Auction quoting regimes is always a hot topic, but it raises its ugly head in the media when market conditions get tough for buyers. In the last month, more than a few journalists have asked for comment about under-quoting, and whether it’s rife.

The short answer is, yes, it is happening, and it is rife, but it’s vital to understand why it happens, and how our quoting system works.

We don’t have an auction quoting regime that is based on the vendor’s desired sale price.

Our regime unfortunately has an essential gap; a loop hole, and it permits vendors to leave their reserve price off the selling authority. A vendor is only required to disclose their reserve price and state it formally to the agent before the auction day.

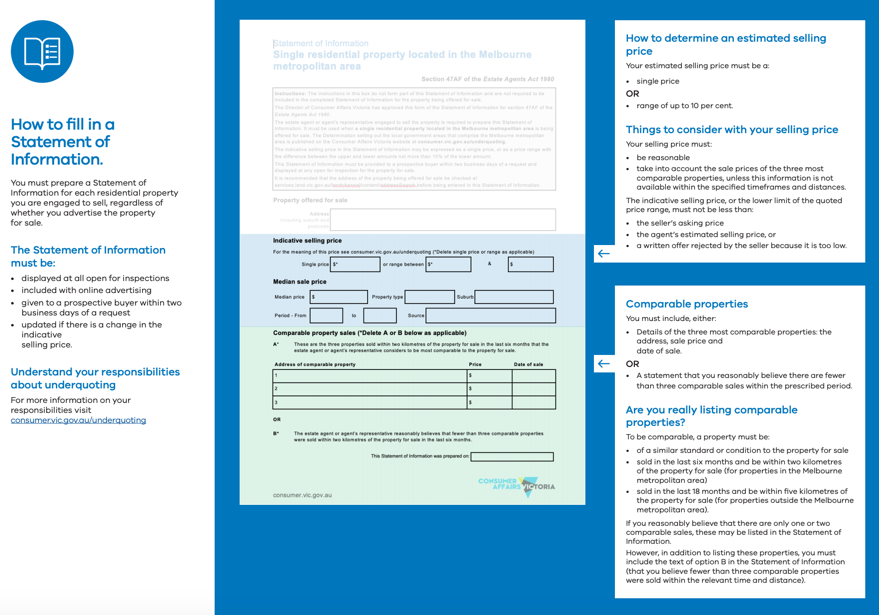

Therefore, the only way that a selling agent can provide a buyer with an indication of a price is by either estimating the likely selling price, or by providing the buyers with three comparable sales as a guide. This form is known as The Statement of Information, (below).

The problem with this clumsy method is that the classification of the data is subjective.

It relies on an agent’s determination of comparable.

Worse still, our regulatory body’s requirement for recent sales offers agents the parameters of six months.

Six months in an aggressively moving market is a long time. Our market has moved more than ten percent in this period.

The regional locations have been particularly difficult for buyers to navigate, because our regulatory body allows some eighteen months for the permitted timeframe of cited comparable sales. Ironically, the regions outperformed the capital cities over the last twelve months, rending some Statements of Information utterly useless.

This methodology gives way to unreliable sales evidence and hence skews the basis for the estimates given to the buyer. In short, the statement of information not only proves to be of limited use, but it often misleads buyers due to the low data integrity.

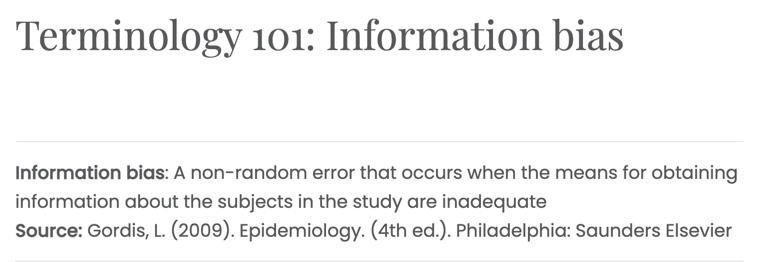

The data explanation for this skewed information is information bias.

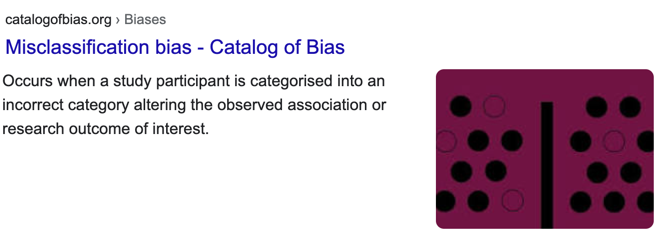

Specifically, a subset of this, misclassification bias is introduced. If an agent includes past sales that are either irrelevant, anomaly results, too dated, or inferior due to an invisible attribute (ie., zoning), a buyer will likely be circling the wrong data points as they determine their bidding strategy.

With this risk of such bias impacting the price guide information given to buyers, it is of little surprise that so many bidders and buyers have insufficient budgets on auction day.

An enormous number of buyers miss out every weekend at auction, and those who have participated in a ‘best and highest’ offer process on a private sale property will be all too familiar with the heartbreak associated with getting their pricing wrong.

A recent example was that of my own stepson’s acquisition. He and his partner are now renovating a brick veneer dwelling in Geelong’s Grovedale; a southern suburb near to the rail. We circled in on a three bedroom, two bathroom house on it’s own full block in a desirable street. The property was quoted $350,000-380,000. Their budget was $450,000, but my familiarity with the region enabled me to prepare them for vast queues due to the pricing inaccuracy. I knew that similar properties had been selling in the mid to high fours, so I suggested they get down there early in case the half hour inspection time runs out before they made it to the front door.

We were right to be concerned. They only just made it through the property. A frenzied ‘best and highest’ offer ensued in the days afterwards. The sale was closed out at 2pm Wednesday after the agent instructed us that there were multiple offers coming in and to submit our ‘best and highest’ offer.

My analysis pointed to a $450,000 to $470,000 price point, however Rob and Mon’s budget was capped. I suggested to them “Guys, put it all on the table. If you get it, you’ll be lucky.”

Their moment of anxiety was forgivable; I was asking them to submit an offer twenty percent above the top of the quoted range. We went through the analysis and we covered their concern with a finance clause. We decided that under the circumstances, it was safest for them to let the bank valuer decide if it was the right price.

The valuation came in at purchase price.

Had Rob and Mon let the price guide influence their approach, they would have missed the property altogether. With a regime that permits 18 month old sales results to be captured on the Statement of Information, this region has been tough for buyers to tackle.

Eighteen offers were apparently submitted, and there is a possibility that for the other seventeen who missed out, some purchasers may have had the financial capacity to submit stronger bids.

There are plenty of buyers out there, who like so many in this situation would have relied somewhat on the Statement of Information. One passerby recently told Rob that she had also submitted a bid on the property. Her offer was $381,000; no doubt influenced by the price guide.

Auctions at least give buyers a sense of social proof; the buyer can rest assured that others bidders also wanted the property, and were prepared to pay a very similar price. But it does present a challenge for buyers in the ‘best and highest’ situation when social proof isn’t available.

Information bias can play a disruptive role in the price setting task for buyers. Being prepared to question the Statement of Information is critical for anyone who is using it as a resource, and disregarding it altogether often enables us to have clearest insight via our own recent comparable sales methods.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU