Melbourne and Sydney both delivered dismal auction clearance rates this weekend; each sitting under 50%.

This marks our lowest point so far this year, and it could well slide below that figure in Melbourne next weekend as we bulk up our auction numbers in what some would term a Super Saturday, making room for our local agents and vendors to enjoy the Melbourne Cup Weekend celebrations (and likely long weekend for most) on Saturday 3 November.

While the headlines can appear gloomy, these low auction clearance rates are predictable, particularly in Melbourne. As documented by Dr Andrew Wilson (an Australian Chief Economist) earlier this morning, “Melbourne results have tracked Sydney recently and recorded a Saturday published rate of 48.6% compared to the previous weekend’s 515 and well below last year’s 74.5%.”

Interestingly though, compared to Sydney’s 550 auctions yesterday, Melbourne had 1003, off the back of 1055 last weekend and a likely Super Saturday figure next weekend.

Interestingly though, compared to Sydney’s 550 auctions yesterday, Melbourne had 1003, off the back of 1055 last weekend and a likely Super Saturday figure next weekend.

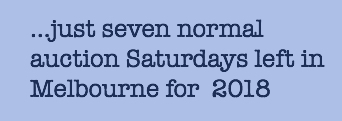

We have a lot of scheduled auctions. And only seven weekends so squeeze them into.

This calendar shows ‘normal’ weekends in green, likely high-volume weekends in red and our holiday weekends in blue. In true Melburnian style, we’ve packed our Spring listings into the very latter part of spring and as we approach the start of Summer, agents are cramping auctions into their diaries and we’re just starting to witness mid-week evening auctions, more Sunday auctions and some 9.30am Saturday time slots.

This speaks volumes. We have stock.

Interestingly though, not all property sales are struggling, and not every eligible buyer is having an easy time picking off low hanging fruit.

Last weekend we missed out on a 2BR apartment (below left) in Prahran when buyers were out in force. The unit sold under the hammer for $720,000. Our same client met success yesterday though when she secured a beautifully renovated 2BR unit in St Kilda East for $680,000.

Competitive conditions at this highly contested period house in Coburg were tough last Saturday with a hefty number of bidders, including four advocates fighting it out (below right). Good properties are selling, particularly when other similar style properties aren’t going to auction at the same time and posing a threat to anticipated buyer numbers.

When property gluts arise in given suburbs for specific dwelling types, price volatility becomes more likely and some properties, despite agents’ best attempts are selling for prices lower than anticipated. We secured this period property in Williamstown last week for $860,000 for an excited investor client who studiously covered the market and pounced with an offer at just the right time. Featuring a generous downstairs bedrooms and a second upstairs loft bedroom, this stylish property will attract a professional tenant easily when settlement approaches.

When property gluts arise in given suburbs for specific dwelling types, price volatility becomes more likely and some properties, despite agents’ best attempts are selling for prices lower than anticipated. We secured this period property in Williamstown last week for $860,000 for an excited investor client who studiously covered the market and pounced with an offer at just the right time. Featuring a generous downstairs bedrooms and a second upstairs loft bedroom, this stylish property will attract a professional tenant easily when settlement approaches.

Likewise, just yesterday we proudly secured a nicely presented, two bedroom strata title apartment in Elwood for an interstate investor family for $475,000. By anyone’s measure, that is good buying.

Likewise, just yesterday we proudly secured a nicely presented, two bedroom strata title apartment in Elwood for an interstate investor family for $475,000. By anyone’s measure, that is good buying.

The broad issue is – we still don’t have strong buyer numbers. While many wish they could take advantage of these opportunistic conditions, banks have almost ground to a halt with their lending ability thanks to two tough forces;

- APRA’s intervention in an effort to subdue house price growth rates and investor market domination, and

- Banking Royal Commission’s enforced tougher scrutiny on lending practises

With less borrowers and higher sale numbers, our supply:demand ratio this spring has completely tipped in favour of the buyer.

The important questions are:

- How long will it continue for?

- Will the opportunities become more (or less) abundant after Christmas?, and

- What changes going forward could better balance our market again?

Despite mixed opinions, I believe that there are some tough forces at play for Vendors now but they are easing. Firstly, our buyer:seller ratio in any Spring selling season doesn’t work optimally for vendors. Competing vendors can wreak havoc on many a campaign. Once Spring is out of the way and following our holiday period for most of January, moderated listing numbers in 2019 should equalise the conditions a little more.

Secondly, the banks are easing their lending policy. It may take a few months to filter through, but assessment times are starting to contract again, enticing offers are being thrown out to new borrowers (including investors), and APRA have openly eased some of the investor caps they earlier placed on our lenders. These advertisements aren’t restricted to just the major banks either. Offers of travel points, cash-backs and lower rates are dominating our bank’s advertising space.

And lastly, feared or not-feared, if Labour does win the Federal election next year, Bill Shorten’s promises to change negative gearing could come into the fore. A rush of investor activity in the first half of 2019 in an effort to capitalise on cementing the negative gearing benefit (provided Shorten’s ‘grandfathering’ commitment stays in place), could certainly alter the current landscape for buyers.

And lastly, feared or not-feared, if Labour does win the Federal election next year, Bill Shorten’s promises to change negative gearing could come into the fore. A rush of investor activity in the first half of 2019 in an effort to capitalise on cementing the negative gearing benefit (provided Shorten’s ‘grandfathering’ commitment stays in place), could certainly alter the current landscape for buyers.

