I remember Friday 13th March well. We all woke up to the p-word.

Pandemic.

The world health organisation had declared it, and it wasn’t until that point that things really started to feel more serious for us. In the real estate world, our introduction to the pandemic was the elbow-touch. As a relatively friendly and tactile bunch, this was our State’s best alternative to handshakes.

Buyers immediately asked me what the pandemic could do to the property market. We canvased as many drivers and threats as we could, but the reality was that this pandemic was moving through the world at a faster pace than we’d imagined, and as Europe data hit the airwaves, it became abundantly clear that this contagion was serious.

And then we had lockdown.

In the space of just one week, we’d gone from auctions and elbow nudges to a two-person rule, strict appointments only, online auctions and a very demure number of buyers remaining.

But vendors who had to sell were still on the market, hoping desperately that their agent would come to them with an acceptable offer that would enable them to meet their financial obligations.

It was a tough time for many.

During 20th March to 4th April, almost all of our our book of clients chose to go on pause. Only a handful of buyers remained committed to their purchase strategy.

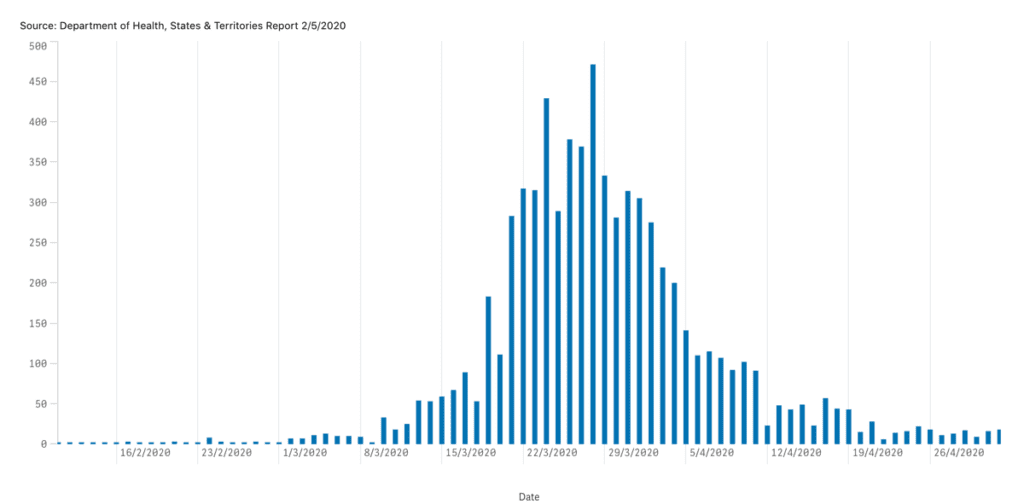

This coincided precisely with the sharpest increase in daily numbers of COVID-19 cases in Australia.

This matched our rate of diminishing buyer numbers

What was MOST intriguing for us following this difficult period was calculating the degree of approximate price discounting for all of the properties that we bid for/negotiated over the COVID-19 lockdown period.

Using comparable sales analysis, our appraised values for each property were provided to our clients on each occasion and we were able to approximate the level of resultant price discounting for each sale.

This is not an exacting science, because prices can be influenced by several factors, and not only restricted to market conditions. Vendor time pressure, difficult tenants, restrictive access, and so on are all relevant factors to take into account, particularly in this challenging period.

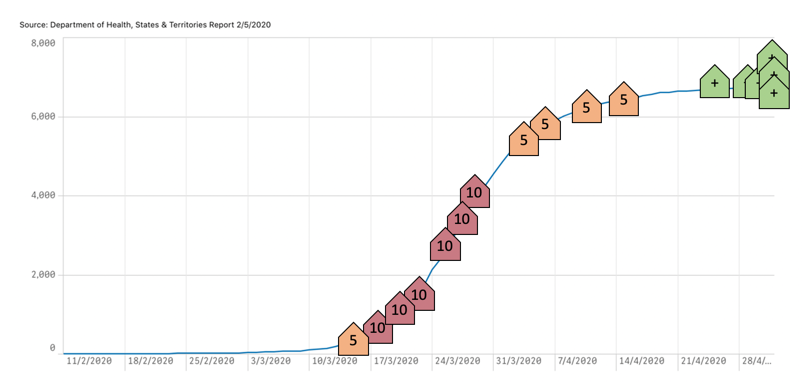

However, what we did note was that our first ‘good buy’ was at auction on 14th March; the very day following WHO’s declaration of the pandemic. We secured a beautiful Californian Bungalow some 5% under our appraised value in Melbourne’s inner NW.

Following this purchase, our market conditions deteriorated and the six purchases that proceeded that last public auction were indeed more representative of the tough conditions.

This chart below tracks each purchase effort we’ve been involved in since COVID-19 gripped Australia.

The houses are denoted in colour and number to signify an approximated degree of price discounting (as a percentage). The green houses denote either a result that we deem in line with pre-COVID-19 market values, or a competitive result that eclipses the vendor’s ‘reserve’. I note that all green houses were competitive purchases with multiple bidders. The five at the far right hand side are all unsuccessful efforts on our part; each of these negotiations had multiple buyers fighting it out. Yesterday’s two online Zoom auction results were significantly higher than reserve.

The red purchases included some of these acquisitions; all secured during the 20th of March and 4th April.

Our last newsletter highlighted some of our favourite recent purchases, each secured by somewhat contrarian buyers.

The change in sentiment, however started to become palpable just after Easter time.

Journalist articles varied, with reports ranging from a stabilising market to fears of up to 30% price falls. Christopher Joye of Coolibah Capital may have felt as though he was out on his own there for a while. He boldly reported back at the end of March that our new cases curve was flattening and that we were passing through peak infections.

As this became more obvious, and in particular, once our nation grew confident that our government’s next likely moves would be a reduction of social restriction, (as opposed to increasing measures), our buyer enquiries started to increase again.

In line with this increase in buyer enquiries, some of our existing ‘on pause’ buyers decided to return to the market.

Our purchase efforts changed from agent negotiations to competitive buying situations very quickly. No longer did we have the luxury of a simple one-on-one negotiation, and our Zoom auctions and negotiation scenarios suddenly included other buyers too.

By mid April, our COVID-19 price discounting was starting to diminish. The sales that followed demonstrated the correlation between the rate of daily new cases and price discounting.

It is little wonder, but intriguing to analyse.

The challenge we face going forward is not just restricted to new case numbers or a re-infection. We also have to consider our rate of economic recovery, lending restrictions, government policy change (particularly in relation to taxation), trade wars between China and the US, global demand for our exports, and most relevant to our domestic property markets, supply and demand ratios.

We have short supply now, but we cannot be completely confident that some distressed sales won’t occur in the later half of 2020. It’s been a tough time for many businesses, and our rate of, (and ability to) recover is yet to be seen.

But right now, the bargains aren’t out there like they were a few weeks ago.

That particular ship has sailed.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU