and I hear some of the ideas that echo my old blunders.

My own experience, good, bad and indifferent has shaped me and it stands me in good stead to ask the simple question, “why?” when I meet prospective clients these days.

Special gratitude to my fellow podcasters and the extended team for the amazing insight of theirs I can share on this important facet of property investing.

Podcast link here.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU