“Cashflow property” is investor-speak for a property which is cashflow positive, or in other words a property that generates a rental income great enough to eclipse all of the costs of holding the property.

There are plenty of misconceptions floating around when it comes to cashflow property, and as an experienced investor, property investment adviser and Victorian Buyer’s Advocate, I’ve penned this article to shed light on cashflow properties.

Back in 2003 I was handed a copy of Steve McKnight’s, “0-130 Properties in 3.5 Years” and I was gripped. Without wanting to spoil the story, this accountant targeted lower socio-economic, high rental yielding areas, (namely Wendouree and Wendouree West in Ballarat), and made his claim to fame after launching his book which, (you guessed it), told Aussies how they too could replace their income via cashflow investing in a short space of time. McKnight has since sold more books, seats at seminars, and tickets for his courses. He has been questioned more than once for his claims and methods adopted over the years, and some of his strategies such as wraps have come under the legal spotlight.

The book was a great read at the time, particularly for a young professional on an annual salary circa $50,000. I was familiar with the limitations on my ability to get finance for investment properties, particularly given I had already challenged my borrowing capacity and our RBA cash rate was hovering around 5%.

The mere idea that I could continue my property acquisition journey and be assured that my out-of-pocket cash contribution to my portfolio would be eased with each acquisition, was an exciting revelation.

The thing is, things were different back then.

Little more than 15 years ago, three critical elements were not what they are today.

Firstly, credit was less restricted. We didn’t just have low-doc loans, we had no-doc options. I could apply for credit with a simple declaration and very limited supporting documentation. In hindsight, it seems insane. Some lenders accepted 100% of the proposed rental income within their servicing calculations.

In other words, if I could provide an appraisal that suggested the rent would cover the expenses, my ability to repay the loan would be broadly unquestioned.

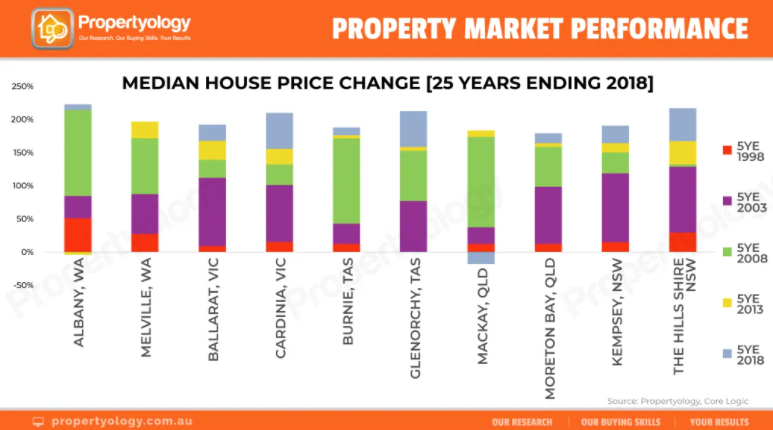

Secondly, Ballarat had already experienced impressive capital growth in this short time. Steve’s book would have no doubt propelled investor interest, but the region was under-valued and Steve spotted the opportunity. This chart, (prepared by Propertyology), illustrates the intensive growth during this period.

Thirdly, rental yields were a lot higher in the local regions in 2003. By the time I had digested Steve’s book and decided to chase positive cashflow properties, I researched townships around our country in an effort to replicate his Ballarat rental yields.

With some equity on hand and the promise of a convenient no-doc loan, I flew into Adelaide and headed north west to a lead smelting township on the Spencer Gulf called Port Pirie. Home to some fifteen thousand folks and supported by a major employer, my reconnaissance trip proved exciting enough at the time to purchase a handful of cashflow properties in quick succession.

This house below was my first acquisition for the modest price tag of $70,000. The rental return of $130pw delivered a gross rental yield of 10%. Upgrades to the properties over the coming years bolstered the rental returns to above 12%.

It sounds exciting, yes?

There was much to learn about this industrial town. From lead-poisoning risk, to the various demographic profiles around town.

The good news for me was the capital growth story.

This modest little place more than doubled in value when BHP’s Olympic Dam announcement aired a few months later. A shortage of accommodation in Roxby Downs pushed workers and their families to other nearby towns and Port Pirie benefited from this overflow.

By this stage we had purchased five properties in Port Pirie and it is fair to say that this capital growth was never what we had anticipated.

The high rental yield was deliberate. The capital growth was totally accidental.

This rapid capital growth spurred on our pace of investment property acquisition and by anyone’s measure, Port Pirie could be considered a success story, yet the reality was; we got lucky. I didn’t research Pirie for it’s growth potential, nor did I have the insight that it could grow like it did during that short time.

Since 2007, Port Pirie hasn’t done very much at all in terms of growth. The smelter has changed hands several times and the affected areas around the west of the township remain a serious concern for blood lead levels, particularly in children. The nature of the locals is fabulously friendly, but I would be remiss not to point out the challenges we’ve faced as landlords with these lower quartile priced properties in a town that has a high representation of social disadvantage. From non-payers to malicious damage, domestic issues and over-populated houses, we have had quite the adventure.

Now that the five properties are well on their way to being paid down, our rents for the five assets equate to a sum of around $1,000 per week. Once the properties are unencumbered we will have achieved the goal we set for ourselves all those years ago.

The question is; could we do that again?

In this lending climate it would be much tougher, and ten per cent rental yields aren’t on offer in Pirie these days.

Would we do it again?

Arguably not. The rental return comes at a price. The properties need constant updating and maintenance. Our ability to do the work ourselves is limited and arranging local trades at a fair price is questionable. The vacancy rates are troubling when the smelter lays off staff, and our annoyance around weekend property manager calls occasionally strikes when we are informed that a tenant has breached, or damage has been done to a property.

Most importantly, the financial return that we sustain after income tax, land tax, maintenance, property management and rates are extracted is diminished.

Many people associate cashflow properties with regional centres and mining hotspots, but cashflow properties come in all sizes. Take this current Melbourne CBD listing as an example.

“Attention all investors! Offering a great NET return of $9,015 P/A with a guaranteed weekly rental return through a long term contract with the IBIS Hotel Group, this apartment is an easy investment opportunity with stress free ownership by having all outgoings such as body corporate, rates etc, covered by the IBIS Hotel along with rental increases based off the CPI every 12 months. What a great opportunity to buy an investment at the right price! Call now before it’s too late!

This building features concierge service and secure lift access which adds consumer confidence in a location literally walking distance from every CBD attraction including Southern Cross Station, the Docklands precinct and Etihad Stadium. Also included is a shared internet / study area, exclusive tenth floor gym and the inviting ground floor cafe/ bar.”

What this ad doesn’t point out is the net cashflow. The 7.2% sounds compelling until the management costs to IBIS are factored into the equation, along with the Owner’s Corporation strata fees, City of Melbourne rates and the property management fees.

Nor does it point out the likely deposit required. “Lenders will require a much higher deposit – expect 30-40% on a serviced apartment. Potentially ties up a lot of capital, particularly if in portfolio building phase,” says Tim Boyle of Finalytics Financial.

A property such as this one is not likely to deliver strong capital growth and the residual cashflow benefit that remains after all expenses are accounted for is modest to say the least. Even with record low interest rates, the case is not compelling for a bedsit in my opinion.

An investor would need many of these to have a desirable post-retirement income.

Cashflow properties certainly have a place in a portfolio, but after all these years I’ve learnt so much about where they fit in the ideal strategy.

Capital growth creates wealth. Cashflow properties can buffer a portfolio for balance, but a long term strategy for someone who embarks on their investing early in life should focus on the best capital growth options that fit within the investor’s own cashflow ability.

Cashflow is king, and capital growth is the enabler to long term wealth.

We have growth assets in our portfolio, (both regional and capital cities) that have since become cashflow positive over time. They are, by far our best performers overall.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU