Bear Markets always create a change in emotion for buyers. Those who have been anxiously pushing themselves at auction during a Bull Market seem to forget the desperation they felt to just secure their property, sometimes anyproperty in the face of what felt like a brick wall between them and their acquisition plans.

Fast-forward the clock twelve months though, and some of these same folks are now standing back, arms folded, convincing themselves that it’s a terrible time to purchase because the market is falling. Never mind the fact that they were prepared to pay a premium price mid last year, but are now reluctant to pay a discounted price for the same stock.

The reason for this is based on fear. Fear twelve months ago that the property market would gallop away and leave them clutching their unspent bank cheque while the property of their dreams vanished out of sight. Or fear today that they may buy their home and wake up next month to find that they could have bought it cheaper if they’d just held on.

But why do so many humans adopt this theory when the obvious option in today’s market could be a better one than this time, last year? If you’d asked the underbidder of a heated auction in July 2017 whether they’d be happy to know that in one years’ time they could buy the same property for a 5% discount, and with less competition getting in their way, you’d think that the answer would be “yes”.

But why do so many humans adopt this theory when the obvious option in today’s market could be a better one than this time, last year? If you’d asked the underbidder of a heated auction in July 2017 whether they’d be happy to know that in one years’ time they could buy the same property for a 5% discount, and with less competition getting in their way, you’d think that the answer would be “yes”.

But it’s not for most.

Not very many buyers opt to purchase counter to the market, but it may land as a surprise to know that some of the most successful business people actually have chosen to do so. As Warren Buffet says;

“Be greedy when others are fearful, and fearful when others are greedy.”

The theory is certainly interesting when investment is concerned, but it does cause me to ponder why a homebuyer targeting their long term home would try to gamble on the market when the theoretical loss or gain is not going to be crystallised in the short term.

To rephrase that, when we consider Melbourne’s long term property market performance and combine that with the fact that the average time frame for a family home to be held by the same owner is ten and a half years (Source: CoreLogic), the impact of waiting it out in an effort to time the market presents more risk than upside for many.

For starters, the delay in purchasing a suitable family home translates into delayed gratification. Every month or year that the buyer holds back from securing the home that they could secure if they chose equates to another month or year(s) that they are missing out on something that they could be excitedly enjoying. Life is short.

To compound this, even if they did manage to secure the property at a ten per cent discount to what they could have spent at the time of being ready, over the course of the average tenure this ten per cent starts to fade as long-term capital growth highlights the benefit of time.

The potential in this current climate for the financier’s maximum borrowing capacity figure to either diminish or disappear altogether is real. Our lenders are tightening their policy by the week and many buyers who could have borrowed $X three months’ ago are now finding that they can borrow a reduced figure to this, and in some cases the figure is significantly reduced. Unfortunately we’ve seen recent situations where Autumn’s eligible buyers are no longer eligible to borrow in Winter based on policy change around their work status, residency status, or other policy-related changes.

Trying to time a trough and missing out on buying altogether is no win at all.

Lastly, working out when the market has reached its trough is indeed a very difficult thing to do. As professional buyers who are interacting and transacting in the market every day, even we can’t pick the peaks or the troughs perfectly. We can do it within a number of weeks, but even then it’s impossible to accurately pinpoint.

I recall back in 2011 when the market turned Bear. A series of weekends with interesting pass-ins were the hallmarks, but even then they were intermittent and ‘patchy’. Some dwelling types and suburbs were out-performing others and I couldn’t put my finger on the peak for some weeks. In hindsight I can recall the month that it turned, but only in hindsight.

This Bear market we find ourselves in is quite different to our last one in 2011-12 because it has different market forces driving it and we have conflicting global market dynamics around us. What’s more, our market is two-speed while the lower priced segment of the market in the inner and middle rings is still exhibiting Bull Market hallmarks.

Lack of available credit for many, a likely change of government (and potentially our policy around negative gearing), continued low interest rates (which I believe will continue for at least another year) leave us standing in an unusual market.

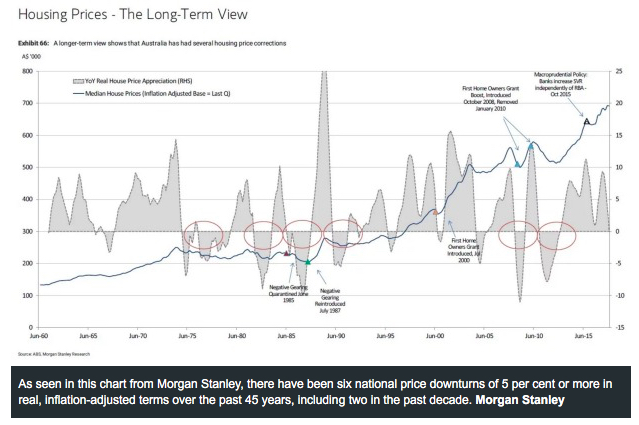

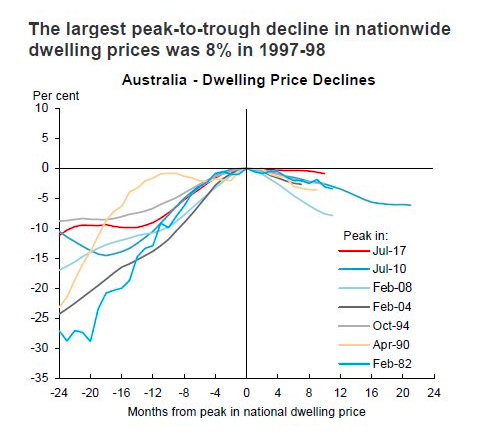

As this chart demonstrates, Australia has experienced “six previous episodes of declining housing prices since 1980, with the peak-to-trough range of 2.5% to 8%,” analysts report. (Source: Macquarie, Business Insider)

“Given current supply and demand-side considerations, along with the view that banks are unlikely to take actions that will exacerbate price declines, Macquarie thinks the current housing market downturn will be modest and orderly in nature.”

“They also believe that unlike previous downturns, higher mortgage rates are unlikely to create headwinds for prices given the likelihood that official interest rates from the RBA will be left unchanged for the foreseeable future.”

Whether readers share the same view of this or not, the two graphs certainly demonstrate that peaks have outweighed troughs historically and the length of time for recovery from a trough for our eastern capital cities has been relatively short.

Trying to time the market carries risk.

Whatever your opinion and decision if you are in the market for a family home, consider the downside to waiting it out.

Whatever your opinion and decision if you are in the market for a family home, consider the downside to waiting it out.

My personal philosophy when it comes to purchasing investment property is simple.

“Start as early as you can.”

As a great industry colleague always says:

“It’s all about time in the market, not timing the market.”