Two years ago this month, I collaborated with my (then 21 year old) stepson to help him onto the property ladder.

He was still living at home with his Mum, work was an easy commute and he had no reason to consider buying his own home. Having grown up around property investment though, he knew all too well that forced savings and investing early was an idea to canvas with us.

There are various ways that parents can help their children get into property and everyone’s situation, risk profile and approach is unique.

From gifting deposits to Family Pledge Loans, joint or tenants-in-common purchases, earmarking properties in Trusts for future gifts and so on, the enablers are numerous.

One thing that they all have in common is the requirement for legal advice or Statutory Declarations.

This is for good reason: helping our loved ones financially can carry risk and parents need to fully understand the scope of their assistance and the implications going forward. In the situations where shared responsiiblity ensures, we all want to know that our children will cope with the responsibility and benefit from it. In situations where gifts are concerned, we never want to think the gift could create turmoil or land in the wrong hands in future years. Legal advice is really important when considering the arrangement itself, the estate planning associated with the property and the responsibility either party is taking on.

We had decided what arrangement would work for us with Rob. He was an apprentice carpenter at the time and while he didn’t have remarkable savings, he did have remarkable energy and ability to renovate.

If we could fund the 10% deposit, he could renovate the house.

At the time his apprentice wages couldn’t have easily covered a cash flow shortfall, and while we were excited to see him start his personal wealth journey, we didn’t want to pay for a cash flow shortfall either.

Knowing that we had to target a property exhibiting stronger rental returns than normal, I circled three bedroom, renovated houses on compact and subdivided blocks as ideal contenders. I also wanted to ensure that the capital growth prospects would reward him so I focused on the gentrifying suburbs in the middle ring west as close to rail amenity as my designated budget would allow.

Sunshine and Albion had already exhibited substantial growth and change, and while I had no doubt that residential investment in this pocket would continue to flourish, we’d been priced out by the recent growth.

Ideally I needed to find a property that could provide a gross rental yield well above 4% and preferably around 4.5%. In order to meet our cashflow target (of minimal ‘out of pocket’ contribution each month), I had worked out that a standard, renovated 3BR brick home in the area typically rented for $360pw, hence I had a budget of circa $400,000 to work with.

My calls to agents worked well. We had a few options to choose from but it was this triple fronted brick house on 307 sqm that showed strong potential to fit the brief. It was presented well, partially renovated and screaming out for a new bathroom, laundry and landscaping.

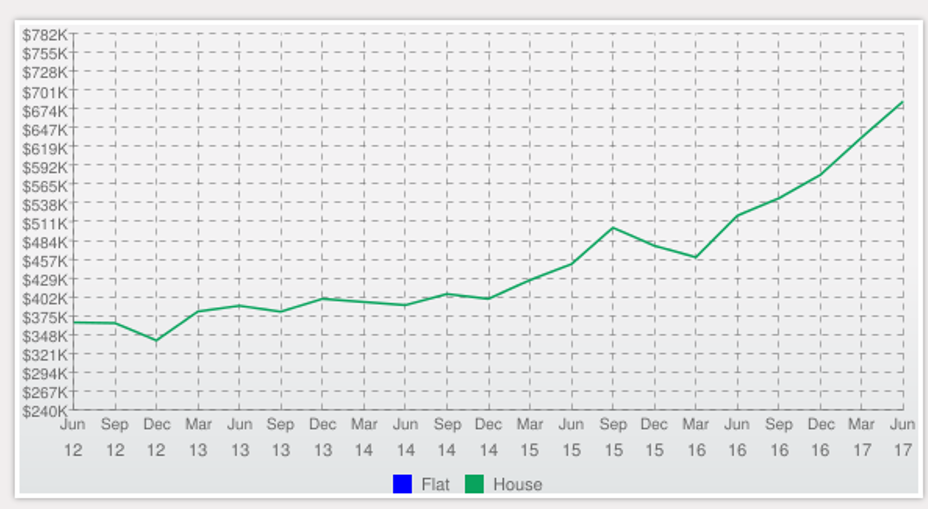

We secured the property for $405,000 in September 2015.

Our 50/50 tenants in common arrangement meant that he owned his half share and his labour over the January break added significant value to the property we had a half ownership in.

Two year’s on, our second tenant now residing in the property, a relatively seamless period of low-maintenance, consistent rental income and attractive tax returns for Rob, his strongest benefit has been the capital growth, but not that he’d know. He’s been happy to accept that the property is purely an investment decision. It’s not to be inhabited by him and equity is not to be accessed for anything other than future property or business investment.

We all agreed on the strategy at commencement.

I chose Sunshine West at the time because it was one of several areas which could offer the cashflow metrics we’d engineered, it was within a 15km radius, the area was supported by rail infrastructure, and I believed that the growth in Sunshine and Albion would have a flow on effect based on relative affordability for those who had been priced out of these two suburbs. I had envisaged that the property would experience capital growth and in hindsight it was a sound decision.

Rob is now 23 and he has generated enough equity to take on a second project already in a short space of time. His commitment to our ‘buy and hold’ strategy is well understood, and we look back at our arrangement with pride.

I see parents assisting their children on a regular basis, from moral support at opens and auctions, to financial contribution. Whatever the method that works for each family, there are ways that we can help them in property. Housing affordability (or the lackthereof) for our young people gets a lot of media attention, but thinking outside the square might provide a different solution.

They don’t have to buy where they want to live.

Note: It’s also important to note that the First Home Buyer Stamp Duty Concession is still available to Rob. Those who invest in property (and don’t live in the property) are still eligible* (*provided the legislation does not change).

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU