In this tough investor market, the term “valuation shortfall” is dreaded by all. It is a banking term which means that the bank valuation is less than the price paid for a property. This is a particularly rare occurrence for an auction property but nonetheless, it is something that every buyer should be mindful of and prepared for with a contingency plan.

When a Valuation Shortfall strikes, it can range from moderately stressful to dire.

Valuation methods and scrutiny varies based on the lender and the borrower’s circumstances. Buyers who are borrowing at a level which places them into Mortgage Insurance territory need to be particularly aware of the process that their lender will be following post-sale.

Typically Lender’s Mortgage Insurance (LMI) is applicable above 80% borrowings, but some exclusions apply. A Mortgage Insurer will generally apply a degree of scrutiny and will likely have policy which they enforce on all buyers. For some lenders, the difference between 80% and 90% borrowings can translate to a ‘full valuation’ being required, as opposed to a ‘curb side’ or automated (computer modeled) valuation range. In most cases, if an automated valuation suggests an anomaly, a ‘full valuation’ will be ordered and a valuer will physically attend the property to conduct the valuation.

The implication of a valuation shortfall doesn’t necessarily spell disaster, and buyers don’t automatically ‘lose’ the property, but they will have to cough up extra money in some way, shape or form.

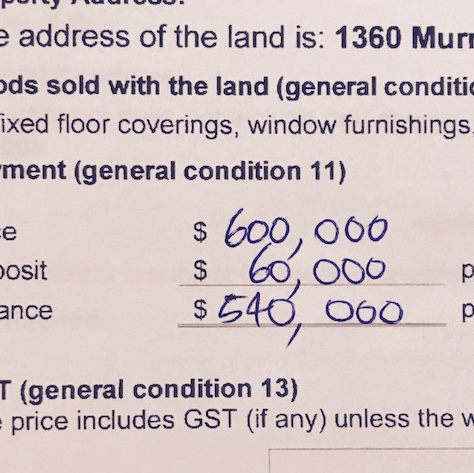

As an example, if a property is purchased at $600,000 on a 90% Loan to Value Ratio (LVR) and later valued at $550,000, the shortfall amount is $50,000. For the buyer, they have a few possible options;

- If the lender was prepared to fund 90% of the price, the $540,000 which was anticipated initially will become $495,000. The lender will only lend 90% of the valuation. The buyer will need to come up with the additional $45,000 on top of their 10%.

- If the buyer is eligible for increased borrowings to bridge the gap via a higher LVR, they may reapply for a higher loan, but they need to accept that most lenders are tough on increased LVRs and most maximum’s for Home Buyers are capped at 95% and lender options are more limited. In this specific example, even on a 95% lending basis, this buyer would only be able to source a maximum loan of $522,500. This leaves a shortfall of $17,500 still. The other additional cost is an increased LMI premium and this will need to be funded too.

- Some buyers are fortunate enough to have access to other borrowed funds; sometimes through equity and other times through parental and family loans.

- If the buyer is confident that the valuer has it wrong, there are channels they can go through to ‘contest’ the valuation, but it’s fair to say that most valuers won’t roll over easily if a non-valuer challenges their work.

If a buyer can’t complete the purchase, they face ‘rescission’ which means that the contract is voided and the vendor and agency retain the deposit and potentially sue the purchaser for any losses caused to the vendor. This is grim, but very rare.

There are a few mitigating actions that buyers can take in order to protect themselves from financial upset and personal angst. The first and most obvious is to be prepared at the time of setting a price limit or formulating an offer. Buyers need to have confidence that the price they are offering is fair and reasonable, and not an over-payment.

There are a few mitigating actions that buyers can take in order to protect themselves from financial upset and personal angst. The first and most obvious is to be prepared at the time of setting a price limit or formulating an offer. Buyers need to have confidence that the price they are offering is fair and reasonable, and not an over-payment.

Obviously there is a fine line between conservative and competitive.

A lack of recent past sales in the vicinity of the offer could spell trouble and buyers need to think like a valuer when they imagine which other recent sales data could be drawn on to support the price they paid.

A contingency, (or Plan B) is essential if the buyer is concerned that the property price tag could be scrutinised. Plan B’s come in a few shapes and forms: a War Chest of savings as a buffer, a available loan or line of credit, kind family members, an alternative Lender option, availability of a higher LVR loan, or an out clause.

In the case of an auction, it’s nearly impossible to have an out clause. A committed buyer needs to take the educated leap and back themselves when they go to auction. There is no ‘subject to finance’ at auction, but buyers can gain comfort from the fact that many capital city properties sell at auction, and all buyers are in the same boat. For a private sale or post-auction negotiation however, buyers who are nervous can consider a ‘subject to satisfactory valuation’ or ‘subject to finance’ clause.

Last year we faced a valuation shortfall situation with a dear client. We had made a move to purchase an attractive investment property prior to auction. Our comparable sales analysis indicated high fours was an appropriate value. After submission of a contract for $480,000, our negotiations with the vendor resulted in agreement at $487,000; a fair price (or so we thought). We knew that our client didn’t wish to buffer any shortfall and we felt protective of their interests.

Last year we faced a valuation shortfall situation with a dear client. We had made a move to purchase an attractive investment property prior to auction. Our comparable sales analysis indicated high fours was an appropriate value. After submission of a contract for $480,000, our negotiations with the vendor resulted in agreement at $487,000; a fair price (or so we thought). We knew that our client didn’t wish to buffer any shortfall and we felt protective of their interests.

The bank valuation came back at $460,000; a considerable percentage differential. We had a condition in the contract and were able to walk away from the purchase, but the property proceeded to auction and sold under the hammer a few weeks later for $485,000. Perception is just that; one person’s idea may not necessarily align with another’s.

The importance of due diligence, comparison with other recent sales and preparation for the unexpected is really important when buyers are borrowing above 80%, and likewise when they buy off the plan. Scrutiny is somewhat increased for off the plan securities and any buyer who enters an unconditional off the plan contract without a contingency is putting themselves at risk.

Aside from the higher scrutiny applied to such contracts, most bank valuations will not take place until the property is ready for settlement. In some cases, this can be two or three years’ away. Betting on a property sale price matching up in a future market is just that; a gamble. Even more so, such purchases definitely deserve caution and contingency.