So the question remains; is now a good time to buy?

We think so. We believe that between now and Christmas Eve will give rise to some particularly sharp opportunities for buyers.

We just aren’t so confident that he same advantageous opportunities will be in abundance for 2019.

Shorten pic sourced from The New Daily

Property pics sourced from REA

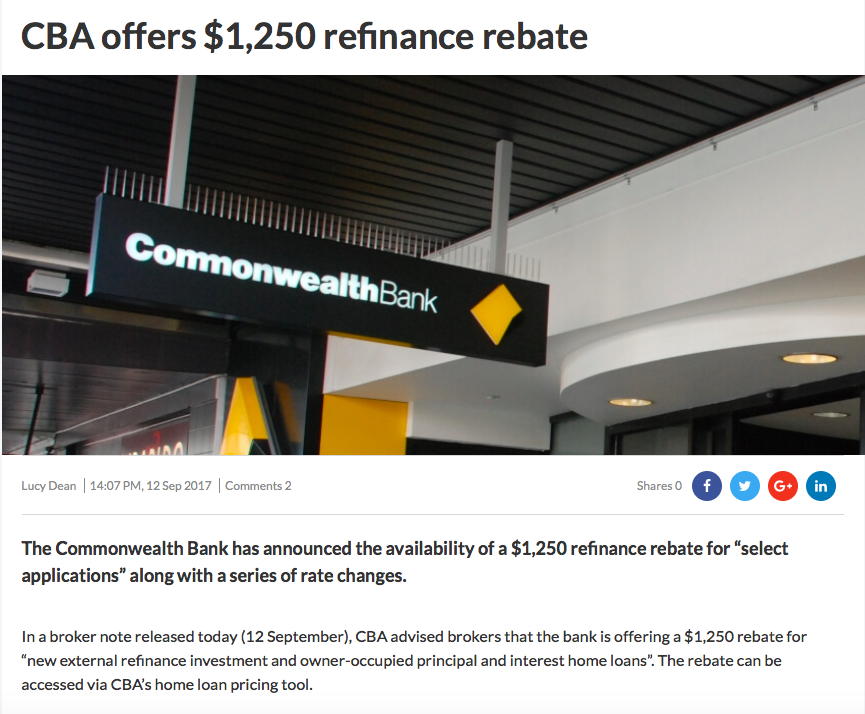

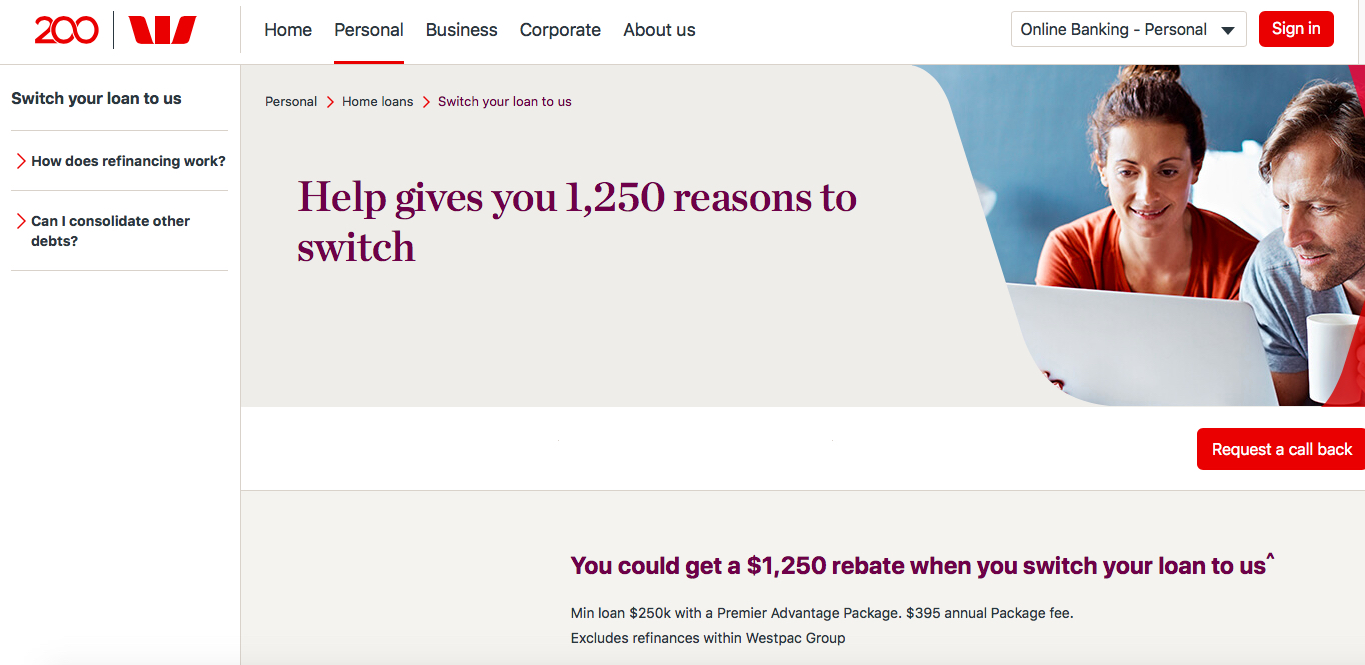

CommBank pic sourced from The Advisor

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU