The next three Sunday blogs are a look into some of my own property investments. I’ve penned this to share my mistakes and my outcomes…. and to demonstrate the power of patience and time.

I’ve been a buyers advocate for thirteen years now, and I first started working in the real estate industry twenty years ago. My exposure to property, (and it’s theory), and in particular, lending policy (when I was a mortgage broker) has taught me so much… but like all accumulated knowledge, it doesn’t come immediately. It takes many years.

My pre-real estate purchases weren’t necessarily dire, but they weren’t all amazing either. I’ve been very consistent over the years when I’ve noted that even the B grade properties perform if given patience and time.

Property is a very forgiving asset class for the patient investor.

This first of three is focusing on one of our gentrifying suburb investments. Unlike this earlier ‘accidental investment’ purchase, this was deliberately chosen as a property we’d never live in, and one we would plan to hold and ultimately retiring the debt.

We circled in on Frankston North. This suburb has come a long way in the last decade, but in 2006 it was only at the beginning of it’s gentrification journey. The Eastlink freeway hadn’t yet been announced formally, (although we knew the state had plans for such a connector).

From a socio-economic point of view, Frankston North presented it’s challenges.

Could have we chosen a blue chip suburb instead?

The answer is no. At the time we didn’t have surplus cashflows to cover a blue chip, negatively geared investment. I had also just fallen pregnant with our daughter and knew all too well that my borrowing capacity would nose-dive once I was on maternity leave.

I’d chosen this suburb after considering a few locations where a house on full land, 5% gross rental yield and budget of $160,000 could align. Frankston North seemed to have some future growth drivers, and proximity to rail, freeway, hospitals and the Mornington Peninsula were just a few.

Mornington’s house and land estates were offering allotments for significantly higher prices, and while Frankston North’s stigma may have steered house buyers to Mornington, the price differential was astonishing, and Mornington was much further south and without rail amenity.

We bought two in succession; both in a similar part of the old ministry housing estate. After spending a little bit of time there, we’d decided on one particular pocket that seemed to have a few more renovations underway than other pockets. At the least, we wanted to be ahead of the curve if and when this suburb gentrified.

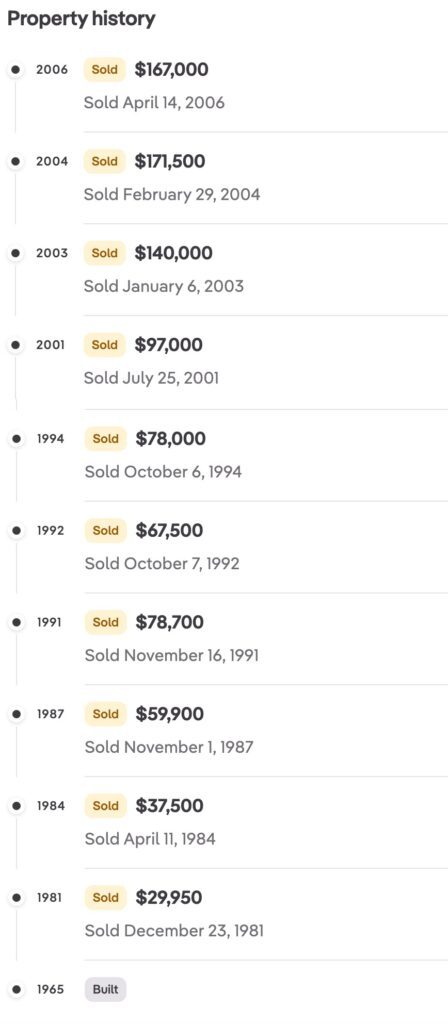

I negotiated a purchase price of $167,000 in early 2006. The house we’d secured in a neighbouring street a week prior cost the same amount, and like many ministry housing estates, the land sizes and styles of home are very consistent. I remember saying to the agent, “I’m not paying $175,000. The other is a perfect comparable sale and I secured it for $167,000”. I didn’t have access to online portals back then like I do today.

Little did I know that the vendor had paid $171,500 two years’ earlier.

The rental return broadly covered our expenses, but the tenant experience wasn’t great in the early days. We became familiar with VCAT during this time. The house was particularly rugged, both inside and out. The tenants that we had didn’t respect the property and small fixes and repairs just continued like a merry-go-round.

Ultimately, the only way to have a better landlord experience was to renovate the property.

We, (the royal ‘we’) managed the renovation ourselves ten years later in 2016. Husband is particularly handy and has a trade background, which is optimal for an investing couple.

Our tenant experience has been great since then, with our renters enjoying their home and looking after it well.

The renovations cost around $80,000 in 2016; a figure representing almost half of the purchase price. However, in that ten year period our capital growth for the suburb did indeed deliver outperformance. Our equity position was significant and not only could we borrow for the renovation, but we could also put it to use for other investment acquisitions.

The earlier years of tenant upset, non-payment of rent, malicious damage and tribunals were a significant point of stress for us. At times, Husband would have happily sold the property.

But we hung in there with our eye on the finish line. Nowadays, the property rents for $450 per week and delivers strong positive cashflow. It’s value sits around $600,000, an 8% year on year return, but factoring in the $80,000 spend at year 10.

We learnt a lot about tougher neighbourhood climates, but we also put in place some great risk mitigating steps. The renovation made an enormous difference to our landlord experience, but maintaining costs is essential, otherwise overcapitalisation is risked. Timing the renovation with asset price movements in the area is essential too.

Nobody wants to have spent more on their property than the property is worth.

Having a great property manager makes the biggest difference in my view. We got in touch with a fabulous local property manager some years in and her clear advice and support enabled us to navigate the stormy waters and design a suitable renovation plan.

Property is a long game, and time is the best ingredient. But knowing when to update a property, and how much to spend certainly helps.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU