I wish I’d written this article fifteen years ago when I started working as a buyers agent. There are so many misconceptions about renovations and upgrades, and what legal documentation is required.

Of all of the misconceptions though, the most common one relates to permits and the contract of sale.

I often see updates in properties that look recent. Many agents are quick to respond with either or both of these comments.

“The works were under $16,000 so they don’t need paperwork.”

“It was done over seven years ago so it doesn’t matter.”

The issue is twofold. Firstly, the seven year requirement only relates to the requirement to include the paperwork in the contract of sale. In Victoria, all documentation, (including permits if required, domestic building insurance and trade certificates) need to be included in the contract of sale if the works were done in the preceding seven years.

But that doesn’t mean that the paperwork isn’t important.

If the works were done without permits and/or certificates prior to the seven year period, the works are illegal. This challenges any future insurance claims and also questions any further works being permitted by the local council.

Just because illegal works are over seven years old doesn’t remove the liability for the new owner.

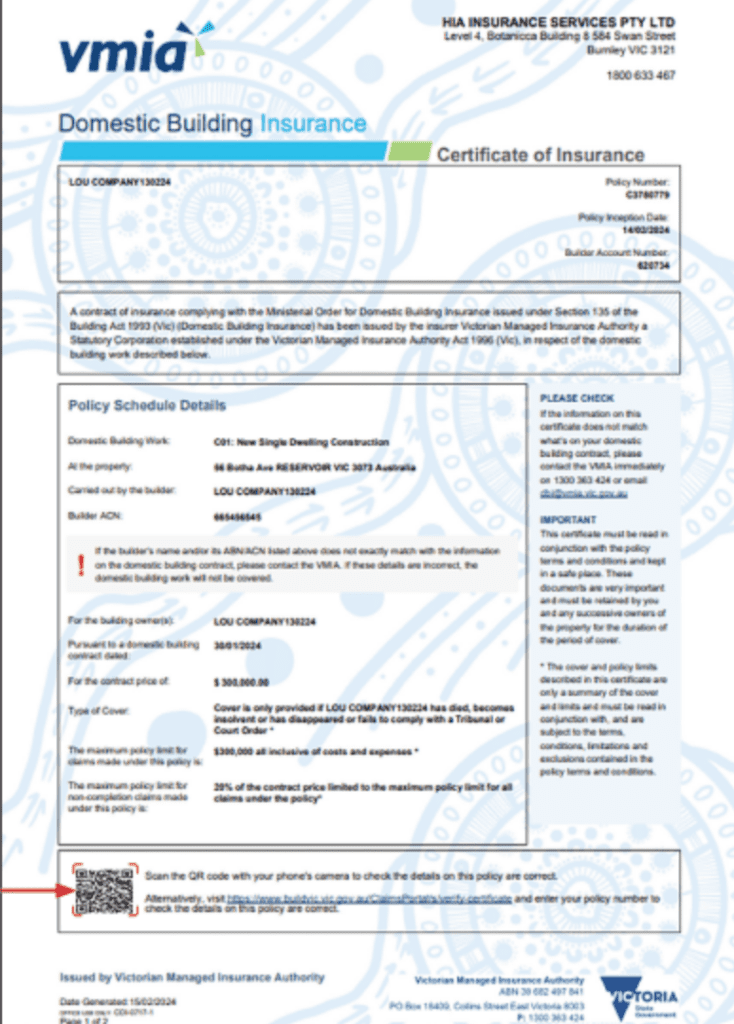

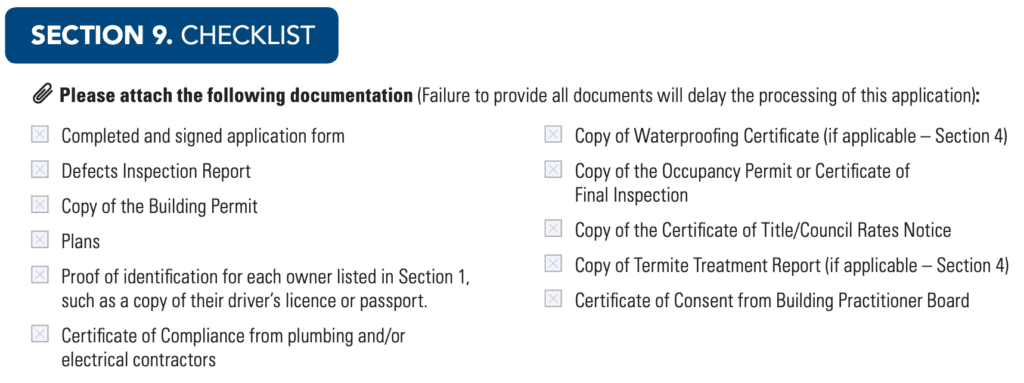

Secondly, the cost-magnitude of any previous work is important to understand. Not all jobs require building and/or planning permits, but for works exceeding $16,000, a domestic builders warranty insurance policy is necessary, and the policy itself will require certificates. These include, but aren’t limited to:

- Certificate of compliance for plumbing and/or electrical,

- Waterproofing certificate (if applicable),

- Building permit (if applicable),

- Planning permit (if applicable),

- Occupancy permit or certificate of final inspection, and

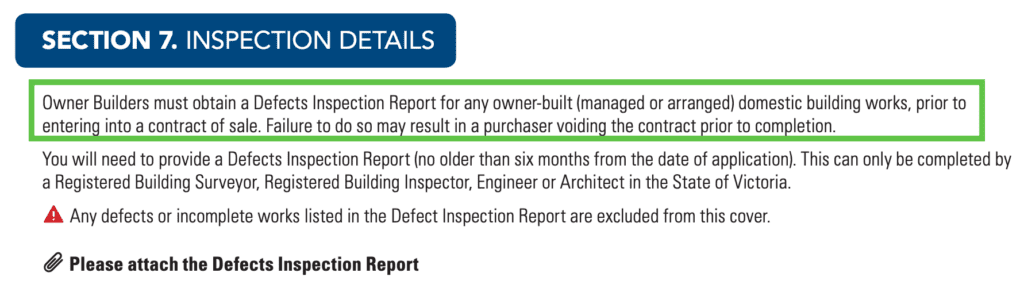

- Defects inspection report (for owner builders)

“Unless the work is done by a registered builder with a major domestic building contract in place for works over $10,000.00 and builders warranty insurance in place if the works exceed $16,000.00, the works are generally regarded as “owner builder” works. If the renovation works have been done by the owner or the owner managed trades to do the works in the 7 years preceding selling the property, the works need to be disclosed in the Section 32 Vendors Statement. Disclosure entails a current Owner Builder Condition Report (less than 6 months’ old) and, if the value of the work exceeds $16,000, Owner Builder Warranty Insurance is required too.” (Quote: Owner Builder Works by First Class Legal).

“Owner Builder works include: kitchen and bathroom renovations/makeovers, pergolas and decking.” It does not need to be gutting of the house nor structural work. In short, if works were done without a permit (whether a permit was required or not), they are regarded as Owner Builder works except where a permit was not required and a registered builder has done the works with a major domestic building contract in place.” (First Class Legal)

So, what sorts of jobs do I see that would have triggered a need for warranty insurance and permits or certificates? From sheds in yards to timber decks, bathroom upgrades to kitchen makeovers.

The works don’t have to be structural, nor do they need to be noticeable from outside the property. If the works are;

- Requiring a building or planning permit, or

- Over $16,000 in total value,

The vendor needs to have paperwork to satisfy us that they complied with the legislation.

The question often arises though; when is it OK to pursue a property for a client when we are doubtful previous works, and whether the legislation was complied with. Like any situation where risk is weighed up, we consider the magnitude of the works and the potential for our client to be disadvantaged. For example, if the works relate to a deck that was built without paperwork prior to seven years ago, we have to weigh up the risk level and the implication.

Would the property be de-valued if the council issued a show cause and requested the deck to be removed? And what is the likelihood of this occurring? The same could be said for an old shed in the backyard. If the cost of removal of the structure, combined with the magnitude of the value-loss is small, the decision to move forward with the purchase may be sound.

But the risk of future issues, (for example, leaking bathrooms due to shortcuts taken without waterproofing), combined with the risk of insurance being declined are much more serious.

Each situation needs to be considered on merit, and in consultation with a conveyancer or lawyer.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU