Over the past week I’ve had two prospective clients ask me about the suitability of their property selections as they canvas the market for their home. My responses to both were very similar. “I don’t recommend it at all.”

My reason was all about the zoning of the property.

Unlike some of my words of caution where I may highlight the risks or encourage the buyer to look into the implications of their choice, I am far more black and white about zoning. The difference between residential zoning and commercial zoning can make the difference between financing the purchase and losing the deposit completely. The trouble that certain zones can represent for residential pre-approval holders can never be underestimated.

A residential loan pre-approval means just that. The bank must consider it as a residential dwelling.

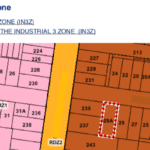

The first enquiry I fielded was in relation to a house on a busy road with a few industrial workshops in the immediate vicinity. The appeal of the property was the price tag. It seemed too good to be true. The issue was the zone. These buyers were not in a position to fund a 30-40% deposit on commercial lending terms.

The first enquiry I fielded was in relation to a house on a busy road with a few industrial workshops in the immediate vicinity. The appeal of the property was the price tag. It seemed too good to be true. The issue was the zone. These buyers were not in a position to fund a 30-40% deposit on commercial lending terms.

Finding out whether a property is residentially zoned (or otherwise) is not hard. Every single contract will mention the zoning.

Asking a lawyer or conveyancer to point it out is a simple request.

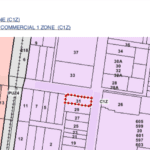

My second zone-related enquiry was only a couple of days ago. A lovely young first home buyer called to ask about a property he’d found that was not only selling off the plan (already enough to make me anxious), but also in a high rise block above shops in a Commercial Zone. He reminded me a few times that it wasn’t a commercial-flavoured unit. …”but what if it’s an obvious apartment?” …”but the agent said I just need ten per cent.” …”but what about if I ask another bank?” His objections continued. I had to point out the risk and tell him this;

“I can’t endorse it. All I an do is tell you why it’s a no for me.”

Banks may consider an apartment above a shop to be a residential dwelling… but if it is zoned Commercial and the property is purchased unconditionally at auction, what are the risks to the buyer? There are two significant risks:

- The bank may decide to enforce the commercial lending terms on the basis of the property being a Commercial Security. This means that the buyer will need a 30-40% bank deposit (as opposed to 5-10%) and commercial lending rates will apply. These are generally higher than residential and the loan term may be shorter. For most first home buyers who don’t have an emergency family loan on tap, they won’t be able to meet the loan requirements. The result is that they will rescind on the purchase, forfeit their deposit paid to the agency, pay the vendor for losses and potentially be sued.

- The bank may decide to finance the property on the basis of it being Residential (provided other residential policy requirements are met, such as minimum floor area being greater than 50sqm as one example). Even with the lender acceptance of the security, the buyer will potentially face hurdles if and when they go to sell the property, as another lender may decide to consider it a Commercial Security, or policy may tighten during this time. If other properties in the building are sold at a later date and the resultant sale prices are low due to buyer nerves (or inability to obtain residential finance), the valuation will remain low too, as these other sales in the building underpin the value of this asset.

There are many zones but it’s integral to be clear about what zoning the bank’s pre-approval is covering. A residential loan product can cover other zone types but usually in combination with the bank’s discretion, the valuer’s report and the borrower’s Loan to Value Ratio (LVR). A higher LVR will generally spell higher scrutiny. Loan amounts above 80% implies that Lender’s Mortgage Insurance (LMI) applies (in most cases). For many lenders the Lender’s Mortgage Insurer also assesses the loan application, not just the lender.

And in most cases, Lender’s Mortgage Insurer’s are even more strict than the bank.

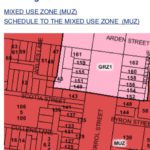

A Mixed Use Zone for one buyer might be acceptable with one lender and may be rejected by that same lender for another buyer. Lender and Mortgage Insurer appetite for a given property always takes into consideration the applicant’s exposure too. This beautiful townhouse in North Melbourne is a good example of a Mixed Use Zoning property and these inner suburbs are quite populated with Mixed Use dwellings.

Far right pic sourced from Urban Melbourne

The same can apply for an Activity Zone. Take this cute Victorian in Footscray as an example. The property is a beautiful terrace in a very central, convenient location but it had to be understood at the time of purchase that Footscray has a lot in store for it as Postcode-3011 undergoes an exciting transformation as outlined by local council and 2030 planning changes. The skyline has cranes dotted everywhere, the online plans show dramatic changes in the central streets, and buyers need to be comfortable with the idea that their streetscape and surrounds could one day become a lot busier.

Zones need to be checked against lending policy for every loan applicant before signing an unconditional contract.

Zones are specified for a reason and zoning can be integral to the future use, development potential, surrounding streetscape and exciting changes in store for an area.

They aren’t to be feared but should always be understood.

Loan pre-approval deserves careful attention, always.