This last of my three own investment examples isn’t what I’d call an accidental purchase, but nor was it primarily an opportunistic purchase. It was more of a safety purchase… but it’s worked out to be a great investment.

Back in 2008, as the depths of fear peaked during the GFC, we purchased a short-term home. We’d been rent-vesting for a while and an opportunity arose as a motivated vendor chose to privately sell his home on Gumtree. Unusual? Yes, but some vendors go down that path.

We bought a home that sat behind shops on busy Nepean Hwy in Aspendale. It represented a challenge in a few ways; it needed a full renovation, and we had a toddler who was good at running up driveways. We renovated the house, (again, the Royal “we”), but I did sand window frames and doors until my fingers bled.

As for the sprinting toddler, we arranged an electric roller-door at the end of our driveway at the street entrance. The letterbox needed repositioning as a result, so we affixed it to the side of the shop at the front, not thinking any further about it. Our daughter was safe and the roller door looked neat.

Some week’s later we received a disgruntled complaint from the owner of the leased shop at the front. He wasn’t too happy about our letterbox position. I asked him what his issue was. “Well, if I want to sell the shop, it may have a negative impact on my sale.”

So I asked him, “Do you want to sell?”

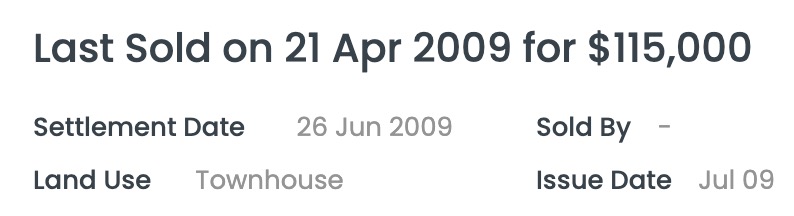

The rest is history. It was an off-market sale and he named his price. After some due diligence and negotiating, I secured the shop, (and it’s commercial tenant) for $115,000. The rental income covered the outgoings so it seemed like a reasonable deal.

It wasn’t that straight-forward, however. Commercial purchases rarely are. We had to either qualify for a commercial loan, or find the equity in other assets to come up with the funds. We did the latter, utilising our newfound equity following the renovation on the house behind.

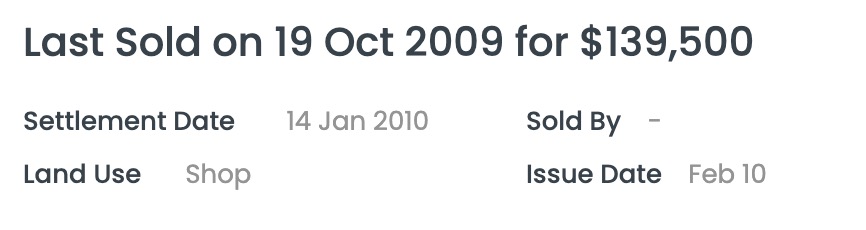

The investment proved to be a great one. Landlords don’t pay all the outgoings on commercial dwellings as they do residential dwellings. The cost of the property was low by any investor’s standards, and as soon as we’d generated a bit more equity, I approached the vendor about the other shop next door.

We’ve had consistent rental demand for both over the years and the capital growth has rewarded us too. The size of each shop is small, and as a result our maintenance bills have been quite manageable.

These days our two shops rent for $10,300 and $11,000 per calendar year; a 9% gross rental return on the purchase price.

Commercial property is not what I’d necessarily recommend for an investor starting out, because vacancies can bite when they occur, and capital growth hasn’t matched residential property. In addition, financing a commercial dwelling is a lot harder. Lenders work off commercial loan rates (which are higher), they require a much more significant deposit (35-40%), and they amortise the loan period to 15 years, which means that repayments per month are a lot higher than residential loan repayments on a 30 year loan term. For these reasons, I do have a saying.

“Treat commercial property like the red hotels on the Monopoly board. Get four houses under your belt before you buy commercial.”

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU