In this rapidly evolving economic climate its easy for investors to find themselves being short-sold.

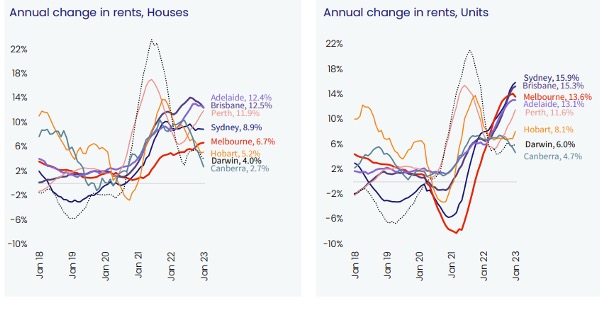

We know that increasing interest rates can’t simply be passed on to the tenant. Rent movement is purely driven by supply and demand, however our current climate is aligned with rental increases, and for good reason beyond interest rate movements.

Currently the pressure on rents, (in most capitals and major regional cities) is increasing. Our supply is down and our demand is being driven up, as new arrivals numbers are growing. The demand is often talked about and we’re acutely aware that renters are experiencing tough market conditions.

What is less documented is the reason for our decreasing supply.

In quite a few of our states and territories, our rental reforms have initiated a flurry of activity for many investors. Trade compliance certificates have triggered significant work orders for many rental providers, particularly for older dwellings. The $400 inspection surcharge pales in comparison to the works required to bring a property up to the new required specifications. We’ve heard examples of recommendations spanning tens of thousands of dollars for some rental providers; from new gas lines to complete electrical rewiring.

For those owners who are cashflow poor, the obvious alternative is simply to sell.

We then need to consider some of the onerous changes that have been initiated by our regulators in relation to tenant’s rights. In Victoria, for example a tenant no longer has to request permission to get a pet. And an owner has now lost the option to invoke a 120 day “no reason” vacate notice to troublesome renters. While this gives good renters some peace of mind about their tenure, it gives a property owner very little opportunity to evict a bad tenant without the drudgery and delay of a tribunal hearing.

And the next dis-incentive we note is that of credit availability. From 2014 to 2019, our regulator instructed banks to limit investor credit. This was done by applying tougher scrutiny to loan assessments, lower LVRs, tighter overall credit per customer and higher interest rates. Since this time, credit availability has improved slightly but it’s still very difficult for investors to obtain credit, according to brokers.

Finally, our ageing population, and particularly baby boomers are now facing retirement. Many are cashing out of property as an asset class and moving into shares.

So the cocktail of reasons above has given way to a dire, (and worsening) rental stock shortage.

One of many of our Victorian rental reforms relates to rental increases. Rental providers are restricted from applying more than one annual rental increase. What this means in a fast-rising rental environment is that they will quickly find themselves out of step with market rent if they are not actively assessing the correct rent at the time of a lease expiration, (or a twelve month anniversary since the last rent change was applied).

Particularly for Melbourne property, a great many of our rental agreements were signed during COVID lockdowns and in periods where our rental eviction moratorium forced owners to be sympathetic to renter financial stress. An enormous number of rental agreements were deliberately signed at a price well under market value during this time.

However, many property managers have not discussed the correct post-COVID market rent, nor the timing of a potential rent increase with their landlord clients.

For those who release at a rent below market rent, they must realise that the next opportunity that they’ll have to apply a rental increase will be twelve months away*, (for those who are not on a fixed tenure eclipsing one year).

The challenge they’ll ultimately create for their tenant could be a rental shock. Applying a rental increase to catch up with past years of static rental movement cab be a tough blow for a tenant who didn’t see it coming.

And while we can’t correlate higher interest rates with rising rents, all investors with loans will be feeling the pinch with the heightened repayments. Many investors are currently discussing market rents with their property managers. If they are in doubt about the recommendations being offered, they should ask for comparable rental analysis…. just as we do with comparable sales analysis when it comes to appraising a property’s likely selling price. Applying CPI on an already low-base is not the right methodology.

Lastly, a good, loyal tenant is a great outcome for a rental provider. Applying a slight reduction on market rental can be a great approach, but managing the increases in step is far better than shocking them with a hefty increase after a three year lull.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU