It’s easy to find fault in our individual investing journeys, particularly when we consider all of our valuable learnings over the decades and reflect on some of the early decisions we made. A number of my own acquisitions were made preceding my time as a buyers agent and I often reflect on the things that I’d have done differently in hindsight.

From buying troublesome property with ongoing tenant issues to selling good property in an effort to access equity, I’ve had a few blunders that I’ve written about openly.

But as I often say, property is a forgiving asset class.

I listen to Stuart Wemyss’ podcast regularly (Investopoly; if you haven’t discovered it, this podcast is a must for the playlist and the episodes are short and punchy; perfect for a short drive).

A few of Stuart’s semi-recent podcasts got me thinking about how we should focus and reflect on our own property investment journeys, because it’s so easy to fall into the trap of thinking short-term, and critiquing our own decisions when fast profits don’t ensue.

It should be of no surprise that my own personal wealth portfolio is all wrapped up in property. I started young, combined forces with a partner who has the same wealth-creation vision, and forged a strategy that was tailored to our own personal income and lifestyle situation. All of the past little mistakes, tough learnings and retrospective ideas aside, it’s fair to say that so far, it’s been a successful journey and our plans are on track.

So when I ask myself, “what are the three key things that have enabled a successful property investing outcome so far?”, some of Stuart’s podcast episodes have certainly resonated.

I also consider past clients, (many of whom are now also friends) and their successful property investing journeys, and unsurprisingly, these three key aspects apply to their success too. Here they are;

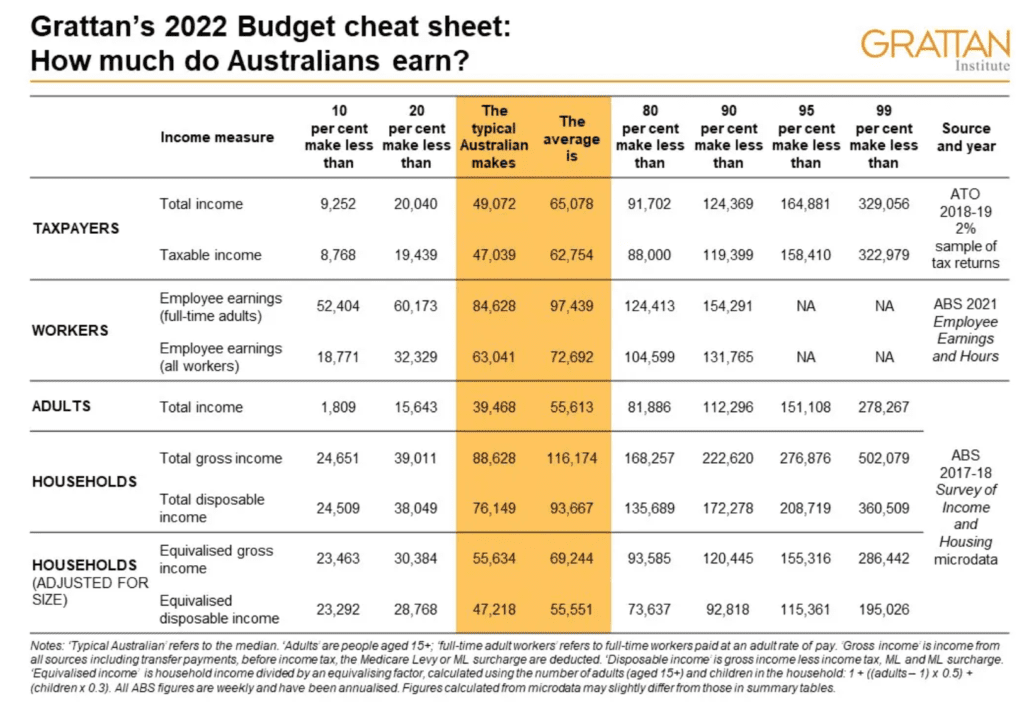

First and foremost relates to cashflow. Ensuring that the cost of holding the property doesn’t interfere with living a happy life is imperative. High income earners who aren’t impacted by the prospect of hefty out of pocket contributions are rare, and this chart that was prepared by the Grattan Institute may surprise some, but it clearly shows that the percentage of tax payers who earn greater than $165,000 are less than five per cent of the Australian population.

Contrary to popular belief, property investors aren’t all rich, and we rely on regular investors in our country to facilitate housing options for renters.

Factoring in the holding costs when embarking on a property investment journey is critical for individuals and households, because the implication of getting the sums wrong spells a regretful, (or distressed) sale. The financial cost includes stamp duty and any losses if the timing of the sale was unfortunate.

Every investor should be calculating the out-of-pocket costs associated with investing to ensure that they aren’t biting off more than they can chew. As I say to investors, “your property should work around your lifestyle, not the other way around”.

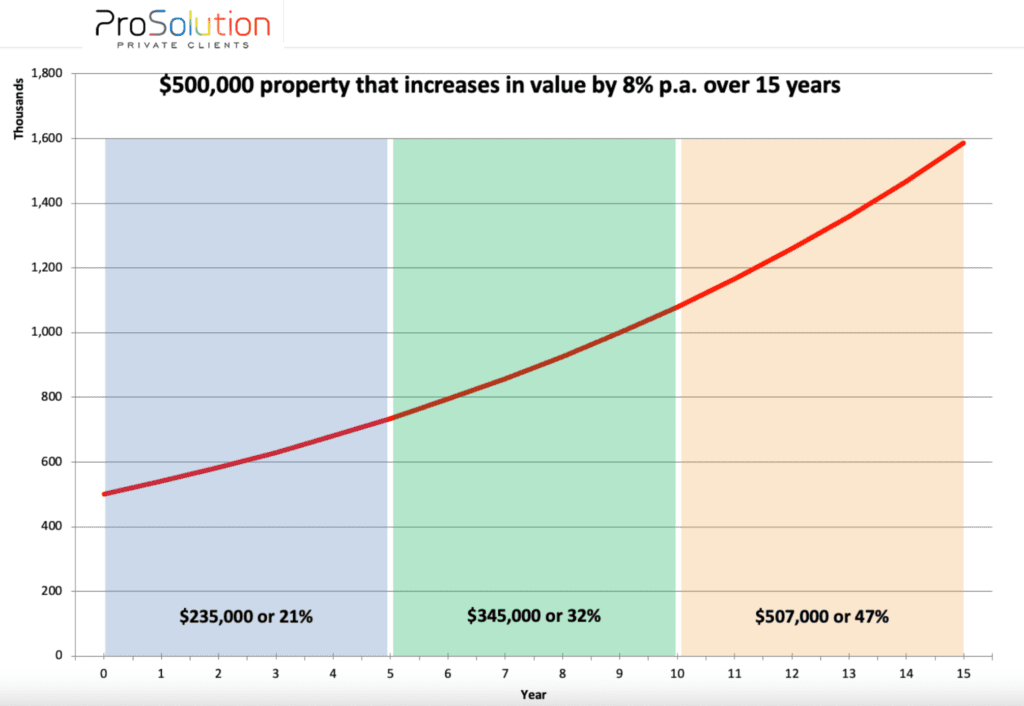

The second element to a successful journey involves being patient. Stuart’s episode about patience and discipline rang so true and it reminded me of some past client ‘wins’ that in hindsight, were cashed in too early. Often, property owners will get excited about a strong gain over the short term and they’ll make the decision to sell their property and crystallise their gain. I always feel a sense of disappointment when past clients decide to sell for this reason. One of my favourite Investopoly charts is this one below and I’ve referenced it many times. It illustrates the power of time and how valuable compounding growth becomes as the tenure of ownership continues.

It’s fair to say that by the time an investor is reaching their third “five year term”, their property is likely to be cashflow positive, (or at least very close to neutral in the case of a higher-priced, capital growth asset). Rents don’t always grow in perfect synchronicity with capital growth, but the two rates of growth don’t tend to vary too greatly over time. As rents grow, most investors will be paying down the principal of their loan in tandem.

For those who start investing early enough and stick to their strategy, it’s conceivable that they can accumulate property assets and pay them down in full before retirement dates strike.

Which leads me to the final important element that I credit a successful property investing journey to.

Getting started as early as possible.

It’s an old saying, but a good one. Time in the market versus timing the market. Time is our most valuable ingredient.

More links here.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU