For decades, economists’ predictions have hit the newsfeeds and influenced forecasting, opinion and buyer/seller behaviour. But how often do they get it right?

Over the last twenty years in particular, (a familiar time for many of us as property investors), we have watched the negative news headlines come in waves throughout the post-Keating era, The GFC, the ‘housing bubble’ period of heightening household credit, COVID, and more recently; the quick and successive interest rate rises.

Economists have weighed in, with plenty predicting significant house price falls, and some predicting colossal falls.

One of the more memorable doomsday claims was Professor Steven Keen’s assessment that our local housing market would fall by 40% following the GFC, citing poor economic management in relation to the Rudd stimulus and other key actions by our government of the day. Another well-known economist challenged him on this with a bet. We all remember his Mount Kosciuszko climb, wearing the T-Shirt stating that he got it horribly wrong.

“As one of the conditions of the wager made in September 2008 with Macquarie interest rate strategist Rory Robertson, Keen will be wearing a T-shirt silkscreened with the words, ”I was hopelessly wrong on house prices – ask me how”.” (Sydney Morning Herald).

Some years later during the ‘credit crunch’, (which ranged from 2015-2019 and intensified in the late stages of this time range), predictions about housing bubbles plagued our newsfeeds.

Things got interesting when COVID hit our shores, too. AMP’s report, (like many) shared a variety of potential outcomes via their forecasts. Base cases and high risk cases were not necessarily separated by journalists, and many headlines clutched the high risk case forecasts. However, most of them didn’t predict the intensive capital growth surge experienced in many cities and regions during 2021.

“The Australian housing market is at risk from the coronavirus recession Australia has now entered. A relatively short recession that sees unemployment rise to around 7.5% would likely only set prices back around 5% or so after which prices would bounce back. But a deeper recession with say 10% unemployment risks tripping up the underlying vulnerability of the housing market around high prices and high debt levels. This could see a 20% fall in prices. This is not our base case, but it highlights the need for the Government & the RBA to minimise the fallout from coronavirus shutdowns in terms of businesses and jobs.” (Source: AMP Capital)

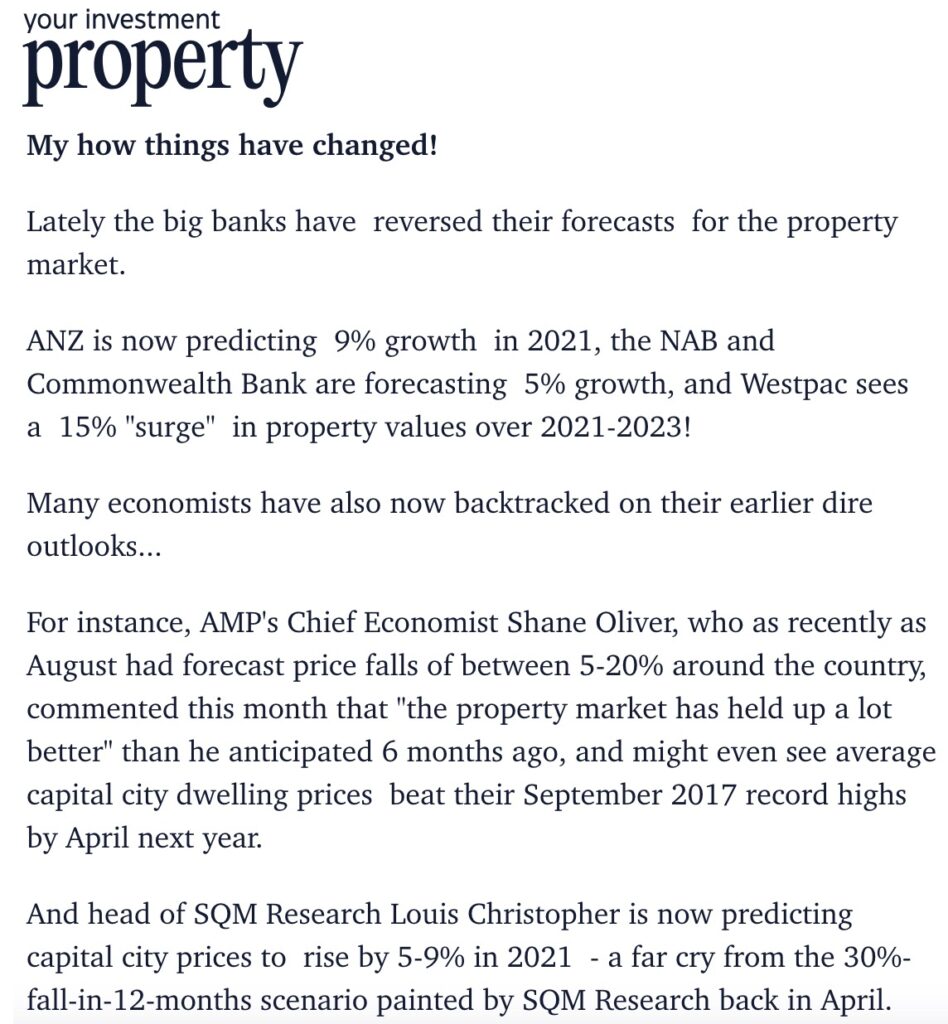

An interesting read by Your Investment Property highlighted some of the incorrect forecasting made by the major banks at the time, though.

“In May [2020], Westpac and the ANZ were both predicting a 10% decline in national property values. The NAB predicted falls of up to 15%.

Not to be outdone, the Commonwealth Bank also made headlines in May with a claim that house prices could collapse by up to 32%.” (Source: Simon Buckingham, Your Investment Property)

Only two year’s later and following one of our biggest runs of capital growth during 2021, plenty of economists quickly reverted to more dire forecasts again in the wake of our rapid cash rate hikes.

“Westpac chief executive Peter King expects house prices will fall 10 to 15 per cent over two years after a run of extraordinary growth but says the bank’s mortgage customers are well placed to absorb interest rate hikes.”

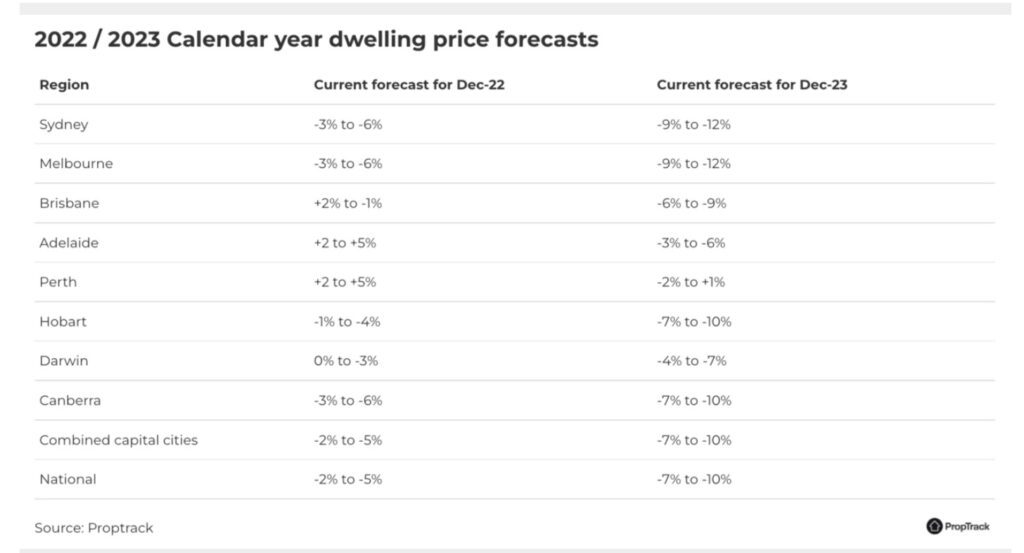

And Prop Track predictions painted a stormy picture in 2021 also, with this array of forecasts;

Winding the clock forward two years, and reviewing the updated forecasts from our major banks’ economists is an interesting exercise.

“After CoreLogic reported prices rose 0.5 per cent in April following March’s 0.6 per cent gain, Commonwealth Bank became the latest major bank to revise its forecasts on Monday. With prices only falling 9.1 per cent peak to trough, CBA has abandoned its forecast of a 15 per cent fall and instead is looking for a 3 per cent gain in 2023, and a 5 per cent rise in 2024.

AMP’s veteran economist Shane Oliver did something similar, conceding his call for prices to fall between 15 per cent and 20 per cent was off the mark; he now expects prices to be flat in 2023 and rise roughly 5 per cent in 2024.

“As an economist I do find it very humbling right now,” says Oliver, who describes this as an “odd” housing cycle. “There are so many conflicting forces that it does make it hard to read.”” (Source: AFR May 2, 2023, James Thomson)

Our market’s resilience has many stumped. There isn’t a single factor that has fuelled Australian property price growth in the face of consecutive interest rate rises though; we have multiple factors. There are a lot of moving parts, and of course, there are markets within markets. Strong employment, heightened demand with record levels of migration, slow building starts and accrued household savings during the pandemic certainly aided this resistance to price falls.

Now that our increasing interest rate cycle is at, (or close to) its peak, 2024 will be an interesting year to ponder.

Tight listing supply likely insulated our major markets during late 2022 and early 2023 from harsher price falls, but interestingly our late burst of listings in 2023 haven’t saturated our market at all. Listings have been soaked up by strong buyer activity and values have consistently risen in most cities.

With migration levels continuing to surge, we can anticipate anything but a dull year ahead.

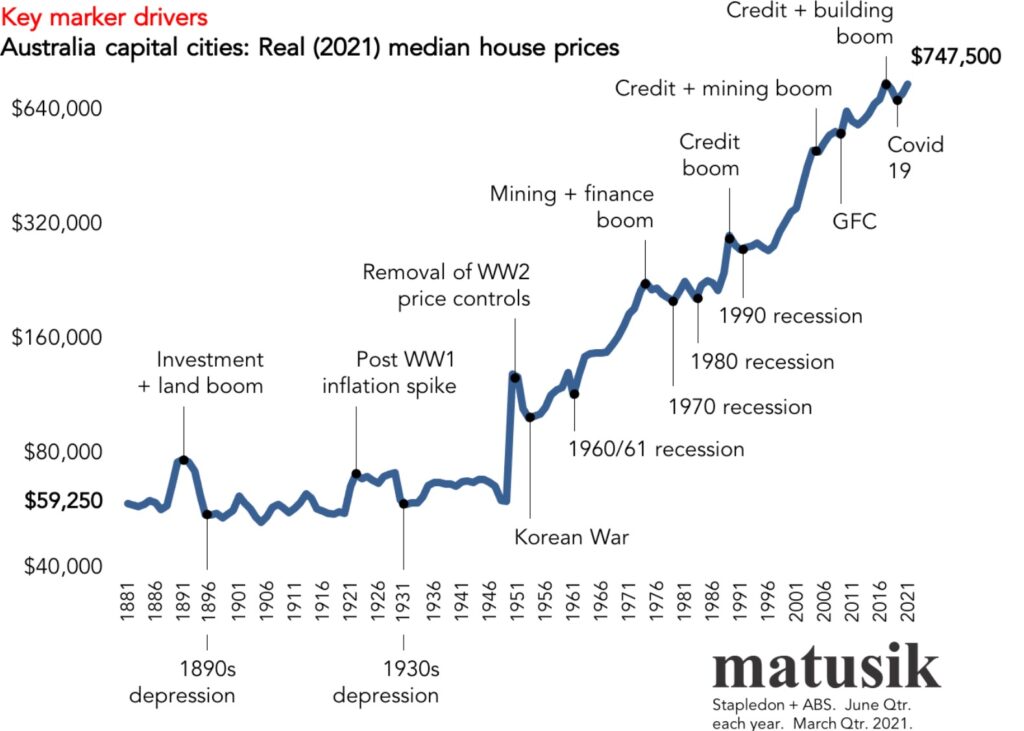

Credit and thanks to Simon Pressley, who generously shared some great historical snapshots with me recently to aid this blog.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU