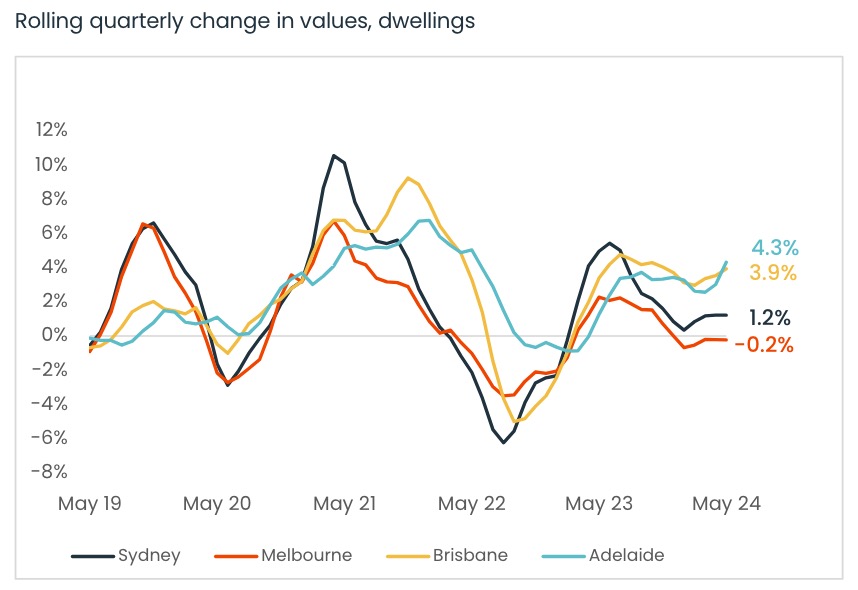

Victoria’s property performance has been lacklustre for quite a while now. Since the market started to correct in May 2022 when interest rates started to rise, property prices haven’t quite returned to the highs of 2021. The chart below shows the quarterly change in values, with Melbourne in red.

Unlike most capital cities, Melbourne’s performance has been pretty dismal. While Perth, Adelaide and Brisbane are all soaring, Melbourne’s monthly results have been swaying between -0.2% and +0.2%.

It’s fair to say that our capital city’s performance has been static.

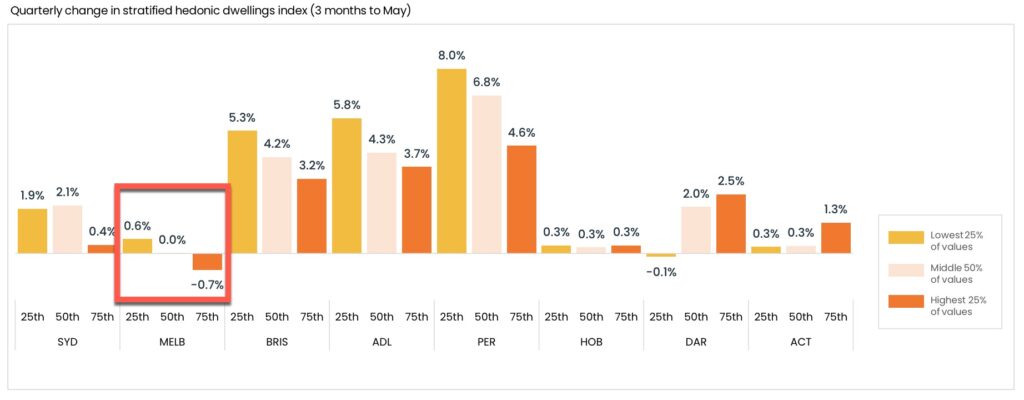

However, like any data set, this figure is generalised. When we focus on the price quadrants, we can see that the highest price quadrant (or most expensive quarter of properties), have declined in value by 0.7%, while the bottom two quadrants (or the cheapest half of properties) have strengthened. In fact, the bottom quadrant have strengthened by 0.6% in this particular quarter.

This is broadly driven by affordability constraints, and there is a correlation showing a heightened level of activity from first home buyers.

While this isn’t great for property owners, it represents a silver lining for property buyers.

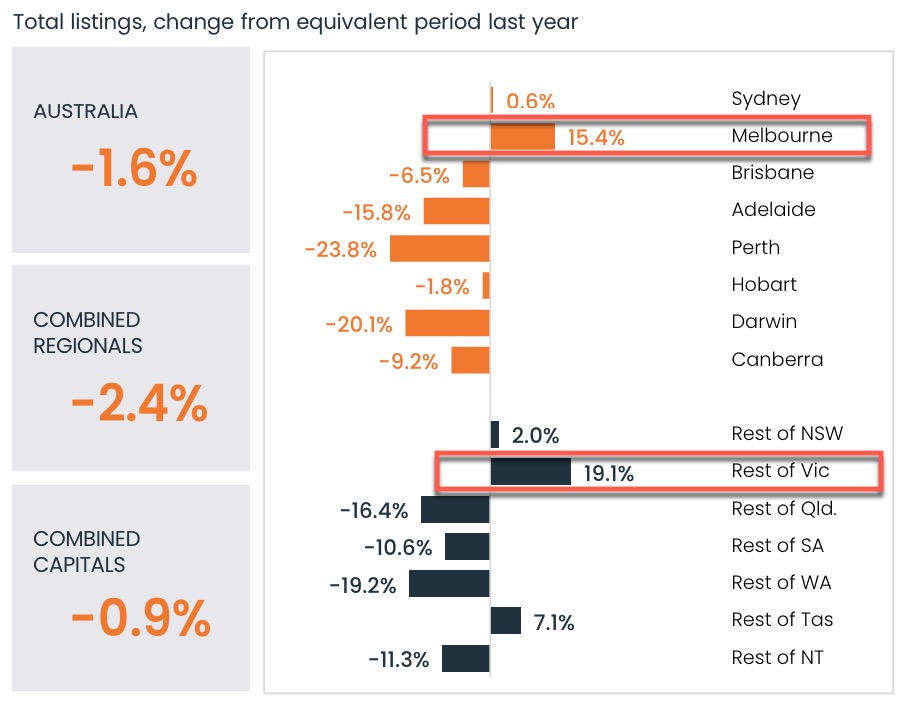

Aside from the capital growth headlines, there is another factor to consider. Listing volumes play a huge role in driving capital growth. If anyone talks to a buyer in Perth, Adelaide, Brisbane, and even Sydney), they will quickly find out that securing a property is a difficult task. Stock levels are really tight and buyers are complaining that there is limited choice and tough competition.

In Victoria, it’s a very different story.

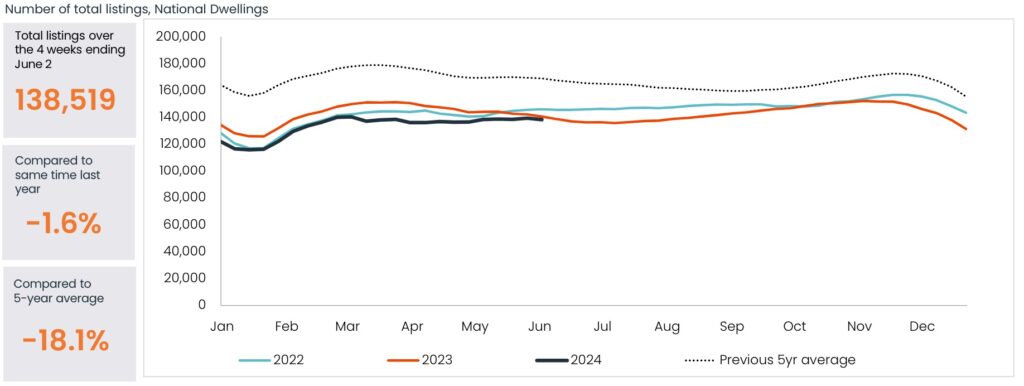

This chart below shows total listing numbers. Unlike new listings, which are higher nationally, it is total listings that directly impact the supply and demand ratio.

The chart below shows how we are tracking nationally against previous years and the five year average. Supply is tighter, although as illustrated above, not in all cities and regions.

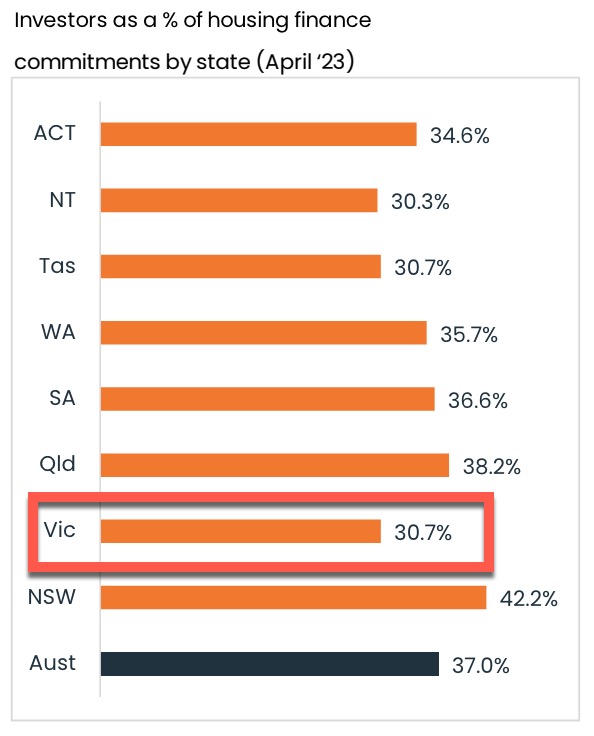

To compound the issue for Victoria, investor participation (or lack thereof) is an issue. Victoria is experiencing a disproportionate amount of investor-led sales currently. This is due to a cocktail of disincentives; higher land tax, mandated compliance costs and onerous rental reforms, many of which favour renters over landlords.

Overall buyer participation is down, yet stock volumes have increased.

Could it be that current buyers are in a purple patch? After all, Melbourne’s property clock has sat still for buyers over the last year. Choice is up, competition is low, and listings are prevalent.

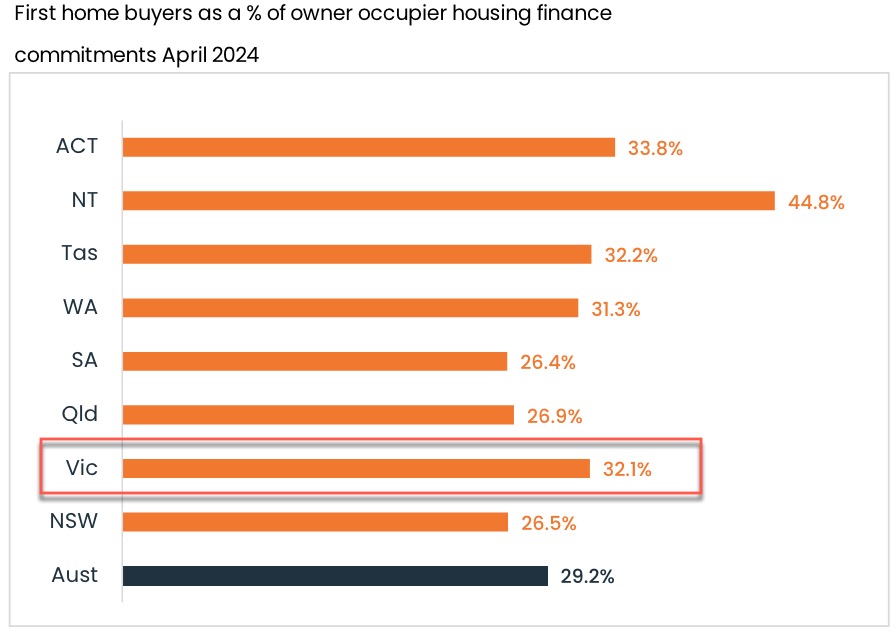

First home buyers have certainly taken the lead and spotted the opportunity. While Victoria is not dominating, it is certainly not lagging either. Victoria’s first home buyer activity is greater than the national average and in the top half of all states and territories.

Buyers who find themselves in hot markets with FOMO (fear of missing out) reining often wish for conditions like we have today. So to all prospective Vic buyers out there, what are you doing?

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU