Every January (and without fail) I field questions from new and past clients about my thoughts on their holiday house acquisition ideas. And every year I learn more about why this is such a well-trodden path for so many. The reasons are always emotional and never pragmatic, ever.

But when is it OK for emotion to rule?

And when is a holiday house a good idea?

My answers in my head are already there, just waiting to be shared, but because this is such an emotional topic I do have to be thoughtful about how I answer. For so many people, the mere idea of a holiday house is driven by a strong force, whether it be the dream to gather family and create memories, to escape the daily grind, to enforce a sense of relaxation, or to pursue a lifestyle that adds a new and happy dimension to their daily mindset.

The reality is that a Holiday House is not an asset in the same sense that a pure investment property is. A pure investment should be considered on all financial, timing and practicality measures. Annual returns, costs of holding, borrowing capacity, long term growth, target tenants and debt retirement strategy form all of the facets to tick off the list when buying an investment property.

As soon as personal use creeps into the equation, purity is no more…. and the waters start to get murky.

I’ve seen so many investors approach investing with personal-use in mind (whether it be ‘one day I might downsize into this unit’, or ‘my kids might live in it when they go to uni in ten years’ time)… and as soon as a personal-use criteria forms part of the brief, the most suited areas and dwelling types for the investor’s financial goals could be over-shadowed by their own personal-use criteria.

I’ve seen so many investors approach investing with personal-use in mind (whether it be ‘one day I might downsize into this unit’, or ‘my kids might live in it when they go to uni in ten years’ time)… and as soon as a personal-use criteria forms part of the brief, the most suited areas and dwelling types for the investor’s financial goals could be over-shadowed by their own personal-use criteria.

Holiday homes are often so much more debilitating for an investor’s financial strategy than a unit that they ‘may’ move into one day. Holiday homes present significant challenges, some of which include:

- The Owner wants to stay in the property when the rental potential is at it’s highest (ie. consider the optimum time of year when a Peninsula or Surf Coast property can lease for a few thousand dollars per week… it’s generally the time of year that the Owner will want to share the property with friends and family)

- The properties are tough to let during the down times without significant management, laundry and cleaning costs

- A long term residential tenancy may not be all that suitable for the property and the target tenant may not be a desirable tenant in these coastal regions

- Tax benefits will likely be eroded or negated if the holiday house is for personal use

- The upkeep of the property can become draining on owners when they feel their weekends at the property are spent maintaining or cleaning it

- Conflict can arise when family members feel that use or costs are not shared equally

- Rates, maintenance, land tax and insurances are often heftier than anticipated and the viability of holding the property can be questioned

These points above can all be upsetting for owners, but there are two points which are often neglected to be answered when in fact they could be vital to the decision-making process.

- Is the property likely to out-perform a similarly priced alternative property in the capital growth stakes? Or could a pragmatic decision to invest enable the investor to buy their coastal dream home in years to come?

- If the Purchaser forecast all of the expenditure and out of pocket costs associated with a pure investment property, and then considered leasing a regular holiday rental each year, would they find that the resultant financial position is more advantageous?

Genuine emotional reasons can be solid reasons, but if the property causes stress, upset, financial strain or creates set-back on the buyer’s own retirement or wealth-creation plans, it really does deserve caution.

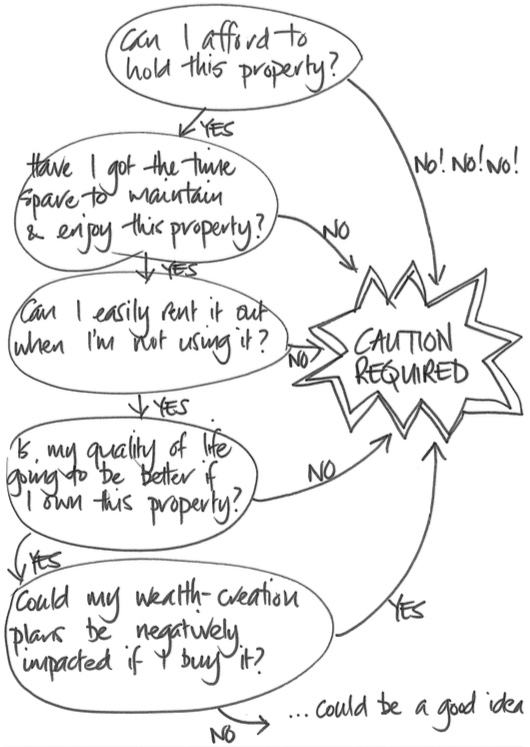

This flow chart (as basic as it seems) is what I often draw in my notebook when I’m talking to someone about whether a holiday house is a good idea for them at this point in time.

The reality is that we only get one life and life is meant for living…

… but if provisioning some money every year to rent out someone else’s holiday house makes more sense and creates less stress, it has to be a model worth considering.

I’ve seen some happy and successful holiday house stories but I’ve seen plenty of stressful stories too.

Holiday hotspots can present price volatility (particularly when the local capital market corrects) and there is nothing more deflating for an investor than selling for a loss due to cashflow restrictions.

January often tugs at our heartstrings and reminds us of beautiful family times and friendship experiences, but a holiday house is more than just a few free weekends away… it’s a serious financial decision.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU