In response to COVID-19 dampening buyer sentiment, domestic spending and confidence in the Victorian property market, our state government announced an incentive for all residential property buyers, (in addition to already-existing concessions and opportunities).

Quickly formulated and declared in early December, this special offering took effect immediately and created a flurry of questions and actions, as these types of incentives often do.

Our state government’s changes to land transfer (stamp) duty was aimed at residential property purchasers, both owner-occupiers and investors, allowing for a 25% discount for all established property, and 50% for all new property priced up to $1,000,000, eligible until 11.59pm on June 30.

This was indeed a surprise, particularly for investors.

Those who had purchased residential property in this price range prior to Tuesday 24 November were caught in a moment of frenzy. Could they retrospectively claim it? Could they cancel and re-submit their old offer? And for those who had purchased incrementally over $1M, could they rethink their purchase altogether?

Like all sudden incentives, more than a few knee-jerk responses were initiated.

In tandem with low interest rates (the last of which had only been applied by our RBA three weeks’ earlier), heightened consumer confidence and a city experiencing multiple weeks of zero new COVID infections, we did wonder if this announcement was ill-timed, or even required at all.

Casting our memory back to 2016 and 2017 when our First Home Buyer Stamp Duty concession was increased substantially, we did in fact see a market shift for a specific genre of dwellings in our market. There is no doubt about it, boutique apartments and villa units held in the typical first home buyer sights had their prices agitated. Villas in the inner ring sky-rocketed, and we finally saw price movement in the established apartment market again, much to the joy of investors who held such stock.

Could the same occur for our sub-$1M market now? Most certainly. And it won’t be restricted to Melbourne, nor will it all have a positive effect when the offering comes to an end.

Sadly we are now seeing plenty of buyers scrambling to secure the discount, particularly in the $950,000 – $1,000,000 price range. Emotion can sometimes toy with us, particularly when it leads to irrational behaviour.

Securing a discount to the detriment of sensibility spells a false economy.

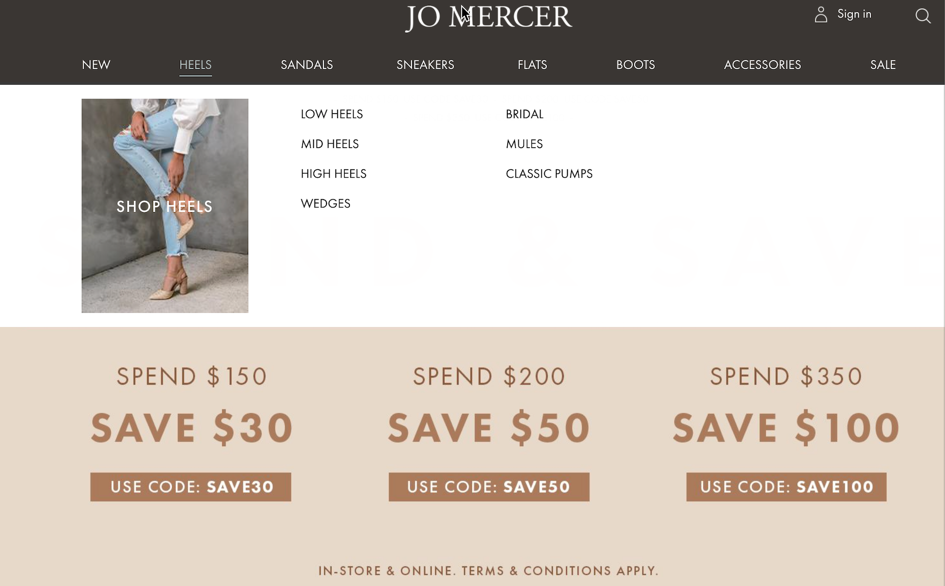

We have spoken with more than a handful of buyers about the ‘cost’ of a discount. It is a little bit like a special offer on a pair of shoes. We often see specials online or instore for a subsequent pair of shoes being discounted. Take this ad for example; it it easy to get excited about the discount on offer, but what if I don’t need the second or third pair of shoes? What then? I’ve secured a discount but spent more than I intended to.

Human behaviour is an interesting thing. We have seen so many efforts to claim the stamp duty discount on offer, but too many buyers fight other buyers to the finish line, losing sight of how much they are actually overpaying.

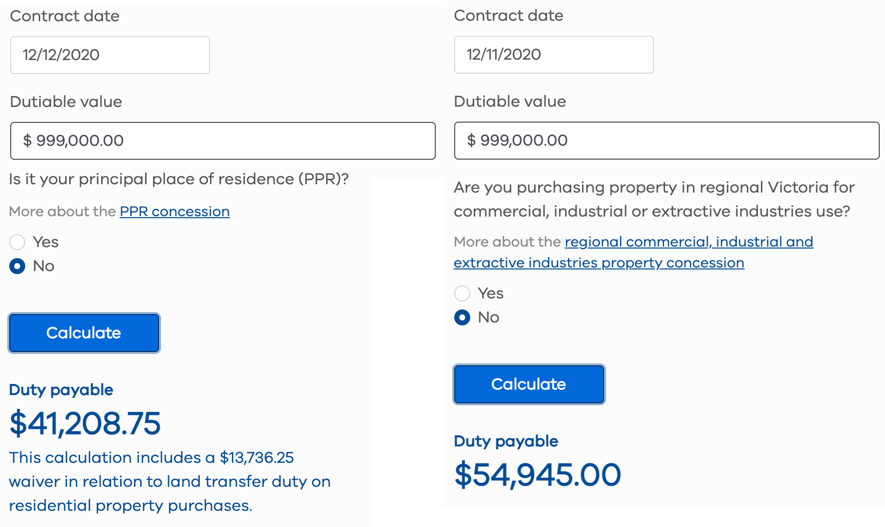

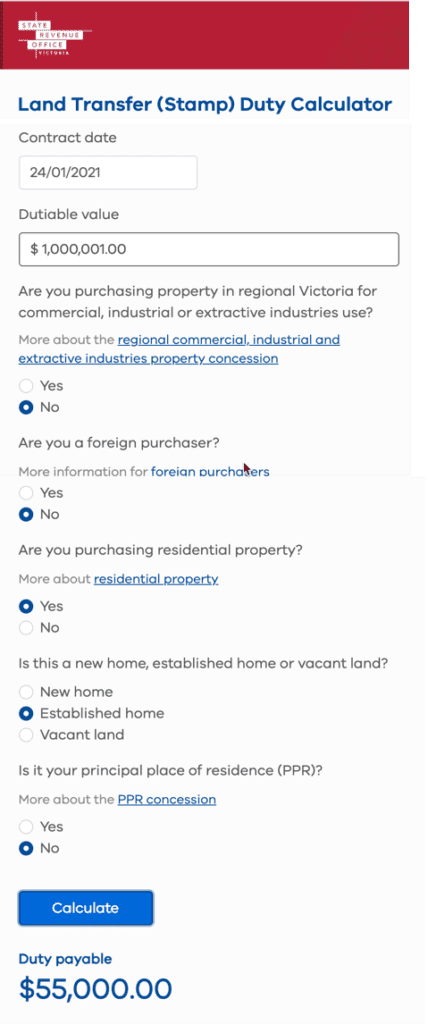

What is the point of paying $30,000 or $40,000 more than the property is worth for the benefit of $13,700 in discounted duty? Surely a buyer would be better off paying $1,000,001 for a property that is actually worth $1,000,001 and accepting the $55,000 stamp duty bill.

We can anticipate that some of the properties to be most impacted by this short-term offer include 3BR houses and townhouses in the areas which offer such dwellings in the $900,000-$1M price bands. Some of these townhouse locations include Newport, Footscray, Kensington, Flemington, Thornbury, Brunswick, Mordialloc, Glen Waverley, Ringwood and Oakleigh, to name a few.

Houses however will be even more dramatically impacted, as our COVID conditions have exacerbated the mainstream desire for more space, more bedrooms and more potential to extend our homes. Such areas include: Glenroy, Reservoir, Sunshine, the foothills of the Dandenongs, Carrum/Bonbeach, and many suburbs in the already-bustling Geelong.

Our contingent who could be most negatively impacted are in fact the contingent that are more vulnerable; our first home buyers. Now that they find themselves up against investors, upgraders, holiday-house buyers and down-sizers, the requirement for pragmatism and sensibility is really imperative.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU