I often talk about the cost/benefit analysis of a holiday house, but what do the numbers really say?

This week, I’ve modelled two similarly priced properties that have recently sold for around the mid-$700,000’s. One is a coastal holiday house on the Mornington Peninsula.

The other is a house in the northern suburbs of Melbourne, 17km from CBD.

My assumptions for each include interest-only repayments, a dutiable land value of $600,000, and no rental/Air BnB activity for the holiday house. I have also assumed an overall 32.5% tax rate for the negative gearing deductions for the investment property.

The cashflows certainly tell a tough story for the holiday house. Without rental income or tax deductions, the holiday house is costing it’s owner an additional $2664 per month than the similarly priced, pure investment property.

This figure translates to $31,968 per year.

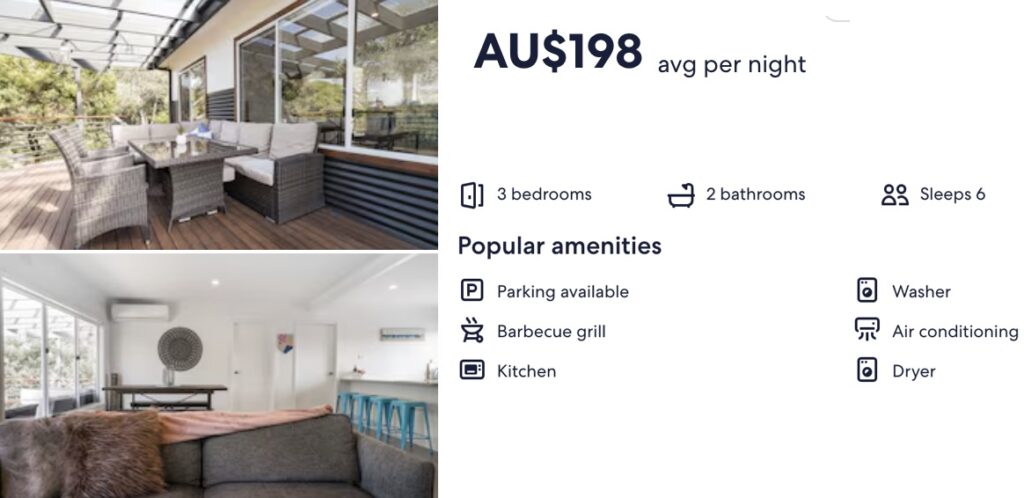

If I weigh up the cost/benefit analysis of this scenario, I need to consider the cost of funding a holiday lifestyle on the Mornington Peninsula. If the purchaser decided to invest in the house in Melbourne instead of purchasing the holiday house, a viable alternative would be to rent short-stay accommodation for six weeks of the year. If we calculate the cost of 42 nights per year based on a similar dwelling in the same suburb, the cost of the holiday rental is $8,316 per year.

And the investor can enjoy arriving when they please, leaving the clean-up to a cleaner, and letting the gardener and maintenance person take care of lawns and gutters.

We must also take into account the capital growth prospects however, not just the cashflow.

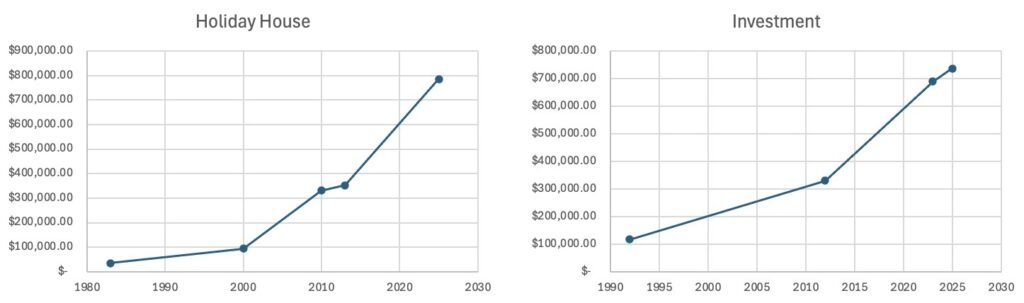

The Mornington Peninsula property has outperformed the northern suburbs property. COVID lockdowns, combined with record low interest rates gave way to a strong surge in asset values in holiday locations during this period. The Mornington Peninsula fared particularly well in terms of capital growth prior to COVID also, especially in the lower priced coastal segments of the Peninsula which have grown off a considerably lower base than the likes of Sorrento and Portsea.

Modelling out the two property’s sales history side by side, and creating a line of best fit reveals that the holiday house has grown at an average of 7.6% year on year. However, the northern suburbs property has only delivered 5.8% over the recorded sales history period.

Over many years, this 1.8% pa differential will make a significant difference and will eclipse the loss of cashflow after a few years.

There is no doubt that the long term growth of the holiday hotspot asset would have place this purchaser in a better asset position over the same period based on this growth, but cashflow counts for a lot too. The volatility of the holiday hotspot cannot be ignored either.

The question remains: What kind of a difference would the $2664 per month make to an investor who decided not to target the holiday house? More holidays in more destinations? A more sizeable investment purchase of a property that delivers stronger capital gains? A growing share portfolio?

The point of this exercise is to focus broadly about cost/benefit analysis when it comes to property decisions, and weigh up what is best for us as individuals.

For some, their holiday house represents far more than an asset, and it can bring immense joy. Cashflow must be understood first though.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU