The property market may not have been presenting idyllic conditions for investors in Victoria, and there is plenty of commentary on this topic. However, Victoria has delivered optimal conditions for first homebuyers, and for several reasons.

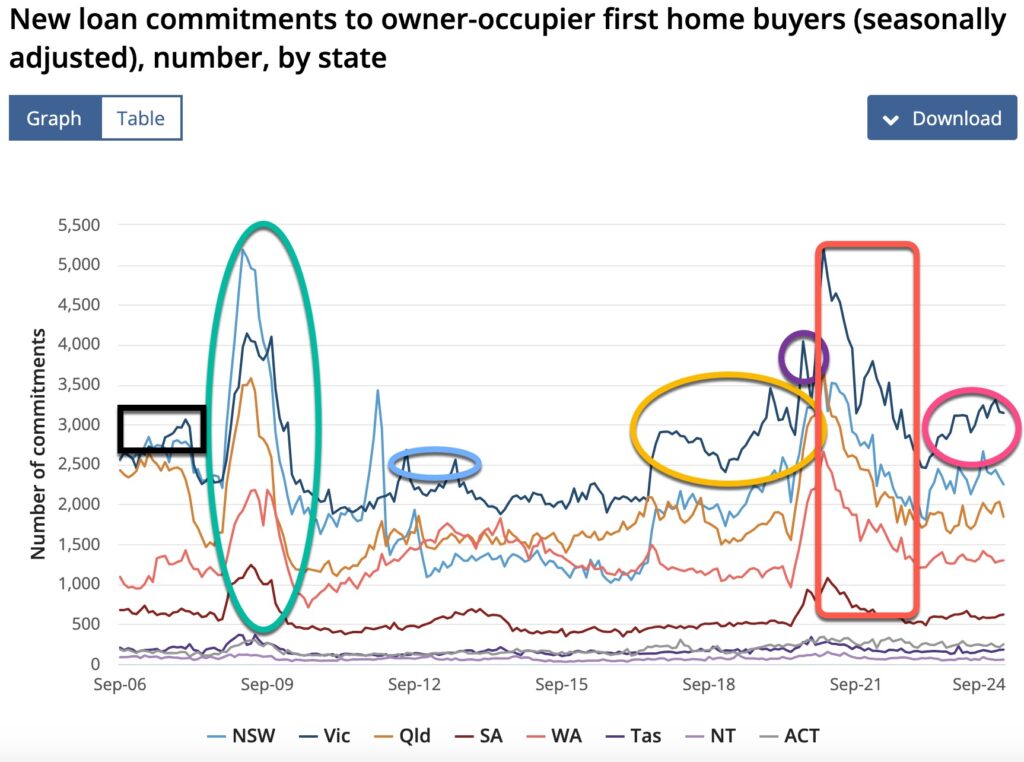

The Victorian (and Federal) governments have historically provided some exciting opportunities to first home buyers, and justifiably so. Looking back at this chart below, some of the key initiatives are circled.

Following Victoria’s line (in navy blue), this chart illustrates some interesting incentives. The first peaks (in black) occurred during the Kevin Rudd leadership period, just prior to the Global Financial Crisis. Following on from the Howard government’s introduction of first home buyer grants, the next government also introduced the ‘boost’. Combined with softer credit policy, (including low-doc, no-doc and 104% LVRs), conditions were encouraging for many first homebuyers during this time.

I recall my experience as a young mortgage broker during this time that some first homebuyers could enter the property market without deposit savings if they were able to take advantage of grants and boosts.

While the incentives for first homebuyers were broadly national (and not Victorian-centric), Victorian first home buyer activity was the strongest nationally during this period. The Victorian market was performing well and first homebuyers were anxious about ‘missing the boat’.

The next peak on the initial first home buyer activity chart (in green) signifies an enormous stimulus from our governments, combined with considerable interest rate cuts. This was all in response to the impact of the GFC. Our market delivered over 20% growth in a very short time, and first homebuyers were still very active, despite dramatic credit policy changes. No longer were high loan to value loans on offer, and some lenders left the Australian market altogether. It was government stimuli and low interest rates that powered the Victorian first homebuyer market in 2009.

The following two smaller spikes were during a period of downturn. The Victorian government introduced the first homebuyer grant of $10,000, and a regional grant of up to $20,000 during this time.

Fast-forward five years, and the yellow circle illustrates the impact of stamp duty concessions. Initially capped to $600,000, the Victorian government shaped the offering to what it is today. The requirement to save both a deposit and stamp duty has always been a tough hurdle for first homebuyers, and while some would argue that the current thresholds are insufficient, the policy has broadly been positive for first homebuyers.

The small spike captured in purple in 2020 is likely a response to the Victorian government’s 50% reduction in stamp duty for all purchases up to $1,000,000. This was a COVID stimulus which was on offer to all buyers (not just first homebuyers, but repeat buyers and investors alike). While it certainly added fuel to the rate of capital growth generally, it is fair to say that the sub-$1M market is largely made up of first homebuyers.

Following this, our record-low interest rates fuelled every market, but Victoria remained the strongest (highlighted in red). There are several reasons why, but hard-hitting lockdowns and a desperate need for change was a key driver.

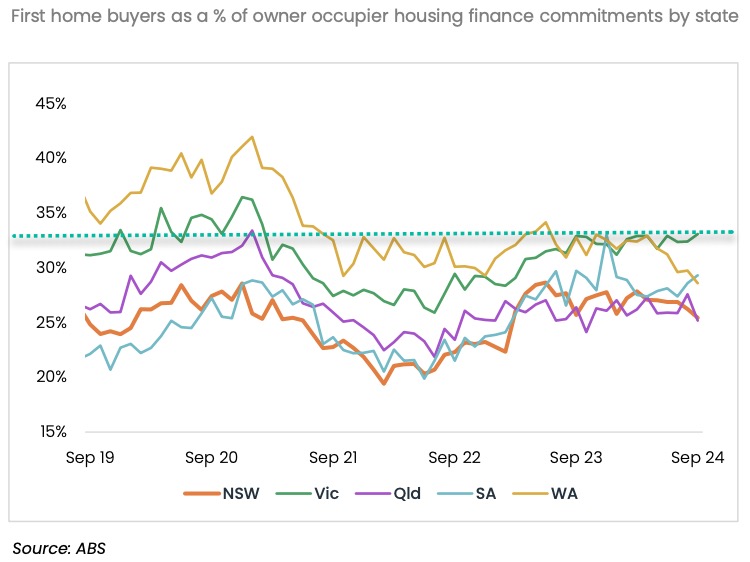

Lastly, we come to our current market. While Victoria has underperformed nationally, the easing of investor activity, combined with investor-led sales has given our first homebuyers an opportunity. Unlike some of the other capital cities, Victorian buyers aren’t competing at the same level with investors. The chart below illustrates the differential in the investor lending ratio between states, and specifically shows that Victoria has the highest count of first home buyer activity.

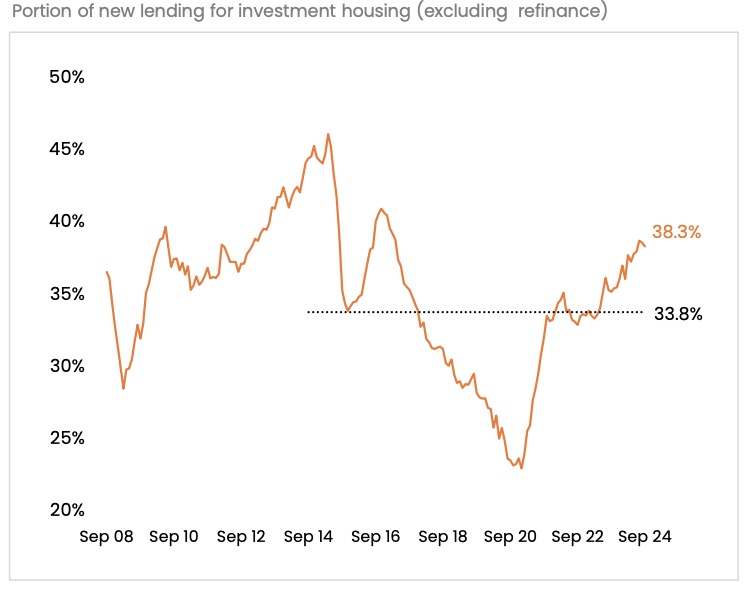

Historically, first homebuyers have competed with investors. This has been a challenge for past governments in terms of managing incentives without stimulating the broader market, (or worse still, artificially segmenting the market). Currently, investor activity is considerably above the historic ten year average (as shown below)

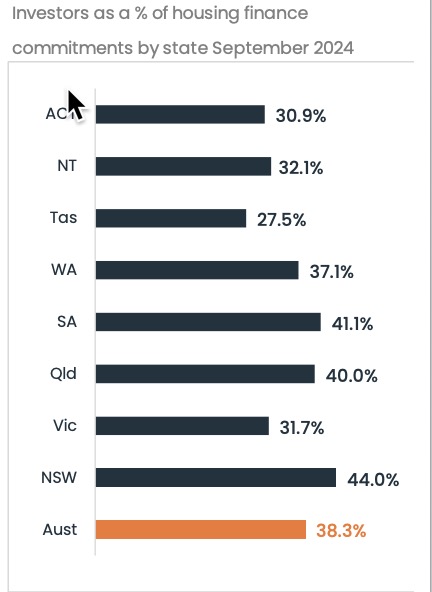

However, as this state and territory breakdown below shows, Victorian investment activity sits below the ten year average. This

The introduction of the First Home Guarantee has optimised things further for our first homebuyers nationally, and in addition, the Victorian government has a shared equity scheme on offer too.

Prices have not only been static for buyers in Victoria, but modest price corrections have given way for some good buying opportunities.

Unlike previous years, the current market conditions for first homebuyers are encouraging.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU