I was reflecting on a few of my recent and memorable prospect meetings yesterday while I drove down to Geelong. I started thinking about the key things that so many investors get wrong, and when I categorised the conscious-decision based mistakes, I recognised five clear variants.

That is, five critical errors that investors consciously decide to make.

Many of the mistakes that I see investors make are often based on lack of knowledge, oversight, invisible issues or trusting the wrong advice. But in this instance, I applied my thoughts to those mistakes that people walk right into, in a deliberate fashion, with an air of confidence that they are either saving money, making money or optimising their own future wealth.

I’ve penned this today in the hope that it challenges some of the thinking behind these approaches. So here they are, in no particular order:

Getting personal – many investors think that their own preferences and familiarity with a property and/or suburb give them an edge. Whether it is an aesthetic style they favour, or a street they know as ‘the best street’ in the suburb, this type of bias can close them from greater opportunity, despite their belief that they hold the advantage over other buyers. I often have to reprogram buyer beliefs when it comes to preferential bias. A common phrase I share is as follows.

“Unless you are representative of the target tenant, your own preferences won’t necessarily equate to a better outcome.”

And lastly, those who choose to stick to their own suburb so that they can “keep an eye on the property” are missing out on thousands of other, (potentially better) suburbs.

Just because we love our own suburb doesn’t mean it’s the best suburb to invest in.

Saving tax – when get tax back, it’s because we’re losing money.

That’s right; whether it’s negative gearing, a capital loss or depreciation, it’s due to a loss. Our ATO recognises all three and allows for this in an effort to compensate investors. Maximising tax deductions is always sensible, but chasing maximised tax deductions when selecting a property is not at all sensible.

Why spend a dollar to save thirty cents?

Investors who select brand new property in an effort to claim higher tax depreciation miss out on so much more. A higher land to asset ratio property in a quality location will deliver long term capital growth benefits that outstrip any of the short term tax deduction benefits.

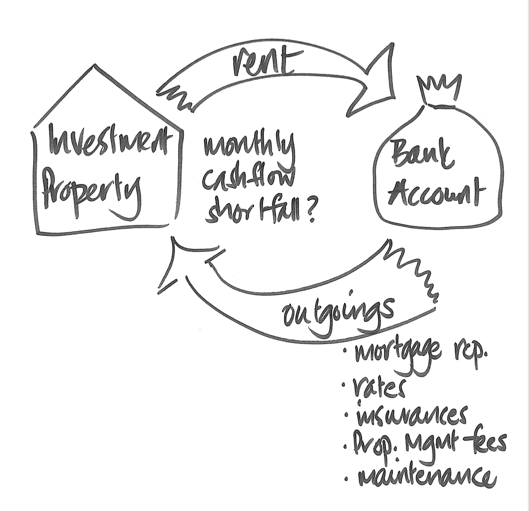

Ignoring cashflow constraints – Some buyers look at property investing as a way of forced savings. I often get the question; “Cate, where would you buy with $700,000?”

Instead of asking what a buyer can spend, I prefer to focus on what they can budget for. Most property investment opportunities in Victoria, (and particularly in our metro city) are cashflow negative; in other words, the rent doesn’t quite cover the mortgage repayments and outgoings. Every investor should have a firm grip on the ‘out of pocket’ expenses they can comfortably cover every month.

When buyers ignore this, (whether it’s laziness or wishful thinking), they are more likely to find out the hard way when cashflow is tight and the investment property is causing them financial stress.

A forced sale at an inopportune time can be a devastating blow.

DIY’ing the stuff you shouldn’t – From preparing one’s own contract to renovating without permits, I’ve seen it all. Some of the silliest DIY jobs are the ones that don’t actually cost much.

So many buyers think that managing their own tenants and collecting the rent is not worth the seven per cent or so that a property manager commands. Fast forward to tribunal attendances, lack of familiarity with the legislation, and bad tenant placements. No amount of cost-saving is worth the headache of a shocking tenant experience.

The same goes for preparing tax returns.

Saving a few hundred dollars can sometimes cost thousands.

Being impatient: either selling to crystallise a short gain or selling because it hasn’t outperformed in a short time frame – Property is a long game. The cost of trading in this asset class is very costly when compared to share trading and other asset classes. From stamp duty to agents fees, property investors can whittle away their returns very quickly if they are too active when it comes to trading.

I remember spotting a familiar property on line a year ago and I was immediately concerned that perhaps our investor client had dealt with a bad experience in relation to her property. I checked in to see if she was OK.

“Oh yes, I’m totally fine. It’s done so well – I’ve almost doubled my money. I decided to take the gain”.

I should have been happy for her but I couldn’t feel happy about the situation. A five year buy and hold strategy wasn’t what I had in mind when I helped her buy in 2014. I could only wonder how she’d feel in 2024 about selling a performing asset for no particular reason ten year’s prior.

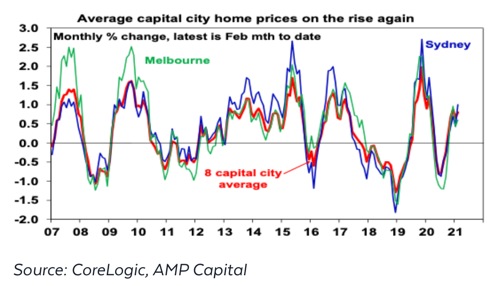

Likewise, capital growth trajectories typically aren’t linear. Property performance oscillates like static. It’s only when we step right back from the chart and look at it from a distance that we can see the benefit of time.

I hope that any of these five points strike a chord with some of our readers and challenge the thinking of someone who is about to make one of these conscious decisions.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU