Since the GFC, this term has become a well-worn one in banking and finance circles, but so few understand what it really means, and why it’s become so important.

Recent news articles in this past week suggest that it will strike again, and some commentators, agents and investors alike are mindful of macro-prudential measures being employed again in an effort to tighten the supply of credit.

Quite a few people fear the idea of macro-pru.

But without understanding the variety of options that our banks and regulators have, and the reasons for turning to MacroPru in the first place, the sheer fear of it can outweigh the reality of it.

Our property market is fuelled by a combination of things, but sentiment is a major component.

Being cognisant of the reasons why macro-prudential measures are being considered is essential. This type of action is never a cookie-cut, ‘black and white’ approach. Economic landscapes change constantly and every assessment on any given occasion is different, based on the factors that are contributing to heightened risk.

Macro-prudential regulation is a methodology applied by regulators to mitigate risk to our financial system. It typically relates to the supply of credit, and like many modes of regulation, regulators and banks can segment the categories of customers that they wish to apply different levels of supply to. MacroPru doesn’t only limit supply. It can also heighten supply.

The best way to picture macro-prudential regulation is to imagine a set of levers.

Each lever represents a different type of action, and when enforced, we see our lenders circling in on some of these policy changes, (among many);

- The amount of credit supplied to a borrower as a function of their income and expenses, (as a percentage of debt to uncommitted income)

- The amount of credit supplied to a borrower as a function of their total debt position, (as a percentage of debt to assets)

- The amount of lending that is permitted as an interest only loan vs principal and interest loan

- The degree of leveraging permitted for a purchase

- The flow of credit via equity release for non-investment purposes

The most recent CoreLogic report for September delivered us the headline that many of us were already anticipating. At the coalface around our nation, the sheer rate of capital growth is palpable in almost every market.

Agents know it, buyers know it and tenants know it.

The issue that we have on our hands at present is two-fold, and it is very different to the post-GFC era. Our asset price growth is particularly strong around the country in both capital and regional cities. Since COVID lockdowns impacted our landscape, many regional markets have also experienced heightened demand from homebuyers who have decided to make the move from the city, for whatever reason.

COVID-19 has influenced homebuyers to seek larger homes with additional work from home spaces, and low interest rates have enabled buyers to borrow more. Multiple federal and state-based incentives have stimulated segments of our markets, and buyer appetite has gone through the roof. Surprisingly, despite commentary around low stock levels, our stock supply has been stronger than previous years and our sales activity has also been higher.

With zero new migrant arrivals, higher stock supply and a pandemic in our midst, it seems crazy that we have more hungry buyers than sellers.

But we do.

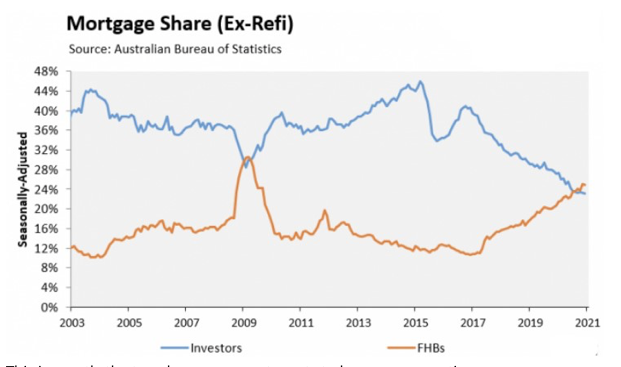

Although we have seen the return of investors over the past twelve months, it’s still clear that it is owner occupiers who are fuelling the exceptional price growth. From first home buyers to upgraders to down sizers, the rate of growth has been so heady that it is nearly impossible for our economists, politicians and regulators not to suggest that something may need to change.

Unlike 2014-2019, though it is not the investors who are dominating the market, and in particular – stealing opportunity from first home buyers. This chart illustrates this perfectly, thanks to Tim Boyle’s weekend newsletter on 3 October 2021. The two collectives in this chart are only investors and first home buyers. The lion’s share, (which is not on this chart) is represented by upgrading/downsizing owner-occupiers.

It is important to note that the regulators are not suggesting that house price growth is reversed. The mentions of macro-prudential restrictions coming into place are only mentions at this stage. The commentary we have all been privy to at this stage relate to ‘keeping an eye on the property market’ and to consider ways to slow the pace of growth.

Slowing the rate of growth is entirely different to stopping growth.

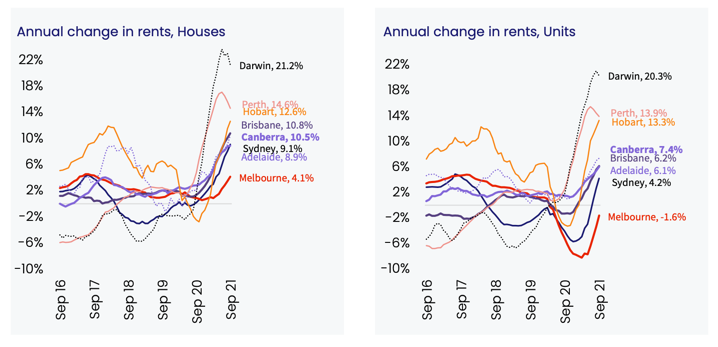

Some key differences in today’s market, (as opposed to the pre-2020 market) are rental vacancy rates, housing shortage figures and rental growth. We have a housing shortage crisis across our nation and our regulators and politicians will be only too aware of the negative impact of quashing investor activity.

Quashing investor activity will have a compounding detrimental impact on households who rent.

We now find ourselves observing a market with strong house price growth recorded in both regions and capital cities, with first home buyers borrowing energetically, yet with a moderate representation of returning investors.

Every lever is available, but which one do our regulators choose?

Slowing down owner-occupier’s ability to stretch themselves harder when it comes to borrowing is one possible approach, and this could be done sensitively with the adoption of increasing what we term ‘buffer rates’. When an applicant applies for a loan to purchase property, the lender assesses the borrower’s ability to pay the debt by calculating their uncommitted income and the projected repayments. The repayments are not calculated using the current interest rate, however. The lender factors in a buffer to account for interest rate rises and other stresses to the current repayment forecasts. Currently the buffer sits at circa +2.5%pa, (this varies among lenders, products and applicants). What this means is that a borrower who is eligible for a 2.5%pa interest rate has been deemed to be able to repay the same loan at 5%pa. Previously this buffer was a greater amount.

If our regulators and lenders do decide to employ any macro-prudential moves, this is what I think they will gravitate to: increase buffer servicing rates.

By slightly increasing the servicing rate on the lending calculator at the time of credit assessment, (to account for a higher buffer) a borrower’s maximum borrowing capacity will be decreased. If a marginal decrease is applied to future borrowers over the coming months/year, we can anticipate the following;

- Those buyers who decide to borrow to their absolute maximum will find that their maximum funds on hand are reduced. They won’t be able to compete at quite the same price point as they had previously,

- Those buyers who could borrow more but choose to conservatively borrow less than their maximum borrowing capacity will be unaffected,

- Investors can still borrow, but they too can’t stretch like they could have previously,

- Investors who require stronger rental returns in order to borrow will be far more likely to enter the markets that are desperately crying for rental stock, (the general correlation between rental shortage and location is in the higher yielding markets),

- Buyers who are consequently priced out of the market that they initially chose will either downgrade their spend level in the same market by targeting locales further from CBD or in the regional markets nearest to their capital city.

The impact of MacroPru deserves a thought, but the likelihood and specific MacroPru actions are what we should be paying careful consideration to.

It is both unsustainable and unhealthy for our markets to continue to perform at +20%pa. A gentle cooling of the pace of growth is not a bad thing.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU