I am often asked by prospective buyers, “Cate, what is the minimum budget recommendation you have for Melbourne?”. Sometimes, a client’s budget may be better-suited to a region, but for those who are keen on Melbourne, it’s important to consider the pro’s and cons of certain price points before jumping in.

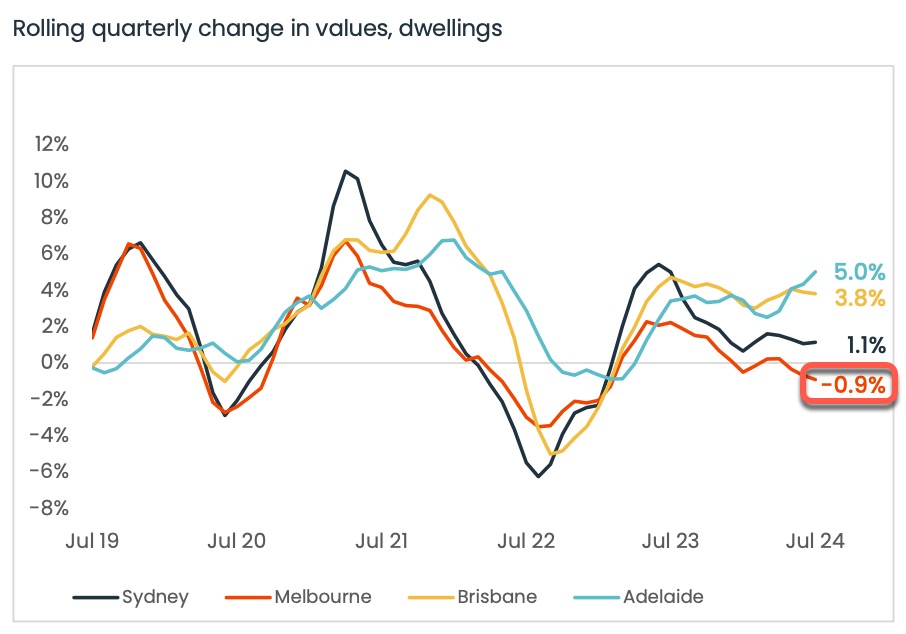

Melbourne has certainly been experiencing increased investor interest of late; mostly speculative or opportunistic. The capital growth performance has been static; in fact, Melbourne dwelling values are now -4.4% below the record high, which was in March 2022.

Opportunistic investors are circling the growing disparity between Melbourne and other capital city median dwelling values. The buying conditions are much softer than Perth, Brisbane, Adelaide and Sydney’s, and the perceived value proposition is strong too. In addition, rental yields have strengthened and in response to the State Government’s land tax and tough rental reforms, rents are still growing in Victoria as landlord-driven sales continue to outpace other states.

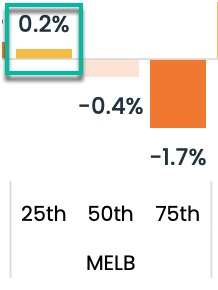

Melbourne is indeed an interesting market. The lower quartile of our market is currently the only segment that is performing positively. The residual is still in decline.

Growth of 0.2% is hardly a hot/competitive market, but it serves to show that the lower priced properties aren’t in decline. In fact, at the coal face, these are the properties that are experiencing reasonable competition. First home buyer activity is solid in Victoria.

In addition, investor budgets have been slashed by increased interest rates and higher loan servicing requirements so many investors have circled back to the unit market.

It’s little shock that this is the most resilient segment of the market.

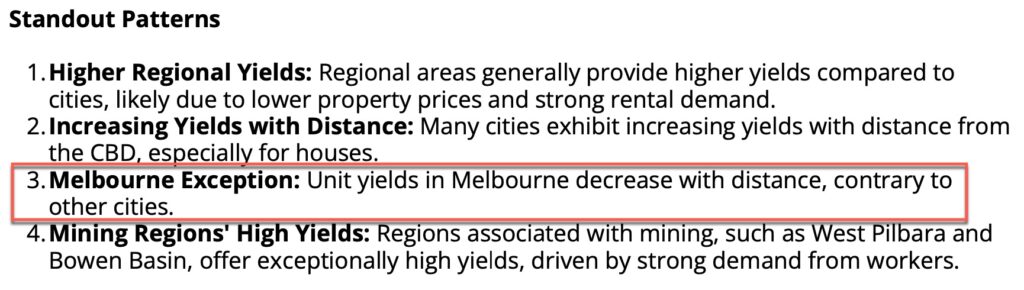

Historically, I’ve suggested that an entry point of $400,000 in the Melbourne market would sit at the comfortable minimum in my view. This budget enables an investor to target a two-bedroom unit in a location supported by rail, local amenity (e.g. shops and cafes), and a healthy renter demand. A recent study by MCG Quantity Surveying shed some interesting data on rental yield and the relationship between this yield and distance to the city CBD. The study focused on capital cities and regions alike, and Melbourne proved to run counter to other markets when it comes to unit rental yields. This could be due to a combination of reasons.

We canvassed a few ideas on a recent episode of The Property Trio podcast.

- Our city is quite oversupplied with units, compared to other cities.

- Our city is sprawling and amenity/connectivity is not great in the outer areas

- Most renters who choose to rent an apartment do so because they want better connectivity with their friends/family/work/lifestyle and they want shorter commute times

A $400,000 budget won’t easily enable a suitable 10km, inner-ring two bedroom unit purchase but it will allow an investor to target some great middle-ring options (and also some gentrifying areas such as Footscray). Once the investors’ distance from CBD increases, the anticipated returns start to diminish. The chances of a tougher socio-economic demographic rental market need to be weighed up also.

The question remains though, can a one-bedroom unit delivery great long term results? Traditionally we have avoided these types of assets, as banks don’t like floor areas that are under 50sqm. Some banks will consider 40sqm+ properties, but they are tough resales for this ‘high scrutiny’ reason. Even if an investor is adopting a ‘buy and hold’ approach, it’s important to recognise that things can change. The one bedroom properties take longer to sell and many of the target buyers have insufficient deposit sizes to get over the Lender’s Mortgage Insurance hurdle.

Unlike Sydney with their apartment-centric market, Melbourne’s units have been particularly stagnant in terms of performance. Melbourne has experienced over-supply issues in the unit market space for over a decade now, and while units are showing positive signs of growth, it’s still early days.

There are some great other inner-west areas I’d happily target for early fours including this unit that recently sold for $425,000. While I’d prefer it offered northerly aspect and a balcony, it serves as a good example of an entry level, renovated option for an apartment investor.

There are city apartments on offer, but they generally have particularly high strata fees that erode rental profits completely. And I’d never buy an investment property apartment without a car space on title. They aren’t popular and are hard to sell.

There are some other warning bells I share with prospective unit investors; namely zoning and title types.

Being familiar with stratum title and company share title is imperative. Such title types are hard to finance and tough to pick without a contract review. We have a fair few of them in Melbourne and they do create issues with banks. A thorough contract review will reveal such titles.

Zoning can catch out a lot of investors too; just because a dwelling looks residential doesn’t mean that the bank will view it as a residential security. A bank can reject a loan application on this basis, regardless of pre-approval status.

Can an investor target Melbourne units with a sub-$400,000 budget?

Most certainly, but challenging lending policy around floor area, title types and zoning is something that will strike often. Outgoings need to be captured carefully too, as higher running costs in a particular building will hamper the investor’s efforts to manage cashflow if the outgoings are a nasty surprise.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU